USAA Car Insurance Review: Best For Military Families?

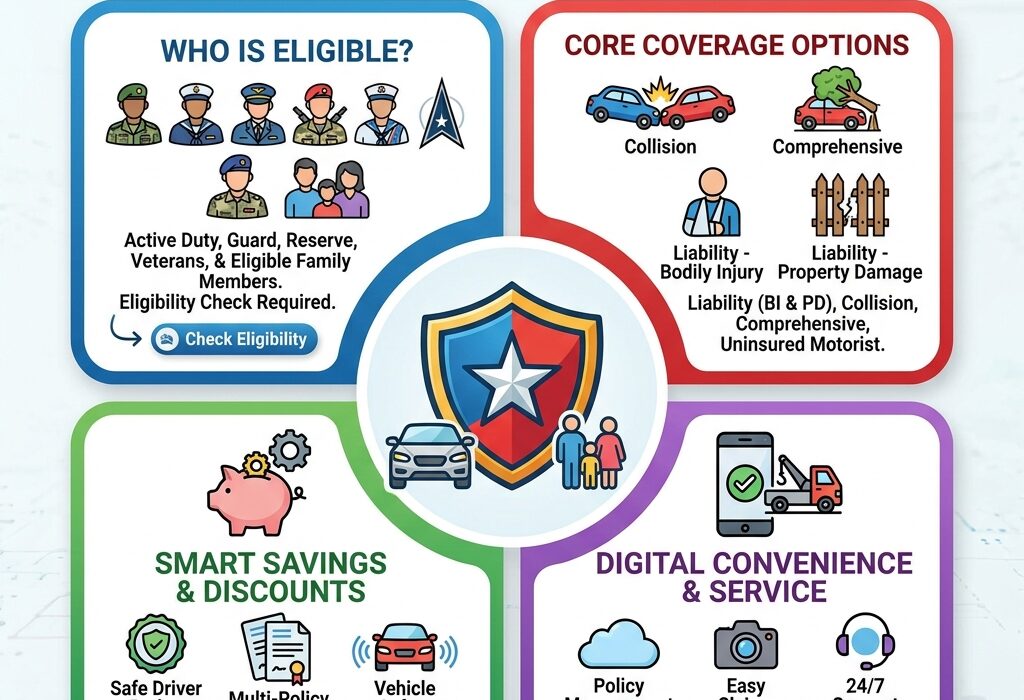

USAA Car Insurance Eligibility and Membership: Key Points

- Exclusivity: USAA Car Insurance is not open to the general public (civilians). It is an exclusive financial institution dedicated solely to the US military community and their families.

- 96% Customer Retention Rate: Compared to the insurance industry average (80-84%), USAA boasts a record 96% customer satisfaction and loyalty rate.

👥 Who is Eligible?

- Active Military Personnel: Current members of the US Army, Navy, Air Force, Marine Corps, Space Force, Coast Guard, National Guard, and Reserve forces.

- Veterans: Retired or former military personnel who received an “Honorable Discharge.” Those discharged due to court-martial or a “Dishonorable Discharge” are ineligible.

- Cadets and Midshipmen: Officer candidates at military academies (e.g., West Point) and advanced ROTC students.

- Family (The Legacy System):

- Current spouses or widows/widowers of eligible members (provided they do not remarry a non-member).

- Biological, adopted, and stepchildren of eligible members.

❌ Who is NOT Eligible?

- Parents: Parents do not gain membership through their children’s military records (membership only passes down to the next generation).

- Siblings: Having a brother or sister in the military does not make you eligible.

- DoD Civilians: Department of Defense civilian contractors or civil servants who have never worn the uniform are ineligible.

⚙️ Verification and the ‘Legacy’ Benefit

- The Legacy Chain: Civilian children automatically become eligible through their military parents and receive a 10% legacy discount for young drivers.

- Strict Verification: Membership is vetted through government databases. Applicants must provide their DD Form 214 (discharge papers), military ID, or their sponsor’s details.

Conclusion: Exclusivity is the key to USAA’s success. By restricting its customer base to the highly disciplined military demographic, the company secures its ‘risk pool,’ resulting in fewer claims and keeping rates highly affordable.

Financial Strength and Top Ratings

- Top-Tier Grading (Including Latest Ratings):

- A.M. Best: A++ (Superior) – The industry’s highest rating.

- Standard & Poor’s (S&P): AA+ (Very Strong).

- Moody’s: Aaa (Highest Quality).

- Massive Reserves: USAA holds over $40 billion in cash reserves (surplus).

- The Benefit: Even during severe natural disasters like Category 5 hurricanes, the company remains financially secure, ensuring your claim payouts are 100% protected.

‘Unofficially #1’ in J.D. Power

- Highest Score: USAA consistently scores between 890-905 in Claims Satisfaction, far exceeding the industry average (870-880).

- The Ranking Secret: Because membership is not open to the general public, J.D. Power does not grant USAA official ‘awards.’ However, in their ‘Unranked’ category, USAA consistently stands as the #1 company in America.

USAA’s Best Coverage Options: Impenetrable Protection

USAA doesn’t just offer affordable rates; it provides 10 incredibly powerful ‘add-on’ coverages to protect members from financial ruin in the event of an accident:

- Car Replacement Assistance (CRA): In the event of a total loss, USAA pays the vehicle’s actual cash value (ACV) plus an additional 20%, making it easier to purchase a replacement car.

- Rideshare Gap Protection: For Uber/Lyft drivers, this covers the risky “gap” period when the app is turned on, but there is no passenger in the vehicle.

- 24/7 Roadside Assistance: Provides rapid assistance for highway breakdowns, including towing, flat tire changes, jump-starting a dead battery, lockout services, and fuel delivery.

- Rental Reimbursement: While your car is at the shop being repaired after an accident, this coverage pays for your rental car (features direct billing with Hertz/Enterprise).

- Accident Forgiveness: If you have maintained a safe, clean driving record for 5 years, USAA will not raise your premium for your first at-fault accident.

- Uninsured/Underinsured Motorist (UM/UIM): If an uninsured driver hits your vehicle, this fully compensates you for medical bills, lost wages, and car repairs.

- Custom Parts and Equipment (CPE): If you have expensive aftermarket modifications on your vehicle (such as a $5,000 lift kit or custom alloy wheels), this ensures they are fully covered in the event of an accident.

- MedPay and TRICARE Coordination: Promptly pays medical bills for you and your passengers if injured in an accident, and coordinates with TRICARE (military health insurance) to prevent double-billing.

- Glass Coverage (Zero Deductible): For minor windshield cracks (chips), USAA repairs it completely free of charge (waiving the deductible); you pay $0 out of pocket.

- Personal Umbrella Insurance: If you are sued following a major accident and your auto insurance limits are exhausted, this provides an additional safety net of $1 million to $5 million to protect your assets.

(This summary highlights that USAA’s policies operate on a “leave no loopholes” strategy, making it the most secure choice for military families.)

Car Insurance Company Comparison with USAA Car Insurance: All You Need to Know

America’s “Top 20 Giants” (The Big 20)

This group controls over 95% of the entire US auto insurance market.

Discounts & Telematics Program: 12 Strategies to Minimize Premiums

Telematics (Driving Behavior) Discount

- 1. USAA SafePilot® Program (Up to 30% Discount): This is a smartphone app that tracks your driving habits, specifically monitoring hard braking and phone usage. You receive an immediate 10% discount just for enrolling, and with safe driving, this discount can grow up to 30% at policy renewal. Best of all: the app does not penalize you for poor driving; it only applies discounts.

Military-Specific Discounts

- 2. Deployment & Storage Discount (Up to 60% Reduction): If a service member is deployed overseas and their vehicle remains parked in a secure garage for more than 30 days, USAA assumes zero liability and collision risk, slashing the premium by up to 60%.

- 3. On-Base Garaging Discount (15% Discount): US military bases are highly secure. If you park your car on base, the risk of theft and vandalism drops significantly. In return, USAA offers a 15% discount on your comprehensive coverage.

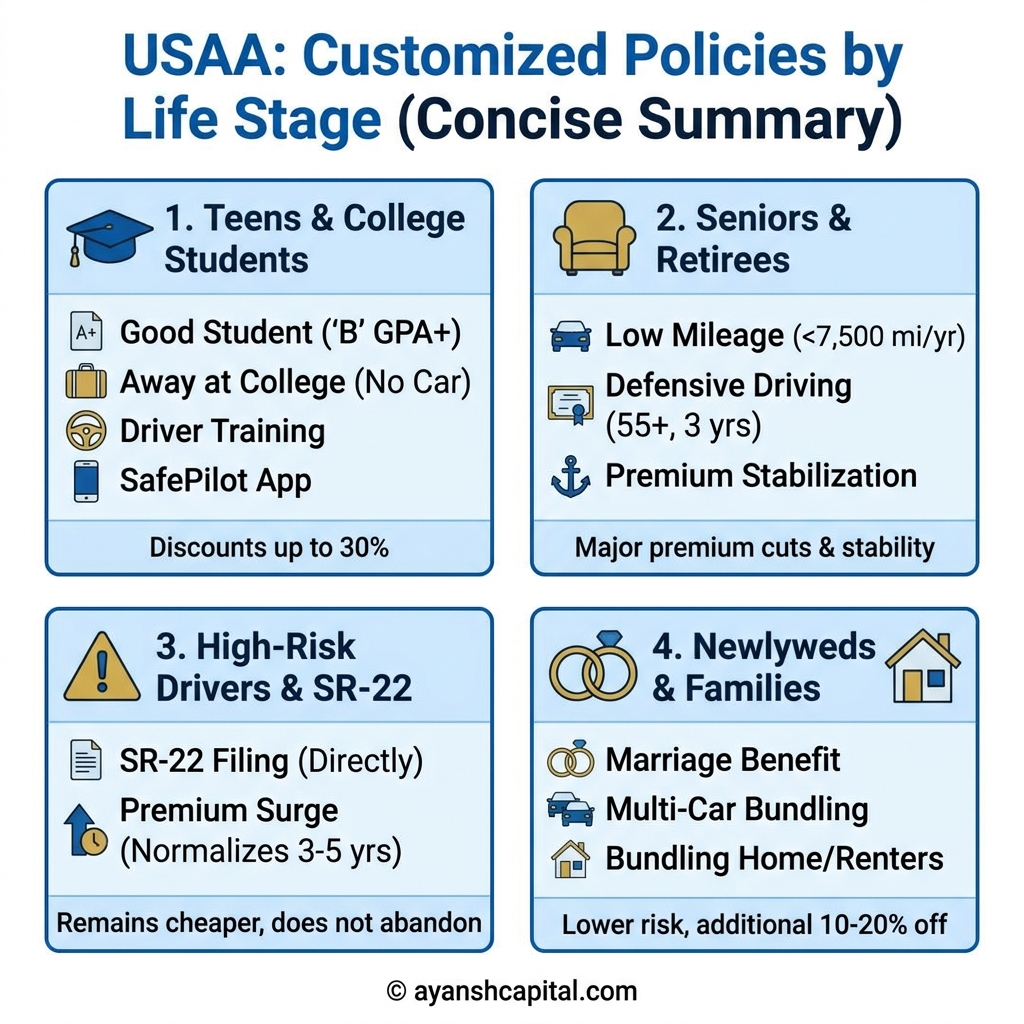

Youth & Student Discounts

- 4. Family ‘Legacy’ Discount (Up to 10%): If your parents have USAA auto insurance and you start your own separate policy as a young adult, USAA rewards your loyalty with a special legacy discount of up to 10% for life.

- 5. Good Student Discount (Up to 15%): Insuring young drivers is notoriously expensive. However, if a full-time high school or college student maintains a ‘B’ average (3.0 GPA) or higher, they receive up to a 15% discount on their premium.

- 6. Basic Driver Training Discount: If a new driver under the age of 21 successfully completes an approved basic driving course, their premium receives an additional reduction.

Bundling & Vehicle Discounts

- 7. Multi-Policy Bundle Discount (Up to 10%): If you bundle your USAA auto insurance with their homeowners or renters insurance, you receive up to a 10% discount on both policies.

- 8. Multi-Vehicle Discount: Insuring two or more cars under the same policy (within the same household) significantly lowers the ‘per vehicle’ premium cost.

- 9. New Vehicle Discount: Cars that are 3 years old or newer are equipped with modern safety features. USAA recognizes this by applying a special ‘New Car Discount’ to your premium.

Loyalty & History Discounts

- 10. Low / Annual Mileage Discount: If you are retired or work from home and drive less than the average commuter (typically 5,000 to 7,500 miles annually), USAA lowers your premium due to the reduced risk of an accident.

- 11. Length of Membership & Loyalty Discount: USAA translates loyalty into cash. The more years you stay with USAA, the more stable your rates remain at renewal, often resulting in an automatic ‘Premium Drop.’

- 12. Defensive Driving Course: Aimed primarily at seniors (ages 55+) but available to any driver, completing a state-approved defensive driving course grants an additional 5% to 10% discount that remains active for 3 years.

USAA Car Insurance (50-State)

USAA Mobile App & Tech: A ‘Virtual Headquarters’ (Concise Summary)

To offset its lack of physical offices, USAA’s mobile app serves as a comprehensive ‘financial control center,’ boasting top-tier ratings of 4.8/5 on the Apple App Store and 4.7/5 on the Google Play Store. Here are its 6 key technical features:

- 1. All-in-One Dashboard (Super-App Model): Banking (checking accounts), auto loans, and auto insurance are all managed right from a single home screen. Members do not need to download separate apps for different services.

- 2. Advanced AI Assistant (EVA): Far more than a basic chatbot, EVA processes complex voice commands (such as instantly looking up a deductible) and executes actual tasks. For instance, stating “add my 16-year-old daughter to my policy” will automatically pre-fill half of the required form.

- 3. Proactive Geo-Location Alerts: Utilizing the phone’s GPS, the app sends out predictive push notifications during severe weather events like hailstorms or wildfires (e.g., “Move your car into a garage”), actively helping to prevent damage and subsequent claims.

- 4. AI Damage Assessment & Live Tracker: After an accident, members can capture and upload 5 to 6 photos of the vehicle, and the built-in AI generates a repair estimate within 15 to 30 minutes. Once the car is at the shop, the app provides a live repair status tracker—mirroring a pizza delivery tracker—covering everything from parts ordered to final delivery.

- 5. Offline Mode & Digital Wallet Integration: Digital ID cards can be saved directly to Apple Wallet or Google Wallet. Even in remote areas with zero cellular data, the app’s ‘Offline Mode’ ensures insurance cards and emergency roadside assistance numbers remain completely accessible.

- 6. Military-Grade Security & Biometrics: Protected by maximum AES-256 encryption, Face ID, and Touch ID. It also utilizes voice biometrics (Voiceprint) technology, allowing members to bypass standard security questions and verify their identity via phone support using just their voice in seconds.

The Takeaway: Through a blend of offline access, proactive alerts, and integrated AI, USAA’s mobile app acts as a round-the-clock digital assistant, placing an entire financial and logistical toolkit directly into the pockets of military members.

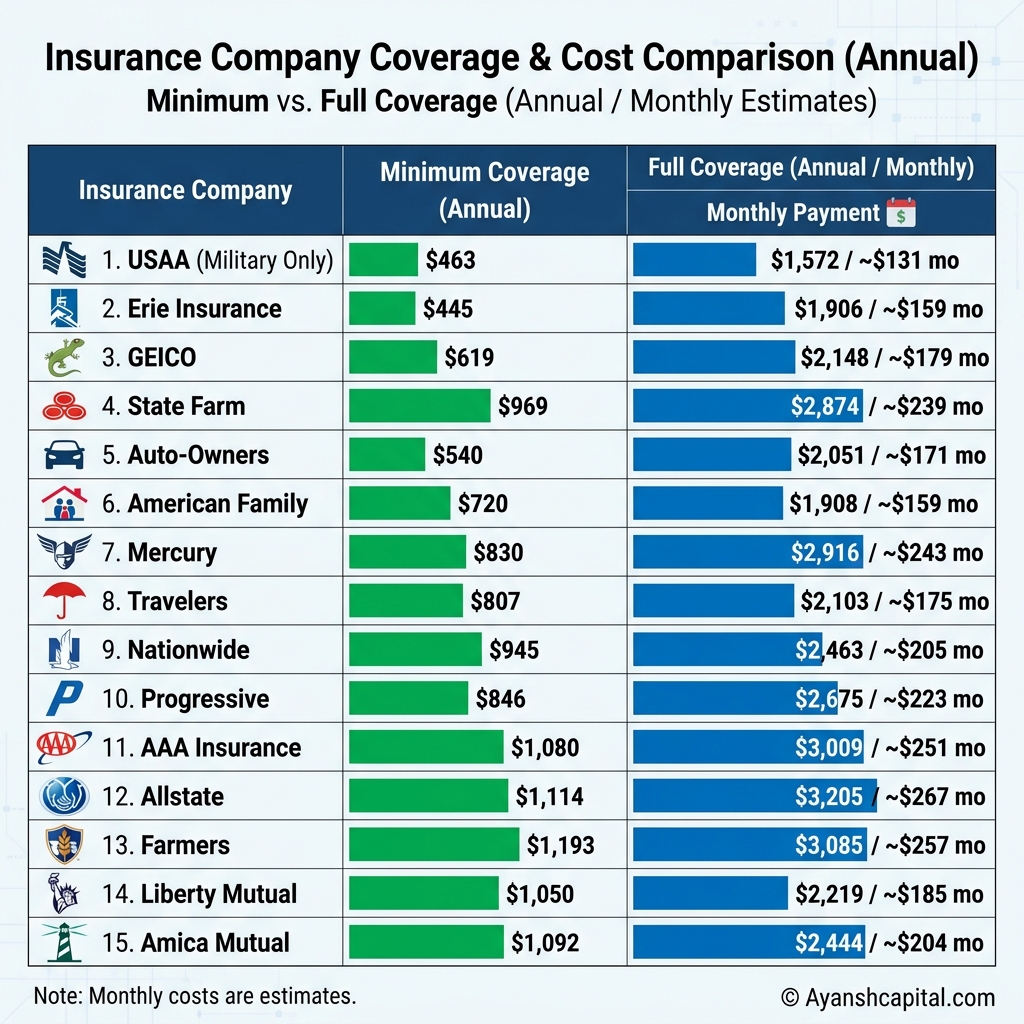

Full Coverage Top 15 Auto Insurance Rate Comparisons

Below is a detailed breakdown of Top 15 Car Insurance average annual rates for full coverage auto insurance across various driver profiles, compared directly against the national average.

USAA’s Financial Ecosystem: A ‘One-Stop-Shop’

USAA is not just an insurance provider; it is a full-scale financial institution. Bundling its various products offers military members immense convenience and significant financial advantages:

- 1. USAA Banking (Payday 2 Days Early): Military paychecks are deposited into checking accounts up to 2 days early compared to traditional banks. It features an integrated dashboard to seamlessly track claims, dividends, and premiums alongside standard automated bill-pay configurations.

- 2. Auto Loans & Car Buying Service (0.25% to 0.50% Rate Discount): Enrolling in auto-pay unlocks an interest rate reduction of 0.25% to 0.50% on USAA auto loans. Furthermore, financing and insuring through USAA automatically syncs vehicle information (like the VIN), eliminating redundant paperwork while granting access to pre-negotiated discounted pricing via their Car Buying Service.

- 3. Multi-Policy Bundling (Up to 10% Savings): Combining auto insurance with either homeowners or renters insurance triggers an immediate discount of up to 10% on the auto policy. Members can also easily scale up their coverage with Personal Umbrella Insurance ranging from $1 million to $5 million to shield assets globally.

- 4. Subscriber’s Savings Account (SSA – Capital Returns): Because USAA operates with a reciprocal structure, a portion of the company’s annual profits is allocated directly into your individual Subscriber’s Account. This acts as an “invisible savings” cache that accumulates over time and is paid out in cash upon retirement or cancellation of membership.

- 5. Life Insurance & Unified Billing (War Zone Coverage): Unlike standard commercial policies, USAA’s life insurance includes comprehensive coverage during active deployments to war zones. All financial obligations—auto premiums, life insurance, and auto loan EMIs—are consolidated into a single billing date from one account.

The Takeaway: The USAA ecosystem eliminates the friction of managing multiple financial vendors. It operates as a cohesive financial shield, rendering military life significantly less complicated and far more cost-effective.

Top 15 Car Insurance Rates by Age & Experience

In the auto insurance industry, age and driving experience heavily dictate your premium. As you gain experience and your statistical risk of accidents decreases, Top 15 Car Insurance Rates by Age & Experience. Here is a quick breakdown of how age impacts your premium:

An Unbiased Review: USAA’s Drawbacks, Complaints, and ‘Hidden Cons’

From an E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness) perspective, while USAA is an industry leader, it is not perfect for everyone. Here are its primary limitations and downsides:

🏢 Lack of Physical Branches and Local Agents

USAA operates on a strictly digital-first model. There are virtually no physical offices or dedicated local agents. If you prefer sitting down face-to-face to review paperwork or value a personal, human touch after an stressful accident, you may find their reliance on mobile apps and call centers frustrating.

🚫 Strict Exclusivity and the Broken ‘Legacy Chain’

No matter how flawless your driving record is, you cannot purchase USAA insurance without a qualifying military connection. Furthermore, the “Legacy Chain” is fragile: if your grandfather was a USAA member but your parent never established a policy, the chain breaks, and you are no longer eligible.

🚗 Gig Economy and Rideshare Geographic Restrictions

Their highly praised ‘Rideshare Gap Protection’ is not available in all 50 states (e.g., New York). Additionally, this coverage is tailored specifically for passenger transport (Uber/Lyft); if you use your vehicle for food or package delivery (DoorDash, UberEats), a claim could be denied at the time of an accident.

⚠️ Strict Underwriting and Policy Non-Renewal Risks

USAA keeps its rates low by exclusively insuring lower-risk profiles. However, if you are convicted of a DUI or rack up multiple at-fault accidents within a year, the company can be ruthless. They will either skyrocket your premium by up to 300% or drop you entirely at your policy’s expiration (non-renewal).

🤖 Dropping Customer Service Scores and Chatbot Frustration

In recent years, members have reported increased phone wait times, sometimes stretching from 30 to 45 minutes to reach a live agent. Furthermore, USAA’s AI chatbot, ‘EVA,’ frequently traps users in automated FAQ loops rather than quickly transferring complex claims or liability disputes to a human representative.

💰 Not Always Cheapest for ‘State Minimum’ Liability

While USAA almost always beats competitors on premium ‘Full Coverage’ packages, it falls short on bare-bones plans. If you own an older vehicle and only want the absolute minimum state-required liability insurance, competitors like Geico or regional carriers often prove to be cheaper.

The Takeaway: USAA is not a magic institution; it is a strictly run financial corporation. If you are a safe, tech-savvy driver with a clean record, you will rarely notice these drawbacks. However, for those seeking a traditional human touch or dealing with a spotty driving history, navigating USAA can be a major challenge.

The Impact of Driving Violations on Premiums: A Comprehensive Breakdown

USAA Auto Insurance: Which Add-Ons Should You Skip? (Money-Saving Strategies)

To avoid ‘over-insuring,’ it is essential to review your policy regularly. Depending on your situation, you can skip the following coverages to save money:

- Extended Vehicle Protection (Mechanical Breakdown):

- When to Skip: If your car is brand new and still covered under the manufacturer’s factory warranty (e.g., 3 years/36,000 miles or 5 years/60,000 miles).

- Reason: Keeping it means wasting money on double coverage.

- Rental Reimbursement:

- When to Skip: If your household owns multiple vehicles, you work from home, or your city has reliable public transportation.

- Reason: Skipping this add-on can easily save you $30 to $60 annually.

- Roadside Assistance:

- When to Skip: If you already have a AAA membership, if the service comes complimentary with your new vehicle (e.g., Honda/Toyota), or if your premium credit card (e.g., Chase) offers it for free.

- Reason: Paying two different providers for the exact same service makes no financial sense.

- ‘Full Coverage’ on Older Cars (Dropping Collision & Comprehensive):

- When to Skip: When your car approaches 15 years of age. Apply the ‘10% Rule’ here.

- Reason (The Math): If your car’s actual cash value drops to $2,500 and your deductible is $1,000, you will only net $1,500 in a total loss event. Paying an annual premium of $300–$400 for such a minor payout is mathematically disadvantageous. Switch these older vehicles to Liability-only insurance.

- Car Replacement Assistance (CRA):

- When to Skip: For vehicles that are more than 10 to 12 years old.

- Reason: CRA pays out an additional 20% of the vehicle’s current value. If your car is only worth $3,000, you will only receive an extra $600. Increasing your premium for this minimal return is not beneficial in the long run.

- Medical Payments (MedPay):

- When to Skip or Reduce: If you already have comprehensive health coverage through TRICARE, VA Health Benefits, or a high-quality, low-deductible private health insurance plan that covers auto-related injuries.

- Caution: MedPay also covers your passengers. Therefore, instead of dropping it completely, lowering the coverage limit is often a safer and highly cost-effective compromise.

The Takeaway: Audit your policy at every renewal cycle and remove any add-on options that no longer align with your vehicle’s depreciation curve or your current lifestyle.

How to Buy USAA Auto Insurance? (Step-by-Step Digital Process)

Through USAA’s digital-first platform, you can purchase auto insurance online or via the mobile app in less than 15 minutes without needing an agent. Here is the step-by-step process:

1.Step 0: Preparation (Pre-Checklist):

Before starting, gather your driver’s license number, Social Security Number (SSN), vehicle’s 17-digit VIN, current insurance policy details, and military service documentation (such as DD Form 214).

2.Step 1: Military Verification:

Entering your details triggers an instant background check against the Department of Defense (DoD) database. If the automated system cannot verify your background, you can manually upload your military ID. Legacy members will need to provide their military sponsor’s details here.

3.Step 2: Risk Profile and VIN Magic:

USAA runs a soft credit pull (which does not impact your credit score) and retrieves your driving history. As soon as you enter your vehicle’s 17-digit VIN, the system automatically detects all safety features and applies your vehicle safety discounts immediately.

4.Step 3: Live Coverage Customization:

An interactive slider allows you to adjust your liability limits (e.g., 100/300/100) and deductibles ($500 to $1,000) while viewing live premium changes. You can add your optional coverages (like CRA or Rideshare) here. Selecting ‘Yes’ for the SafePilot program instantly reduces the quote by 10%.

5.Step 4: Payment and Binding:

Select the policy’s effective date. Opting for auto-pay and paperless billing unlocks an additional 3% to 5% discount. Once the initial payment goes through, digital ID cards are instantly generated, allowing you to save them to your Apple/Google Wallet or send them directly to a dealership.

6.Step 5: Three Essential Post-Purchase Steps:

- Cancellation: Call your previous insurance carrier (e.g., Geico) to formally cancel your old policy.

- App Activation: Download and activate the ‘USAA SafePilot’ app within 7 days to lock in and maintain your enrollment discount.

- Auto-Pay Check: Ensure that your bank account or card information is correctly linked to avoid missed payments.

The Takeaway: USAA’s user interface is transparent and highly optimized, allowing customers to easily tailor policies and set budgets completely free from high-pressure sales tactics.

The Digital Process of Filing a Claim with USAA (Concise Summary)

USAA’s claims process is an excellent blend of technology (AI) and convenience, designed to minimize post-accident stress. Here is the step-by-step procedure:

1.Safety on the Scene & GPS Assistance:

The app’s ‘Smart Checklist’ allows you to call 911 directly.

The phone’s GPS sends your exact location to the towing service.

The app helps gather witness info, police reports, and the other party’s data (and advises against admitting fault at the scene for your legal protection).

2.AI Damage Estimation:Virtual Adjuster & Photo Estimates.

Take photos of the car’s damage using the app’s guided camera.

USAA’s AI (Machine Learning) assesses the damage and provides an estimate within minutes.

For major damage, a ‘Virtual Adjuster’ approves funds from their desk within hours (eliminating weeks of waiting for a field agent).

3.Choosing a Repair Shop:STARS Network vs. Independent.

STARS Network: Choosing a USAA-certified repair shop enables ‘direct billing.’ You only pay your deductible, and USAA pays the mechanic directly.

Independent Shop: You can also choose an independent garage of your choice; in that case, USAA will issue a check directly to you.

4.Rental Car Setup:Zero Out-of-Pocket.

A rental car can be booked directly with Enterprise or Hertz through the app.

USAA sets up ‘direct billing’ with the rental company, meaning you do not have to pay out-of-pocket and deal with the hassle of filling out reimbursement forms later.

5.Live Claim Tracker: Domino’s-Style Updates.

During repairs, the app provides real-time, live status updates (e.g., “parts ordered,” “car is in the paint booth,” and “ready for delivery”).

6.Lifetime Warranty & Total Loss Resolution:

Lifetime Warranty: Repairs done through the STARS network come with a lifetime guarantee on the work (parts and labor) for as long as you own the vehicle.

Total Loss: If the car is considered “totaled” and you have Car Replacement Assistance (CRA), USAA adds an extra 20% to the car’s market value and deposits the funds directly into your bank account (EFT) within a few days.

Conclusion: USAA’s primary goal is not to leave customers stranded after an accident, but to get them back on the road as quickly as possible by leveraging their ‘super-app’ and AI technology.

State-Specific Rules: Ultra-Short Summary

- CA (Prop 103): No credit/gender pricing; USAA stays 18–22% cheaper via its low-risk military pool.

- FL (No-Fault Crisis): $10K PIP required; USAA’s $40B+ reserves ensure stability while other insurers flee.

- TX (Weather Risks): High limits + hailstorms; San Antonio HQ means rapid localized claim payouts.

- MI (PIP Loophole): High costs due to unlimited PIP; TRICARE/VA users can opt-out to slash premiums by 40%.

- NY (High Density): $50K PIP mandate; excels in upstate winter driving (Fort Drum) and rivals Geico in NYC.

- HI (Rate Bans): Bans credit/age/gender pricing; offers crucial transit coverage for vehicle shipping.

- NC (SDIP Trap): Tickets trigger mandatory 25–45% hikes; USAA Accident Forgiveness shields members.

- PCS Moves (Ultimate Win): Cross state lines seamlessly; update address in-app to auto-adjust policy with $0 lapse.

USAA: Not Just Insurance, A Financial Shield (The Ultimate Verdict)

The Core Message: If you are eligible for USAA, choosing another insurance company is a major financial mistake.

1. Best Value & A++ Security: It is not just cheap; it offers ‘A++’ financial strength. It survives natural disasters without going bankrupt and provides guarantees like ‘Car Replacement’ and ‘Lifetime Repairs’.

2. The Power of Exclusivity: Being restricted to military members creates a highly disciplined, low-risk driver pool. This results in fewer accidents, allowing the company to give customers cash dividends and lower premiums.

3. Best for Military Life: It seamlessly adapts your coverage during PCS moves without any gaps. If you are deployed overseas, putting your car in “Storage Mode” instantly cuts your premium by 60%.

4. Is it right for you?

- Choose blindly if: You want full coverage, have young drivers (ages 16-25) at home, want to bundle everything in one app, and value ‘Accident Forgiveness’.

- Consider alternatives if: You have a very old car and only want the absolute cheapest ‘State Minimum’ coverage, or if you strictly need a local, in-person agent to talk to.

5. A Generational Legacy: Founded in 1922 by just 25 military officers, it has now become a $200 Billion empire. Its goal is not just to insure you, but to securely protect your future generations as well.

Questions covering the key aspects of USAA car insurance

1. Q: Who is eligible to buy USAA car insurance?

A: Only active-duty military members, veterans, and their immediate family members are allowed to purchase it.

2. Q: What is the biggest advantage of USAA insurance?

A: It is perfectly tailored to military life, offering some of the industry’s cheapest rates backed by a superior A++ financial rating.

3. Q: What is the USAA SafePilot program and its main benefit?

A: It is a telematics smartphone app that tracks safe driving habits to give you up to a 30% discount upon policy renewal.

4. Q: How does USAA help you save money during an overseas deployment?

A: By allowing you to put your garaged car into “Storage Mode” via the app, USAA instantly slashes your premium by up to 60%.

5. Q: How does the Car Replacement Assistance (CRA) add-on work?

A: If your vehicle is declared a total loss in an accident, USAA pays you an additional 20% on top of the car’s actual cash value.

6. Q: Does USAA provide adequate coverage for rideshare (Uber/Lyft) drivers?

A: Yes, their “Rideshare Gap Protection” safely covers the high-risk period when your app is on but you haven’t picked up a passenger yet.

7. Q: How fast is the USAA claims process after an accident?

A: You can upload damage photos through their app, and their advanced AI system can estimate and approve initial payouts within hours.

8. Q: What is the main benefit of using USAA’s STARS repair network?

A: If you use their certified repair shops, USAA provides a free lifetime warranty on all the repair work (both parts and labor).

9. Q: Will USAA immediately hike your premium after a minor accident?

A: No, if you have been accident-free for 5 years, USAA will completely waive the surcharge for your first at-fault crash using “Accident Forgiveness.”

10. Q: What is the biggest weakness or drawback of USAA insurance?

A: They do not have local physical agent offices, meaning all your interactions and claims must be handled digitally via the app or over the phone.