Travelers Car Insurance Discounts to Lower Your Premium ✅

Corporate Overview of Travelers Car Insurance

A Legacy of Innovation (1853 to Present)

The Travelers Car Insurance Companies, Inc. is not just an insurance provider; it is a historic pillar of the American financial sector that grew alongside the industrial revolution. Tracing its roots back to 1853, Travelers has a long track record of industry firsts.

It is a company that has consistently anticipated the future. Today, Travelers holds the prestigious distinction of being the only pure property and casualty (P&C) insurance company included in the Dow Jones Industrial Average.

The Iconic “Red Umbrella”

First used in advertising during the 1870s, the “Red Umbrella” is one of the most recognized corporate symbols in the world. It is more than just a marketing tool; it represents the company’s core philosophy: providing a strong, reliable shield against unexpected disasters and life’s storms. For consumers, this umbrella is a psychological guarantee of financial backup and peace of mind.

Market Position & Strategy

The secret behind Travelers’ enduring success is its strict underwriting discipline. Instead of just aggressively collecting premiums, the company leverages advanced data analytics and AI to accurately assess risk. In the auto and home sectors, they strategically target safe drivers and homeowners looking to bundle policies. This approach keeps their combined ratio—a key measure of insurer profitability—highly stable and healthy.

Travelers Car Insurance: What We Like and What We Don’t

✅ Pros (Advantages)

- 🏆 Superior Financial Strength: Holds an A++ (Superior) rating from AM Best, ensuring 100% reliability in paying out claims, even during major disasters.

- 💰 Excellent Discount Stacking: Offers massive savings for bundling (Home + Auto), good students, and safe drivers.

- 🚗 Premier New Car Replacement®: Industry-leading add-on that replaces a totaled new car with a brand-new one for up to 5 years (most competitors only offer 1-2 years).

- 📱 IntelliDrive® Savings: Safe drivers can save up to 30% at renewal by tracking their driving habits for 90 days via the smartphone app.

- 🛠️ ConciergeClaim® Network: Offers a lifetime workmanship warranty and direct billing if you use their certified repair shops.

❌ Cons (Disadvantages)

- ⚠️ Telematics Penalties: Unlike some competitors, the IntelliDrive app can actually increase your premium in certain states if it records bad driving habits (like hard braking or late-night driving).

- 📉 Average Customer Satisfaction: Ranks slightly average in some regional J.D. Power claims satisfaction and customer service studies compared to top-tier rivals.

- 🛑 Discount Caps: Even if you qualify for 10 different discounts, Travelers enforces a strict maximum discount cap (usually between 35% to 45%).

- 📞 Agent Reliance: While the digital app is good, purchasing specific policies or making complex endorsements often requires talking to an independent local agent rather than doing it 100% online.

Summary: Travelers is a fantastic choice for safe drivers, homeowners looking to bundle, and buyers of brand-new cars, but it may not be the best fit for night-shift workers or drivers with poor driving records.

Car Insurance Company Comparison with Travelers Car Insurance: All You Need to Know

America’s “Top 20 Giants” (The Big 20)

This group controls over 95% of the entire US auto insurance market.

“The Ultimate Travelers Car Insurance Coverage Matrix: From Essential Liability to Premium Add-Ons”

1. Essential Liability Coverage (Mandatory)

- Bodily Injury Liability (BIL)

- Coverage: Pays third-party medical bills, rehab, and legal fees if you cause an accident.

- Limits: Ranging from state minimums to $500k/$1M.

- Conclusion: Never carry just the state minimum; high court awards can drain your personal assets.

- Property Damage Liability (PDL)

- Coverage: Pays for damage you cause to someone else’s property (vehicles, fences, buildings).

- Limits: $10,000 to $250,000+.

- Conclusion: Carry at least $100k to cover potential collisions with expensive EVs or luxury cars.

2. Vehicle Physical Damage Coverage

- Collision Coverage

- Coverage: Pays to repair your own car after hitting another vehicle or object, regardless of fault.

- Deductibles: $250 to $2,500.

- Conclusion: Choosing a higher deductible (e.g., $1,000) significantly lowers your monthly premium.

- Comprehensive Coverage

- Coverage: Pays for non-collision damage, including theft, fire, vandalism, hail, and animal strikes.

- Deductibles: $100 to $1,500.

- Conclusion: Hitting a deer falls under Comprehensive, not Collision.

3. Medical & Uninsured Driver Protection

- Uninsured/Underinsured Motorist (UM/UIM)

- Coverage: Covers your medical and repair bills if hit by an uninsured or hit-and-run driver.

- Limits: Usually matches your BIL limits.

- Conclusion: Essential protection, as roughly 1 in 8 US drivers hit the road without insurance.

- Medical Payments (MedPay)

- Coverage: Pays immediate medical costs (ambulance, X-rays) for you and your passengers, regardless of fault.

- Limits: $1,000 to $10,000 per person (no deductible).

- Conclusion: Kicks in instantly, bypassing high health insurance deductibles.

- Personal Injury Protection (PIP)

- Coverage: Covers medical bills, plus lost wages, childcare, and funeral costs.

- Limits: Mandated by state law (required in “No-Fault” states like NY, FL, MI).

- Conclusion: If allowed by your state, designating PIP as “secondary” to your primary health insurance can save money.

4. Travelers Specialty Add-Ons

- Premier New Car Replacement®

- Coverage: Replaces a totaled new car with a brand-new exact match, zero depreciation deducted.

- Eligibility: Valid for the first 5 years of ownership.

- Conclusion: A major Travelers advantage; most competitors only offer this for 1 to 2 years.

- Loan/Lease Gap Insurance

- Coverage: Pays the financial gap between your totaled car’s actual cash value (ACV) and your remaining bank loan.

- Eligibility: Crucial for 60-72 month loans or low down payments.

- Conclusion: Prevents you from making monthly payments on a car that no longer exists.

- Rideshare Coverage

- Coverage: Protects gig drivers during “Period 1” (app is on, but waiting for a ride request).

- Eligibility: Designed for Uber, Lyft, and DoorDash drivers.

- Conclusion: Personal auto policies and standard app insurance drop coverage during this specific gap; this prevents denied claims.

“How to Maximize Your Savings: The Ultimate Travelers Car Insurance Discount Guide”

1. Policy Bundling

- Multi-Policy Discount: Link your auto insurance with Travelers home, renters, condo, or umbrella coverage.

- Estimated Savings: Up to 10–15% on Auto and 5–20% on Home.

- Conclusion: Even if a driver does not own a home, buying a cheap $15/month Renters policy often pays for itself via the auto discount it triggers.

2. Household & Fleet

- Multi-Car Discount: Insure two or more vehicles at the same primary residence on one master policy.

- Estimated Savings: 8–12%.

- Conclusion: Always add a teen driver’s vehicle to the parents’ policy rather than buying a standalone policy.

3. Driving History

- Safe Driver / Accident-Free Credit: No at-fault accidents, DUIs, or major speeding tickets in the past 3 to 5 years.

- Estimated Savings: 10–25%.

- Conclusion: Ask your agent about the “Responsible Driver Plan” to lock in Minor Violation Forgiveness so one small mistake does not erase this massive discount.

4. Youth & Education

- Good Student Discount: Full-time students (ages 16–25) maintaining a 3.0 (B) GPA or higher.

- Estimated Savings: 8–15%.

- Conclusion: Submit a fresh transcript at every policy renewal to keep this discount active until age 25.

- Student Away at School Discount: Students attending college 100+ miles away from home without a vehicle.

- Estimated Savings: 5–10%.

- Conclusion: This can be stacked with the Good Student Discount to cut a young driver’s premium nearly in half.

5. Vehicle Safety & Technology

- Anti-Theft Device Credit: Factory-installed alarms, immobilizers, or active GPS trackers (like LoJack).

- Estimated Savings: 3–15% (applied to Comprehensive coverage).

- Conclusion: Installing an aftermarket GPS tracker often pays for itself in the first year through this premium drop.

- Hybrid / Electric Vehicle (EV) Credit: Owning an eco-friendly Hybrid, PHEV, or full EV.

- Estimated Savings: Up to 5%.

- Conclusion: This discount helps offset the traditionally higher collision repair costs associated with EVs.

- Anti-Lock Brakes & Airbag Credits: Standard safety tech like ABS and passenger/curtain airbags.

- Estimated Savings: 2–5% (applied to MedPay/PIP coverage).

- Conclusion: Standard on post-2010 cars, but owners of older vehicles must ensure the agent manually logs these features.

6. Driver Training

- Defensive Driving Course: Completing a state-approved safe driving class (popular for teens and seniors).

- Estimated Savings: 5–10% (valid for 3 years).

- Conclusion: A $30 online, 4-hour course will consistently lower rates for 36 consecutive months.

7. Financial & Payment Planning

- Paid-in-Full Discount: Paying the entire 6-month or 12-month premium upfront.

- Estimated Savings: 5–7.5%.

- Conclusion: Paying in full also eliminates the hidden $2–$7 monthly installment fees charged by most insurers.

- EFT / Paperless Billing: Setting up auto-pay via a checking account and opting out of physical mail.

- Estimated Savings: 2–5%.

- Conclusion: Combine this with the Paid-in-Full discount for maximum baseline savings and zero risk of late fees.

8. Time & Quoting Strategy

- Early Quote Advantage: Requesting an insurance quote 3 to 15 days before you need the policy to activate.

- Estimated Savings: 3–11%.

- Conclusion: Never buy insurance on the exact day you need it. Planning just one week ahead triggers an automatic price drop.

9. Telematics (Usage-Based)

- IntelliDrive® Participation: Allowing a smartphone app to track driving habits (speed, braking, phone use) for 90 days.

- Estimated Savings: Up to 10% just for enrolling, plus up to 30% at renewal for safe driving.

- Conclusion: Highly recommended for remote workers and low-mileage drivers, but aggressive drivers should avoid it, as poor scores can increase premiums in certain states.

10. Customer Loyalty

- Continuous Coverage Credit: Maintaining auto insurance with zero lapses, even if transferring from a competitor like GEICO.

- Estimated Savings: 5–7%.

- Conclusion: Ensure exact time overlap when switching carriers. Even a 1-day lapse voids this discount and flags you as a “high-risk” driver.

The Ultimate Discount Stacking Strategy

It is impossible to stack discounts to achieve a “zero dollar” premium. Travelers enforces a Maximum Discount Cap, which varies by state but typically maxes out between 35% and 45%.

Case Study Example: If a 22-year-old student stacks the Multi-Policy (12%), Good Student (10%), Early Quote (5%), and EFT Auto-Pay (3%) discounts, a standard $2,000 annual premium can drop to roughly $1,400.

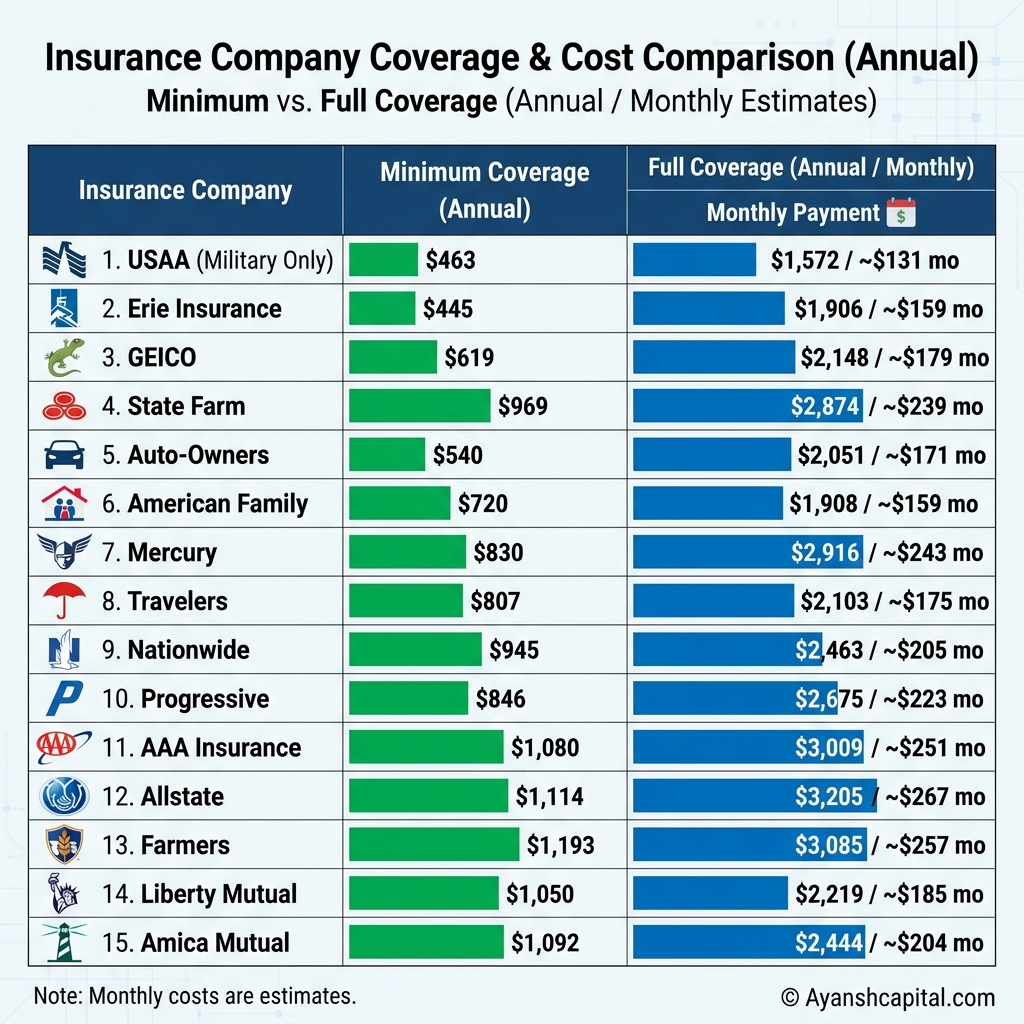

Full Coverage Top 15 Auto Insurance Rate Comparisons

Below is a detailed breakdown of Top 15 Car Insurance average annual rates for full coverage auto insurance across various driver profiles, compared directly against the national average.

Top 15 Car Insurance Rates by Age & Experience

In the auto insurance industry, age and driving experience heavily dictate your premium. As you gain experience and your statistical risk of accidents decreases, Top 15 Car Insurance Rates by Age & Experience. Here is a quick breakdown of how age impacts your premium:

“The Ultimate Travelers Car Insurance App Audit: Navigating the Digital Ecosystem, Hidden Bugs, and Tech Hacks”

1. MyTravelers® Master Portal

- Functionality: Full policy management, digital auto ID access, and biometric login (FaceID/TouchID).

- User Benefit: 100% paperless management; access digital ID cards offline during police stops.

- Cons & Bugs: Occasional login errors during late-night Sunday server maintenance.

- Conclusion: Integrate your digital ID with Apple Wallet or Google Wallet for instant access without opening the app.

2. IntelliDrive® Performance Tracker

- Functionality: Uses smartphone telematics (GPS, gyroscope) to track driving habits for 90 days.

- User Benefit: Earn up to a 30% premium discount at renewal for safe driving.

- Cons & Bugs: Drains phone battery 15–20% faster; poor scores can increase premiums in certain states.

- Conclusion: Do not use this app if you work night shifts. The algorithm heavily penalizes driving between 12 AM and 4 AM.

3. AI-Powered Photo Claims Tool

- Functionality: Guided 3D photography that uses AI to analyze vehicle damage and estimate repair costs.

- User Benefit: Receive initial repair estimates in hours without waiting days for a physical adjuster.

- Cons & Bugs: Rejects photos taken in extreme low light or if the vehicle is heavily covered in mud.

- Conclusion: Always take claim photos in daylight with both close-up and wide-angle shots to ensure first-time AI approval.

4. Roadside Assistance Tracker 2.0

- Functionality: Uber-style geolocation dispatching that displays the tow truck’s vendor name, phone number, and live ETA.

- User Benefit: Provides peace of mind and exact timelines during stressful breakdowns.

- Cons & Bugs: Live map tracking can freeze in rural dead zones with weak cellular coverage.

- Conclusion: Always request help via the app rather than calling, as it sends your exact GPS coordinates directly to the driver.

5. Paperless Billing & EFT Configurator

- Functionality: Links checking accounts for auto-debit and switches all documentation to digital.

- User Benefit: Eliminates $3–$7 monthly installment fees and triggers an immediate premium discount (up to 3%).

- Cons & Bugs: Failed auto-pays due to insufficient funds trigger both a late fee and an NSF fee ($25–$35).

- Conclusion: Always link a checking account routing number instead of a debit/credit card to prevent failed payments when a card expires.

6. Instant Quote & VIN Scanner

- Functionality: Uses the smartphone camera to scan a vehicle’s barcode/VIN for a 60-second quote.

- User Benefit: Check exact insurance rates on the dealership lot before finalizing a car purchase.

- Cons & Bugs: Fails on pre-1981 vehicles that lack modern barcodes (requires manual entry).

- Conclusion: Scan the car and request the quote at least 5 days before buying to unlock the 10% “Early Quote Advantage” discount.

7. ConciergeClaim® Repair Locator

- Functionality: GPS-based directory of Travelers-certified network repair shops.

- User Benefit: Guaranteed lifetime warranty on repairs done at network facilities.

- Cons & Bugs: Limited or zero network shop availability in highly rural counties.

- Conclusion: Using a network shop ensures Travelers pays for “hidden” supplemental damages directly to the mechanic with zero pushback.

8. Digital Policy Endorsement Engine

- Functionality: 24/7 self-service portal to add drivers, change limits, or adjust deductibles.

- User Benefit: Instantly generates a new Declarations Page without waiting for agent business hours.

- Cons & Bugs: Cannot process complex legal requirements (like SR-22 filings).

- Conclusion: If leaving your car garaged for a long vacation, use this tool to temporarily drop Collision coverage and slash your premium.

9. Virtual Assistant Emma (AI Chatbot)

- Functionality: NLP-based chatbot designed to answer basic billing and policy questions instantly.

- User Benefit: Bypasses long customer service phone queues for simple queries.

- Cons & Bugs: Struggles with complex legal inquiries (like subrogation status) and creates loops.

- Conclusion: Type “Live Agent” or “Representative” immediately to bypass the bot and connect with a human.

10. Family Driver Safety Dashboard

- Functionality: A master screen showing IntelliDrive scores for all household drivers.

- User Benefit: Excellent tool for parents to monitor teen driving habits and enforce safety.

- Cons & Bugs: Teens may perceive the tracking as an invasion of privacy.

- Conclusion: Gamify the experience by creating a safe-driving competition among family members to secure a household-wide 30% discount.

Deep Dive: The Science Behind the App

The Actuarial Math of Braking

- The Metric: The Travelers AI defines “hard braking” as decelerating more than 7 mph in 1 second.

- The Risk: Actuarial data shows drivers with 3+ hard brakes daily are 400% more likely to crash within 6 months.

- Conclusion: Stop tailgating. Leaving ample following distance is the easiest way to prevent algorithm-damaging hard stops.

Distracted Driving & Data Privacy

- The Metric: The app tracks your phone’s internal gyroscope and screen-on status when traveling over 10 mph.

- The Reality: Travelers is not reading your texts or recording calls. It only detects if the phone is physically handled while in motion.

- Conclusion: Interacting with a dashboard mount or using hands-free Bluetooth audio will not hurt your score. Keep the phone out of your hands.

Exceptional Financial Strength & Solvency Ratings

This data confirms that Travelers operates with minimal default risk and holds massive liquid cash reserves to pay out claims during catastrophic events or economic downturns.

- AM Best: A++ (Superior). This is the highest possible rating, maintained consistently for 15 years. It guarantees that the company has a virtually zero default risk and can easily pay claims even during mega-crises like Category 5 hurricanes.

- S&P Global & Fitch Ratings: AA (Very Strong). Both agencies highlight the company’s exceptional long-term debt security and claims-paying ability. Travelers remains financially stable regardless of stock market crashes or volatility.

- Moody’s Investors Service: Aa2. Reflects minimal credit risk and high-quality fixed-income obligations, making Travelers a highly trustworthy choice for long-term policyholders.

- Solvency Capital Ratio: 210% to 225%. The company holds more than double the legally required minimum cash reserves, meaning billions of dollars are kept in liquid surplus for immediate claim settlements.

- Weiss Ratings & Fortune 500: Graded A- (Excellent) by independent auditors, proving financial self-sufficiency. As a top 100 Fortune 500 company (and part of the Dow Jones), Travelers generates over $41 billion in annual revenue with an 8% steady year-over-year growth.

Customer Satisfaction & Market Integrity

Beyond financial power, Travelers demonstrates a strong track record in customer service, dispute resolution, and claims handling compared to industry standards.

- NAIC Complaint Index: 0.62. This is the most critical consumer metric. With the national industry average set at 1.00, a score of 0.62 means Travelers receives nearly half the complaints of an average insurer, indicating extremely high customer satisfaction.

- J.D. Power (Auto Claims Satisfaction): 871 / 1000. Travelers scores above the national average for its smooth and highly digital claims process. The score recently improved by 12 points following major app updates.

- Better Business Bureau (BBB): A+ Rating. This top-tier grade confirms the company’s professional integrity. It highlights Travelers’ internal commitment to resolving customer disputes swiftly and fairly without the need for court intervention.

Travelers Car Insurance (50-State)

Travelers Car Insurance Extra Charges: What’s Really Increasing Your Premium?

1. Administrative & Billing Fees

- Installment Premium Fee

- Cost: $1 to $10 per payment.

- Trigger: Paying your premium in monthly installments rather than upfront.

- Conclusion: Select the “Paid-in-Full” option or set up EFT Auto-Pay to reduce this fee to zero or a minimal amount.

- Late Payment Surcharge

- Cost: $10 to $30 (varies by state laws).

- Trigger: Missing the premium due date and entering the grace period.

- Conclusion: Set up Automatic EFT Authorization scheduled for two days after your payday to ensure sufficient funds.

- Paper Statement Fee

- Cost: $1 to $5 per mailing.

- Trigger: Requesting physical, mailed copies of bills and ID cards.

- Conclusion: Select the “Go Paperless” option in the MyTravelers app to eliminate this administrative cost and trigger a paperless discount.

- Non-Sufficient Funds (NSF) / Bounced Check Fee

- Cost: $25 to $40 per failed transaction.

- Trigger: The auto-pay system attempts a withdrawal, but your bank account is overdrawn.

- Conclusion: Set low-balance alerts on your bank account and keep your credit card expiration dates updated in the digital portal.

- New Policy Underwriting Fee

- Cost: $15 to $35 (one-time setup fee).

- Trigger: Creating a new account, which covers the cost of pulling your official MVR (driving record) and CLUE (claims history) reports.

- Conclusion: This fee cannot be waived, but you can neutralize the financial impact by securing the 10% Early Quote Advantage discount.

- Policy Endorsement Surcharge

- Cost: $0 to $15 administrative fee.

- Trigger: Calling an agent to manually make policy changes, such as adding a vehicle or changing coverage limits.

- Conclusion: Always use the MyTravelers digital endorsement engine for minor updates; self-service changes are processed with a $0 admin fee.

2. Penalty & Claims-Related Surcharges

- Early Cancellation / Short-Rate Penalty

- Cost: 10% of the remaining premium or a $50 flat fee.

- Trigger: Canceling your policy mid-term to switch to a competitor.

- Conclusion: Never switch insurers in the middle of a policy term. Always shift to a new company exactly on your renewal date.

- Policy Reinstatement Penalty

- Cost: $25 to $100.

- Trigger: Re-activating a policy that was officially canceled due to non-payment.

- Conclusion: Never let your policy lapse. If you face financial hardship, submit a written request for a “Payment Deferral” instead of missing the payment.

- SR-22 / Certificate of Financial Responsibility Fee

- Cost: $15 to $50 (one-time filing fee).

- Trigger: Court or state DMV mandates a financial responsibility filing after a severe violation (e.g., DUI, driving without insurance).

- Conclusion: If an SR-22 is legally required, ask a Travelers agent to file it electronically to avoid expensive third-party broker processing fees.

- Out-of-Network Claims Handling Surcharge

- Cost: Variable out-of-pocket difference.

- Trigger: Using an independent mechanic whose labor rates exceed the Travelers “reasonable and customary” payout limits.

- Conclusion: Always select a Travelers-certified ConciergeClaim® network garage to avoid out-of-pocket labor differences and secure a lifetime workmanship guarantee.

How the Travelers Car Insurance IntelliDrive Scoring System Really Works

1. Hard Braking (40% Weight – Highest Impact)

- Critical Threshold: A speed drop of more than 7 mph per second.

- Mitigation Hack: Maintain a 3-second following distance and anticipate traffic lights to let your car decelerate naturally.

2. Time of Day (20% Weight – High Risk)

- Critical Threshold: Driving between 12:00 AM (Midnight) and 4:00 AM.

- Mitigation Hack: Avoid driving during these hours entirely. If you work night shifts, consider opting out of the telematics program.

3. Rapid Acceleration (15% Weight)

- Critical Threshold: A speed increase of more than 8 mph per second.

- Mitigation Hack: Avoid “jack-rabbit” starts at green lights; accelerate gradually and smoothly.

4. Distracted Driving (15% Weight)

- Critical Threshold: Unlocking, touching, or handling your phone while driving faster than 10 mph.

- Mitigation Hack: Set your GPS and music before putting the car in drive. Keep the phone secured on a dash mount and strictly use voice commands (Siri/Google Assistant).

5. Speeding Limits (10% Weight)

- Critical Threshold: Consistently driving 10 to 15 mph over the posted local speed limit.

- Mitigation Hack: Rely on cruise control on highways to lock your speed and prevent accidental speeding.

6. Cornering Intensity (5% Weight)

- Critical Threshold: Generating a lateral force greater than 0.3G during a turn.

- Mitigation Hack: Decelerate at least 50 meters before reaching an intersection or curve. Do not brake or accelerate sharply mid-turn.

7. Continuous Rolling Stops (5% Weight)

- Critical Threshold: Rolling through a STOP sign at 2 to 5 mph instead of coming to a 0 mph stop.

- Mitigation Hack: Come to a complete, absolute stop at every sign and count to 2 seconds before moving forward.

8. Total Mileage Exposure (Informal Modifier)

- Critical Threshold: Driving more than 5,000 miles within the 90-day tracking window.

- Mitigation Hack: High mileage amplifies the penalty for minor driving errors. If taking a cross-country road trip, drive with extreme caution, as the algorithm heavily penalizes mistakes over long distances.

9. Route Risk Surcharge (Sensor-Assisted)

- Critical Threshold: Frequent driving in high-density urban cores or high-crash intersections.

- Mitigation Hack: When possible, choose alternative routes with fewer traffic lights and stop signs to naturally reduce the chance of hard braking.

10. Passenger Distraction (False Positives)

- Critical Threshold: The app accidentally records phone handling when you are sitting in the passenger seat or taking public transit.

- Mitigation Hack: Open the app and manually change the specific trip’s label to “I was the Passenger.” Travelers will automatically erase the negative score from your record within 24 hours.

The Impact of Driving Violations on Premiums: A Comprehensive Breakdown

The Ultimate Travelers Car Insurance Exclusions Guide: Policy Gaps, Triggers & Mitigation Strategies

- Commercial & Gig-Work Use

- Exclusion: Using a personal vehicle for Uber, Lyft, DoorDash, or Amazon Flex.

- Actuarial Reason: Commercial use increases road exposure and crash risk by 400%.

- Financial Danger: Immediate claim denial and policy cancellation.

- Strategic Solution: Add a Rideshare Coverage Endorsement ($10–$20/month) or purchase a dedicated Commercial Auto Policy.

- Unlisted Household Residents

- Exclusion: Accidents caused by unlisted roommates or family members living at your address.

- Actuarial Reason: Underwriters cannot accurately assess household risk if drivers are hidden.

- Financial Danger: Claim rejection due to “Material Misrepresentation.”

- Strategic Solution: List all licensed household members on the policy. If they never drive your car, list them as “Excluded Drivers” to prevent premium hikes.

- Illegal Acts & Street Racing

- Exclusion: Street racing, evading law enforcement, or using the car in a crime.

- Actuarial Reason: Insuring illegal acts violates public policy; racing carries a 99% crash probability.

- Financial Danger: $0 payout and Travelers will not provide legal liability defense.

- Strategic Solution: Drive legally and never participate in unauthorized racing events.

- DUI / DWI Property Damage

- Exclusion: Wrecking your own vehicle while driving under the influence of drugs or alcohol.

- Actuarial Reason: In select states, underwriting clauses allow insurers to deny physical damage payouts to an at-fault impaired driver.

- Financial Danger: Travelers may deny the Collision/Comprehensive claim for your own vehicle.

- Strategic Solution: Never drink and drive; utilize rideshare services.

- Unlicensed or Suspended Driving

- Exclusion: Handing your keys to a driver with a suspended, revoked, or non-existent license.

- Actuarial Reason: Violates the fundamental contract condition that operators must be legally licensed.

- Financial Danger: Travelers may pay the victim but will use subrogation to sue you personally for the entire cost.

- Strategic Solution: Always verify the active license status of any friend or relative borrowing your car.

2. Mechanical, Legal & Systemic Exclusions

- Wear & Tear / Mechanical Breakdown

- Exclusion: Engine seizure, transmission failure, worn brakes, or a dead battery.

- Actuarial Reason: Auto insurance strictly covers “sudden and accidental” events, not routine aging or poor maintenance.

- Financial Danger: $0 payout for mechanic labor or replacement parts.

- Strategic Solution: Purchase a separate Mechanical Breakdown Insurance (MBI) plan or an extended third-party warranty.

- Intentional Acts & Fraud

- Exclusion: Intentionally crashing the car, arson, or staging fake accidents.

- Actuarial Reason: Violates the principle of utmost good faith; insurance is designed for unexpected losses, not illegal profit.

- Financial Danger: $0 payout, immediate policy cancellation, and criminal prosecution by the Special Investigation Unit (SIU).

- Strategic Solution: Only file 100% legitimate and truthful claims.

- Commercial Cargo & Hazardous Hauling

- Exclusion: Transporting heavy commercial goods, explosives, or highly flammable chemicals.

- Actuarial Reason: Personal policies only underwrite the risk of standard passengers and everyday personal items.

- Financial Danger: Total denial of Comprehensive/Collision claims if the cargo causes or exacerbates the damage.

- Strategic Solution: Purchase an In-Transit Cargo Endorsement or upgrade to a commercial policy.

- Seizure & Government Confiscation

- Exclusion: Vehicle is impounded, seized, or destroyed by customs, police, or government agencies.

- Actuarial Reason: Reimbursing losses resulting from lawful government actions violates public policy.

- Financial Danger: $0 payout for any damage sustained while the car is in a police impound lot.

- Strategic Solution: Obey local laws. If a government agency damages the car unlawfully, you must file a Government Tort Claim against that specific department.

- War, Riot & Nuclear Risks

- Exclusion: Damage from acts of war, civil unrest, military coups, or nuclear radiation.

- Actuarial Reason: These are “Catastrophic Systemic Risks” that no private insurer has the actuarial capacity to cover.

- Financial Danger: Travelers is not financially liable for these systemic events.

- Strategic Solution: Financial relief in these scenarios relies entirely on federal emergency management funds.

Travelers Car Insurance Claims Process: Step-by-Step Lifecycle, Subrogation & Total Loss Guide

1. On-Scene Actions

- Your Action: Move to a safe lane, check for injuries, and take 360-degree photos. Do not admit fault.

- Travelers Action: System awaits your emergency roadside call or app ping.

- Timeline: 0 to 60 minutes.

2. Claim Reporting (First Notice of Loss)

- Your Action: File via the MyTravelers® app or call 1-800-CLAIM33.

- Travelers Action: AI generates a Claim Number and assigns a dedicated Claim Professional.

- Timeline: Within 24 to 48 hours.

3. Initial Review & Assignment

- Your Action: Provide a recorded statement and your policy declarations page.

- Travelers Action: Adjuster verifies active coverage and deductible limits.

- Timeline: 24 to 48 business hours.

4. Liability Investigation

- Your Action: Answer supplemental questions and provide the police crash report.

- Travelers Action: Adjuster determines fault (0% to 100%) based on state traffic laws and evidence.

- Timeline: 2 to 7 business days.

5. Fraud Investigation (SIU Audit – Conditional)

- Your Action: Cooperate fully and provide medical or maintenance history if requested.

- Travelers Action: Special Investigation Unit (SIU) audits the claim if red flags appear.

- Timeline: Adds 15 to 30 days.

6. Damage Appraisal

- Your Action: Take the car to a network garage or submit AI photo estimates via the app.

- Travelers Action: In-house appraiser estimates labor and parts costs.

- Timeline: 1 to 3 days after photo submission.

7. Total Loss Valuation (Conditional)

- Your Action: Hand over the car title, keys, and loan pay-off statement.

- Travelers Action: Declares a total loss if repairs exceed 70%-80% of the Actual Cash Value (ACV). Pays the lender via Gap Insurance if applicable.

- Timeline: 5 to 10 days for the valuation report.

8. Repair & Rental Management

- Your Action: Pay your deductible to the shop and pick up a rental car (if covered).

- Travelers Action: Approves repairs and sets up direct billing for the rental car.

- Timeline: 3 to 14 days (repair duration).

9. Final Settlement

- Your Action: Sign the release form and pick up the repaired vehicle.

- Travelers Action: Issues direct Electronic Funds Transfer (EFT) to the repair shop or a check to you/your lender.

- Timeline: 24 to 48 hours after bill approval.

10. Subrogation (Background Action)

- Your Action: No action required.

- Travelers Action: Legal team sues the at-fault driver’s insurance to recover costs. If successful, Travelers refunds your out-of-pocket deductible.

- Timeline: 3 months to 1 year.

Subrogation & Total Loss: Critical Nuances

Subrogation: Getting Your Deductible Back

- The Process: Travelers pays your repair bill (minus your deductible) and legally pursues the at-fault driver’s insurer (e.g., GEICO, Progressive).

- The Result: Once Travelers recovers the full claim amount from the opposing insurer, they are legally obligated to refund your deductible.

- Actionable Advice: Stay in contact with your subrogation adjuster via email to track your refund status.

Total Loss & Actual Cash Value (ACV)

- The Reality: Insurance pays the current market value (ACV) based on age, mileage, and pre-crash condition, using software like CCC ONE.

- The Math: If your car is worth $12,000 but needs $10,000 in chassis and engine repairs, it will be totaled. Travelers sells the salvage to recover costs.

- Actionable Advice: Carry the Premier New Car Replacement clause to avoid massive financial hits when a newer vehicle is totaled.

How to Cancel Travelers Car Insurance: Step-by-Step

- 1. Buy a New Policy First: Always activate your new auto insurance before canceling your Travelers policy. Even a one-day lapse in coverage can significantly increase your future insurance rates and is illegal in most states.

- 2. Gather Your Information: Before calling, have your policy number, your name/date of birth, and the exact effective date you want the cancellation to take place.

- 3. Contact Travelers Directly:

- You cannot cancel your policy online through the portal or the app.

- Call Travelers direct customer service at 1-800-842-5075.

- Alternatively, you can call the local independent agent who originally sold you the policy.

- 4. Ask About Cancellation Fees: Travelers generally does not charge a cancellation fee, but it is always best to ask the representative to confirm there are no hidden “short-rate” penalties in your specific state.

- 5. Request Written Confirmation: Ask the agent to send an email or a formal letter stating that your policy has been successfully canceled. Keep this document as proof for the DMV or your new insurer.

- 6. Monitor for a Refund: If you paid your 6-month or 12-month premium upfront, Travelers will issue a prorated refund (via check or back to your original payment method) for the unused days remaining on your policy. Ensure your auto-pay is permanently turned off.

How to Get an Auto Insurance Quote from Travelers

- 1. Online Portal (Travelers.com)

- Process: Visit Travelers.com directly and enter your ZIP code, vehicle identification number (VIN), and driver’s license details.

- Timeline: Generates an official, highly accurate online quote within a few minutes.

- 2. Independent Local Agents

- Process: Use the “Find an Agent” tool on the Travelers website to connect with a local insurance professional.

- Benefit: Access Travelers’ vast network of over 13,500 independent agents who can manually uncover and stack location-specific discounts.

- 3. Toll-Free Phone Call

- Process: Call the direct Travelers customer service line at 1-800-842-5075.

- Benefit: Speak directly with an insurance representative to fully customize your liability limits, deductibles, and coverages.

- Conclusion: Never wait until the last minute to shop for a policy. Request your quote 7 to 15 days before your current insurance coverage expires to automatically unlock the Early Quote Advantage discount, slashing up to 10% off your baseline premium.

Auto Insurance Add-Ons That Waste Money (Drop These for Maximum Savings)

When customizing your car insurance policy, you can save a significant amount of money annually by removing the following add-ons:

- 1. Roadside Assistance

- What it is: Covers towing and mechanic services if your car breaks down on the road, gets a flat tire, or has a dead battery.

- When to drop it: If you already have an AAA (American Automobile Association) membership, get it as a free perk with your premium credit card, or if it is already included in your new car’s manufacturer warranty.

- Reason for saving: Paying your insurance company for a service you already have elsewhere is just a waste of money. Drop it to avoid double-paying.

- 2. Rental Reimbursement

- What it is: Covers the daily cost of a rental car so you can commute to work while your vehicle is in the auto shop for crash repairs.

- When to drop it: If you have an extra car available at home, work entirely from home (WFH), or can easily rely on public transit (bus/subway).

- Reason for saving: If you do not strictly need a car every single day, remove this pricey add-on from your policy.

- 3. Gap Insurance

- What it is: If your car is declared a total loss or stolen, this covers the “gap” (difference) between your car’s current market value and the remaining balance on your auto loan.

- When to drop it:

- If you have paid off the car entirely (meaning you have no auto loan).

- If you made a massive down payment and your remaining loan balance is now less than the car’s current market price (Actual Cash Value).

- Reason for saving: In these situations, Gap insurance provides zero financial benefit; keeping it is completely useless.

- 4. Overlapping Medical Coverage (MedPay / PIP)

- What it is: Covers hospital bills, X-rays, and medical expenses for you and your passengers if injured in a crash, regardless of who is at fault.

- When to drop it (or reduce it): If you already have excellent personal health insurance (through your employer or individually) with a very low deductible.

- Reason for saving: In the event of an accident, your primary health insurance plan will cover your medical bills anyway. Therefore (if your state laws allow it), lower your MedPay or PIP (Personal Injury Protection) coverage to the state minimum to reduce your monthly premium.

Comprehensive Travelers Car Insurance FAQ

1. What is Travelers’ official financial strength rating?

- Answer: Travelers holds an A++ (Superior) rating from AM Best and an AA (Very Strong) rating from S&P Global. This indicates a rock-solid financial foundation with an exceptional capacity to pay out claims.

2. What is the financial danger of carrying only state minimum liability limits?

- Answer: If a court ruling or medical bills exceed your low minimum limits, your personal assets (savings, home) can be legally seized to pay the difference. Carrying at least $100k/$300k limits is highly recommended.

3. How does the Premier New Car Replacement® add-on work?

- Answer: If your new vehicle is declared a total loss within the first 5 years or 60,000 miles, Travelers replaces it with a brand-new exact match, deducting zero depreciation.

4. Can I stack all available discounts to achieve a $0 premium?

- Answer: No. Travelers enforces a strict Maximum Discount Cap that varies by state but typically limits total combined savings to between 35% and 45% of your baseline premium.

5. Can a bad score on the IntelliDrive® telematics app raise my rates?

- Answer: Yes. While enrolling gives an immediate 10% discount, risky habits—such as hard braking or consistently driving between 12 AM and 4 AM—can actually increase your premium at renewal in select states.

6. What is the First Notice of Loss (FNOL) timeline for filing a claim?

- Answer: You should officially file your claim within 24 to 48 hours of an accident via the MyTravelers® app or by calling 1-800-CLAIM33 to prevent fraud flags and processing delays.

7. How does subrogation help me get my deductible back?

- Answer: When you are hit by an at-fault driver, Travelers pays for your repairs (minus your deductible) and legally pursues the opposing insurer. Once they recover the funds, Travelers refunds your out-of-pocket deductible.

8. Are gig-work delivery and rideshare apps covered under a personal policy?

- Answer: No. Driving for Uber, Lyft, DoorDash, or Amazon Flex is an absolute commercial exclusion. Fulfilling these roles without a Rideshare Endorsement results in immediate claim denial.

9. What is the biggest advantage of using a ConciergeClaim® repair shop?

- Answer: Network shops provide direct billing, seamless rental car coordination, and a lifetime workmanship warranty on all repairs for as long as you own the vehicle.

10. How can I completely eradicate monthly administrative installment fees?

- Answer: You can eliminate the $1 to $10 monthly installment charges by selecting the Paid-in-Full option upfront or by linking a checking account via EFT Auto-Pay.