GEICO Car Insurance: How to Save Hundreds on Your Premium

GEICO Car Insurance is currently one of the most recognized auto insurance companies in the United States and around the world. If you are looking for reliable, affordable, and customer-friendly coverage for your vehicle, GEICO is often the first name that comes to mind. In this comprehensive blog post, we will break down every aspect of GEICO auto insurance—from its coverage options and discounts to the claims process and customer reviews.

What is GEICO?

GEICO stands for Government Employees Insurance Company. It was founded in 1936 by Leo Goodwin and his wife, Lillian. Originally, the company’s goal was to provide insurance exclusively to U.S. government employees and military personnel. However, today it is a wholly-owned subsidiary of Warren Buffett’s Berkshire Hathaway and provides coverage to the general public.

GEICO’s mascot is a little green gecko, which has made its commercials wildly popular. You likely know them by their famous tagline:

“15 minutes could save you 15% or more on car insurance.”

The Good and the Bad: Is GEICO Right for You?

No auto insurance company is a perfect fit for everyone. Before making a decision, it is crucial to weigh the advantages and drawbacks to see if GEICO aligns with your needs.

The Advantages: Why Choose GEICO?

- Highly Affordable Rates: GEICO consistently offers premiums well below the industry average, making it an especially great choice for young and safe drivers.

- Industry-Leading Digital Experience: They feature a top-rated mobile app that allows you to seamlessly manage your policy, pay bills, and file claims entirely from your smartphone.

- Extensive Discount Options: You can stack massive savings through programs like the DriveEasy telematics app, as well as generous military and good student discounts.

- Unbeatable Financial Strength: Backed by Warren Buffett’s Berkshire Hathaway and boasting an A++ rating from A.M. Best, GEICO’s financial stability and ability to pay out claims is rock-solid.

The Drawbacks: Where GEICO Falls Short

- Lack of Local Agents: GEICO operates on a direct-to-consumer model. If you prefer building a relationship and discussing your policy face-to-face with a local agent, this company isn’t for you.

- No Traditional Gap Insurance: A major downside for drivers with leased or heavily financed cars is that GEICO does not offer standard Gap Insurance (though they do offer Mechanical Breakdown Insurance as an alternative).

- Average Claims Satisfaction: In J.D. Power auto claims studies, GEICO typically ranks strictly “average” or slightly above, trailing behind customer service leaders like USAA and Amica.

- Steep Rate Hikes for Bad Records: While they reward safe driving, GEICO is notoriously unforgiving if you have a poor driving record; your premiums will skyrocket if you get a DUI or have multiple at-fault accidents.

Car Insurance Company Comparison with GEICO Car Insurance: All You Need to Know

America’s “Top 20 Giants” (The Big 20)

This group controls over 95% of the entire US auto insurance market.

GEICO Car Insurance Industry Ratings & Performance Summary

1. Financial Strength & Customer Satisfaction

- A.M. Best (Financial Strength): A++ (Superior). Ranks in the top 1%; guarantees massive cash reserves, meaning GEICO can easily pay all claims even during widespread natural disasters.

- Standard & Poor’s (Corporate Stability): AA+ (Very Strong). Indicates a highly secure and profitable business model capable of withstanding economic inflation.

- Moody’s (Credit Rating): Aa1 (Excellent). Shows minimal debt and smart premium investments, ensuring long-term corporate survival.

- J.D. Power (Auto Claims Study): 874 / 1,000. Above average; customers report high satisfaction with agent support, garage services, and the speed of claim payouts.

- NAIC (Complaint Index): 0.78. Much better than the national average (1.0). This means GEICO receives an unusually low number of official complaints considering its massive size.

- Better Business Bureau (BBB): A+ Rating. Demonstrates excellent business ethics; the company actively works to resolve customer disputes rather than ignoring them.

- Consumer Reports (Value & Transparency): 82 / 100. Very good value for money; customers appreciate clear premium quotes with minimal hidden fees.

- Forbes Advisor (Overall Ranking): 4.5 / 5 Stars. Ranked in the Top 3 companies; named the “Best Budget Pick” for students, young drivers, and tech-savvy individuals.

🏆 Comprehensive Breakdown of GEICO Car Insurance Coverage

🤕 1. Bodily Injury Liability Bodily Injury Liability covers the medical bills, pain and suffering, and legal fees for the other party if you are found at fault in an accident. However, it strictly does not cover your own injuries or the medical bills of your passengers. This coverage remains legally mandatory in 49 states.

- GEICO Deductible: No

- Estimated Premium Cost: High

🚧 2. Property Damage Liability If you cause an accident, this policy covers the damage you inflict on someone else’s property—whether it is another vehicle, a house wall, a fence, or city infrastructure like a streetlamp. It does not cover any damage to your own vehicle. This is legally mandatory in almost every U.S. state.

- GEICO Deductible: No

- Estimated Premium Cost: Medium

💥 3. Collision Coverage This covers the repair costs for your own vehicle if it hits another car, a tree, or a pole, regardless of who is at fault. It does not cover theft, fire, weather damage, or medical expenses. Collision coverage is mandatory if your vehicle is currently financed (on an active auto loan) or leased through a dealership.

- GEICO Deductible: Yes (Policyholders typically select a deductible ranging from $50 to $1,000)

- Estimated Premium Cost: High

🌪️ 4. Comprehensive Coverage Comprehensive coverage handles vehicle damage not caused by a driving collision. This includes car theft, fire, flash floods, hail, or striking an animal like a deer. It strictly excludes collisions with other cars and routine wear and tear. It is mandatory for newly purchased cars and any financed/leased vehicles.

- GEICO Deductible: Yes (Typically set at $250 or $500)

- Estimated Premium Cost: Medium

🏥 5. Personal Injury Protection (PIP) PIP covers the medical bills for you and your passengers after an accident, along with lost wages and essential replacement services, entirely regardless of who was at fault. It does not cover damage to your car or the other party’s property. PIP is mandatory in ‘no-fault’ insurance states (such as Florida, New York, and Michigan).

- GEICO Deductible: Yes, depending on state-specific regulations (Optional)

- Estimated Premium Cost: Medium to High

⚕️ 6. Medical Payments (Med Pay) Med Pay specifically covers the immediate medical and surgical bills for you and your passengers, regardless of who caused the collision. Unlike PIP, it does not reimburse lost wages or long-term rehabilitation costs. It is highly recommended in states where PIP is not legally required or available.

- GEICO Deductible: No

- Estimated Premium Cost: Low

⚠️ 7. Uninsured Motorist Bodily Injury (UMBI) If you are injured by a driver who is driving illegally without insurance, or if you are the victim of a ‘hit-and-run’, UMBI covers your resulting medical bills. It does not cover physical damage to your vehicle. This coverage is legally mandatory in many states and heavily recommended nationwide given current uninsured driver rates.

- GEICO Deductible: No

- Estimated Premium Cost: Low to Medium

🚙 8. Uninsured Motorist Property Damage (UMPD) This policy covers the specific repair costs for your car if it is struck by an uninsured driver. It does not cover your medical bills. UMPD is highly recommended as a cost-saving strategy for drivers who drive older vehicles and choose not to carry standard ‘Collision’ coverage.

- GEICO Deductible: Yes (A smaller deductible applies in certain states)

- Estimated Premium Cost: Low

🛻 9. Emergency Roadside Assistance If your vehicle breaks down, this digital-first service (which can be dispatched via the GEICO mobile app) covers towing to the nearest facility, flat tire changes, jump-starts, and lockout services. You are, however, responsible for the actual cost of any replacement parts (e.g., paying for the physical battery itself). It is strongly recommended for older cars and high-mileage highway drivers.

- GEICO Deductible: No

- Estimated Premium Cost: Very Low

🔑 10. Rental Reimbursement This covers the daily cost of a rental car (coordinated directly with partners like Enterprise or Hertz) while your vehicle is in the auto shop for covered accident repairs. It does not cover renting a vehicle for personal vacations or leisure road trips. It is highly recommended for commuters who do not have access to a secondary backup vehicle.

- GEICO Deductible: No

- Estimated Premium Cost: Low

⚙️ 11. Mechanical Breakdown Insurance (MBI) Often serving as a cheaper alternative to dealer extended warranties, MBI covers sudden technical failures in your car’s engine, transmission, or electrical systems that are completely unrelated to an accident. It excludes routine maintenance (like oil changes or brake pad replacements). To qualify under current guidelines, the vehicle must be new (typically less than 15 months old with under 15,000 miles).

- GEICO Deductible: Yes (Requires a fixed $250 deductible per repair visit)

- Estimated Premium Cost: Low

📱 12. Rideshare Coverage This hybridized policy provides seamless protection for you and your vehicle while the ‘app is on’ and you are waiting for a request or driving for gig economy services like Uber, Lyft, or Amazon Flex. It bridges the gap between your personal policy and the commercial policy provided by the rideshare company. It is strictly mandatory for modern delivery and rideshare drivers.

- GEICO Deductible: Yes (Applies to the Collision/Comprehensive portion)

- Estimated Premium Cost: Medium

GEICO Car Insurance (50-State)

💰 How to Maximize Your Savings: A Complete Guide to GEICO Car Insurance Discounts

The biggest secret behind GEICO’s highly competitive rates lies in their extensive discount programs. The best part is that these discounts are usually “stackable”—meaning you can apply multiple discounts on top of one another to drastically reduce your total premium.

Below is a detailed breakdown of the savings, eligibility requirements, and application steps, organized to help you get the most out of your policy.

🚦 1. Driving Behavior & Habits

🛡️ Safe Driver Discount

- Estimated Savings: 22% to 26%

- Detailed Eligibility: You must have a clean driving record with no at-fault accidents or traffic violations (like speeding tickets) over the past 5 years.

- How to Apply: Automatically applied during the quoting process when GEICO checks your motor vehicle record.

📱 Drive Easy Program (Telematics)

- Estimated Savings: 5% to 25% (or more, depending on driving score)

- Detailed Eligibility: Requires you to download the GEICO app, which monitors your driving habits in real-time—including hard braking, cornering, and phone usage.

- How to Apply: You must opt into the program and keep the app installed and active on your smartphone.

🔒 2. Vehicle Safety & Security Features

🚨 Anti-Theft System Discount

- Estimated Savings: 2% to 25% (applies to the Comprehensive portion)

- Detailed Eligibility: Your vehicle must be equipped with a built-in alarm, active GPS tracker, or engine immobilizer.

- How to Apply: Usually identified automatically via your vehicle’s VIN (Vehicle Identification Number).

✨ New Vehicle Discount

- Estimated Savings: Up to 15%

- Detailed Eligibility: Your car must be three model years old or newer.

- How to Apply: Automatically verified using your vehicle registration details.

🎈 Air Bags and Anti-Lock Brakes (ABS) Discount

- Estimated Savings: 23% to 40% (applies specifically to the medical/PIP portion of your premium)

- Detailed Eligibility: Your car must have driver and passenger-side airbags, as well as factory-installed anti-lock brakes.

- How to Apply: Verified automatically based on your car’s factory features.

☀️ Daytime Running Lights Discount (Additional Discount)

- Estimated Savings: Up to 3%

- Detailed Eligibility: Your vehicle must be equipped with standard daytime running lights that turn on automatically.

- How to Apply: Verified through your vehicle’s VIN.

👥 3. Customer Profile & Affiliations

🚘 Multi-Car Discount

- Estimated Savings: Up to 25%

- Detailed Eligibility: You must insure more than one vehicle under the same GEICO policy.

- How to Apply: Simply link and add all household vehicles to a single policy.

🏠 Multi-Policy (Bundling) Discount

- Estimated Savings: 5% to 15%

- Detailed Eligibility: You bundle your auto insurance with another GEICO product, such as Homeowners, Renters, Condo, or Life insurance.

- How to Apply: Purchase policies through GEICO’s partner network and link your accounts.

🪖 Military Discount

- Estimated Savings: Up to 15%

- Detailed Eligibility: Available to active duty military, retired military, and National Guard or Reserve members.

- How to Apply: Submit your military ID or relevant service documentation.

🦅 Federal Employee (Eagle) Discount

- Estimated Savings: 8% to 12%

- Detailed Eligibility: Available to active or retired government employees (GS grades) and members of certain federal organizations.

- How to Apply: Provide proof of employment or federal ID.

🤝 Membership & Alumni Discount (Additional Discount)

- Estimated Savings: Up to 8%

- Detailed Eligibility: GEICO partners with over 500 professional groups, fraternities, sororities, and university alumni associations. If you belong to one, you get a break on your rate.

- How to Apply: Select your organization from their drop-down menu when quoting or call customer service.

🎓 4. Education & Demographics

📝 Good Student Discount

- Estimated Savings: Up to 15%

- Detailed Eligibility: Full-time students (typically ages 16-24) who maintain a ‘B’ average (3.0 GPA) or higher, or are in the top 20% of their class.

- How to Apply: Submit a copy of the most recent report card or transcript.

👴 Senior Driver / Defensive Driving Course Discount

- Estimated Savings: 5% to 15%

- Detailed Eligibility: Drivers (often 50 and older) with a safe driving record who voluntarily complete an approved defensive driving or accident prevention course.

- How to Apply: Submit the course completion certificate to GEICO.

🎗️ Seat Belt Use Discount

- Estimated Savings: Up to 15% (applies to Medical Payments/PIP coverage)

- Detailed Eligibility: You and your passengers sign a pledge to constantly wear seat belts.

- How to Apply: Opt-in during the policy setup.

📋 Important Rules for Maximizing Your Discounts

- Discount Stacking: The true power of GEICO’s pricing is that most of these discounts can be combined. For example, an active military member who is a safe driver, has a new car with airbags, and bundles their renters insurance will see all of those individual discounts stacked together for a massive reduction in their premium.

- State-by-State Variations: Insurance is highly regulated at the state level. Because of this, certain discounts (like the ‘DriveEasy’ telematics program or specific Good Student percentages) are only available in select U.S. states or may have different saving caps.

- Policy Renewals and Updates: Your discounts are not locked in forever. They are recalculated at every 6-month policy renewal. If you get a speeding ticket, your Safe Driver discount may drop off. Conversely, if your student brings their grades up to a ‘B’ average mid-year, you can submit the transcript to lower your premium on the next cycle.

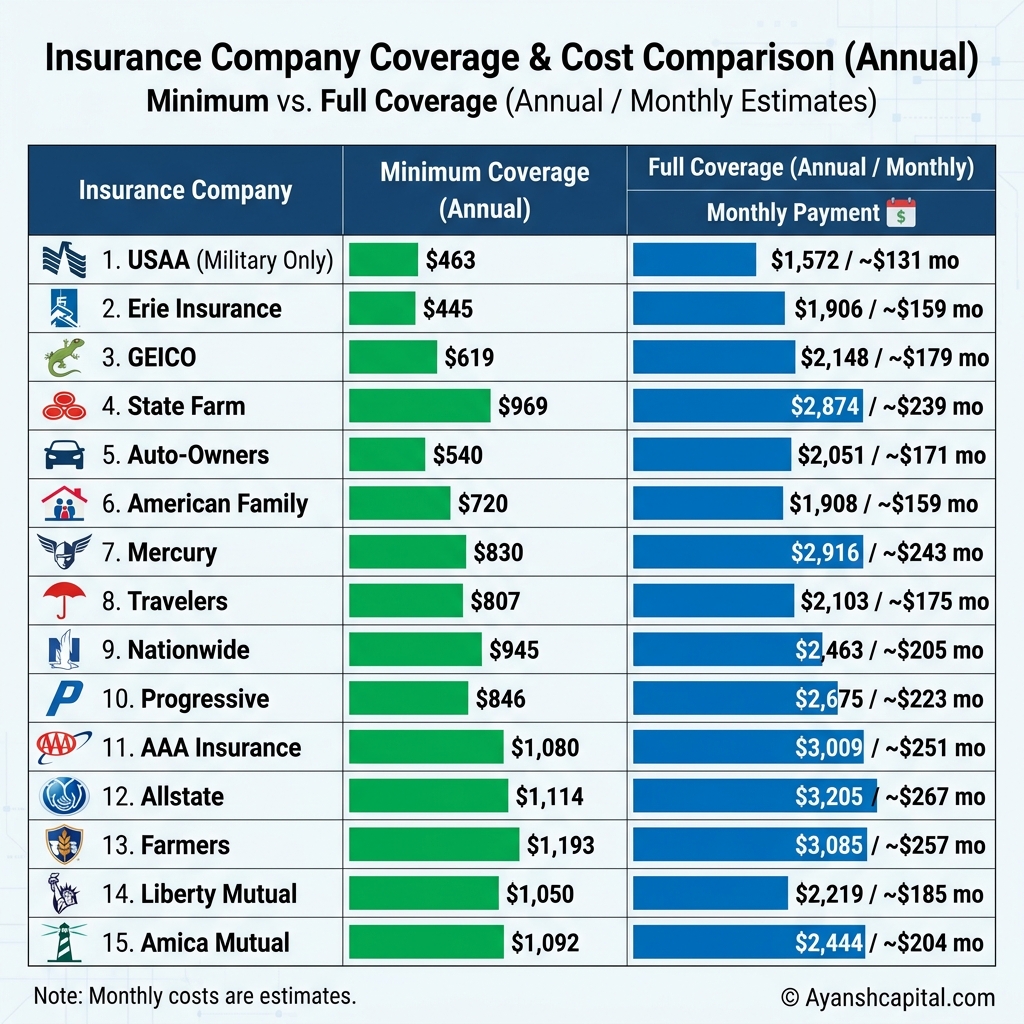

Full Coverage Top 15 Auto Insurance Rate Comparisons

Below is a detailed breakdown of Top 15 Car Insurance average annual rates for full coverage auto insurance across various driver profiles, compared directly against the national average.

GEICO Car Insurance Mobile App: A Complete Digital Vehicle Management System

GEICO is widely recognized as one of the most technologically advanced insurance companies in the United States. Today, Gen Z and Millennials often choose their insurance provider based entirely on the quality of their mobile app.

Below is a comprehensive breakdown of the GEICO Mobile App’s cutting-edge features, focusing on user experience (UX), technology, and real-world benefits.

1. Digital ID Cards

- The Tech & Benefit: This feature allows you to seamlessly save your auto insurance card directly to your Apple Wallet or Google Wallet. It eliminates the stressful hassle of searching for physical paper cards in your glovebox during a police traffic stop or an accident. Digital IDs are 100% legally valid across most states.

2. ‘Kate’ AI Virtual Assistant

- The Tech & Benefit: ‘Kate’ is an AI and Natural Language Processing (NLP)-driven virtual assistant that understands both voice and text commands. You never have to wait on hold for a human agent; Kate provides 24/7, instant answers to questions regarding billing details, coverage limits, and policy documents.

3. AI-Powered Easy Photo Estimate

- The Tech & Benefit: Utilizing your smartphone’s camera and advanced machine learning, this feature guides you step-by-step to capture the correct angles of your car’s damage after an accident. The AI immediately analyzes the photos to generate a repair estimate within hours, saving you a time-consuming trip to the auto body shop.

4. GEICO DriveEasy® (Telematics)

- The Tech & Benefit: This telematics program leverages your smartphone’s built-in sensors (GPS, accelerometer, and gyroscope) to monitor your driving habits—such as hard braking, sharp cornering, and phone usage while driving. It rewards focused, safe drivers with massive premium discounts of up to 25%.

5. On-Demand Roadside Assistance

- The Tech & Benefit: Functioning very much like the Uber app, this feature uses your exact GPS location to dispatch the nearest tow truck operator. You can watch the tow truck’s progress on a live tracking map, providing ultimate peace of mind if you are stranded on a dark highway at night.

6. Vehicle Care & CARFAX® Integration

- The Tech & Benefit: The GEICO app syncs directly with the CARFAX database using your car’s VIN (Vehicle Identification Number). It proactively sends you push notifications for upcoming routine maintenance (like oil changes) and immediately alerts you if the manufacturer issues a safety recall for your specific vehicle.

7. Gas Station & Parking Locator

- The Tech & Benefit: Utilizing Location-Based Services (LBS), the app scans your immediate area to find the cheapest gas stations and available parking slots. This is a massive time and money saver when navigating unfamiliar cities or heavy downtown traffic.

8. Biometric Login Security

- The Tech & Benefit: The app integrates seamlessly with your phone’s native hardware security—such as Face ID, Touch ID, or fingerprint sensors. This grants you secure, one-second access to your policy without needing to remember long, complex passwords, while keeping your sensitive data safe from hackers.

9. One-Click Smart Bill Pay

- The Tech & Benefit: Built with heavy encryption, the app links directly to Apple Pay, Google Pay, or your saved credit/debit cards. You can pay your monthly premium with a single swipe or easily configure auto-pay to avoid annoying installment fees and late charges.

10. Dynamic Policy Management

- The Tech & Benefit: This self-service dashboard is connected straight to GEICO’s backend mainframe for real-time updates. Without ever needing to call an agent, you can instantly add a newly purchased car to your policy, remove a driver, or increase your coverage limits on the fly.

Why the GEICO App is a Game-Changer

Boasting a stellar 4.8/5 rating on the Apple App Store with millions of user reviews, the GEICO app is far more than just a basic insurance portal—it is a comprehensive “vehicle management system.”

For the modern American driver, the era of keeping a cluttered glovebox full of paper documents is officially over. Whether it is tracking a live tow truck at 2 AM or flashing an insurance card to a police officer via Face ID in a split second, the app makes everything possible with just a few taps. This ultimate technical edge is exactly why younger generations strongly prefer GEICO over traditional, legacy competitors like State Farm or Allstate.

🚫 Money-Wasting Car Insurance Add-Ons: Drop These Now to Maximize Your Savings!

1. 🛑 Roadside Assistance: Avoid Paying Twice

- Skip it if: You already have a AAA membership, your premium credit card offers this perk for free, or your car is new and comes with 3 to 5 years of complimentary manufacturer roadside assistance.

- The Big Reason: Calling your insurance company for a tow or a battery jump-start is often recorded on your profile as a “mini-claim.” This can actually trigger a rate increase when it is time to renew your policy.

2. 🚕 Rental Car Reimbursement: An Unnecessary Expense

- Skip it if: You work from home (WFH), your household has an extra vehicle, or you can easily rely on public transit or Uber for a week or two while your car is in the shop.

- The Savings Math: Dropping this add-on can easily save you $30 to $50 per 6-month policy cycle—money that is much better spent on beefing up your essential liability limits.

3. 📉 ‘Full Coverage’ (Collision/Comprehensive) on Older Cars: When Premiums Outweigh Value

- Skip it if: Your vehicle is 10 to 12 years old and its current actual cash value has dropped below $3,000 or $4,000.

- The 10% Golden Rule: If you are paying 10% or more of your car’s total market value just in annual Collision and Comprehensive premiums, it is time to drop them. Stick strictly to the legally mandated Liability coverage.

4. 🛡️ Extended Warranty or MBI (Mechanical Breakdown Insurance): Redundant Protection

- Skip it if: Your car is brand new and still fully protected by the manufacturer’s factory warranty.

- The Big Reason: Major engine, transmission, or electrical failures in new cars are typically fixed for free under the dealership’s warranty. Paying your insurance provider for this add-on while the original warranty is active is a complete waste of money.

5. 💳 Gap Insurance: Don’t Forget to Cancel It on Time

- Drop it immediately if: You have paid off 70% to 80% of your auto loan, or the current market value of your vehicle is now higher than your remaining loan balance.

- The Savings Math: Gap coverage is only useful when you owe more on your car loan than the car is actually worth (preventing you from being “underwater” if it is totaled). Once your loan drops below the car’s value, keeping this add-on is just throwing cash away.

6. 🏥 Medical Payments (Med Pay) Overlap: Stop Double-Insuring Yourself

- Skip it (or reduce it) if: You and your family already have an excellent, high-limit personal Health Insurance policy.

- The Big Reason: If you are injured in a crash, your primary health insurance will cover the bulk of your hospital bills anyway. Carrying massive MedPay limits on your auto policy means you are essentially paying twice for the exact same coverage. (Note: If you live in a ‘No-Fault’ state where PIP is mandatory, simply carry the legal minimum).

7. 💎 Custom Parts and Equipment Coverage (CPE): Strictly for Modded Cars

- Skip it if: Your car is exactly the same as when it rolled off the showroom floor, and you haven’t added expensive aftermarket modifications (like custom alloy wheels, premium stereo systems, or a high-end paint job).

- The Big Reason: Standard auto insurance policies fully cover all factory-installed parts. This specific add-on is designed exclusively for heavily modified vehicles; for the average daily commuter, it is completely useless.

Top 15 Car Insurance Rates by Age & Experience

In the auto insurance industry, age and driving experience heavily dictate your premium. As you gain experience and your statistical risk of accidents decreases, Top 15 Car Insurance Rates by Age & Experience. Here is a quick breakdown of how age impacts your premium:

GEICO Payment Plans, Hidden Fees, and How to Avoid Them

Standard Payment Methods & Billing Fees

- Pay in Full: $0 fee. Paying your entire 6-month premium upfront on day one is the smartest way to save. It is completely free because it eliminates GEICO’s ongoing administrative and banking costs.

- EFT / AutoPay: $0 to $1 per month (depending on state laws). By linking your checking account and turning on paperless billing, you avoid high fees because ACH bank transfers cost GEICO significantly less than credit card merchant fees.

- Credit/Debit Card Installments: $3 to $5 per month. Visa and Mastercard charge “swipe fees” for every transaction, which GEICO passes on to the customer. Avoid this by paying in full or switching to EFT.

- Paper Billing Fee: $3 to $5 per bill. Printing, paper, and postage costs are high. You can completely avoid this fee by enabling “Paperless Billing” in your account settings.

Penalties & Special Administrative Fees

- Late Payment Fee: $10 to $15. This penalty is designed to encourage on-time payments and prevent policy cancellation. Avoid it by setting up AutoPay or calling GEICO for an extension before your due date.

- Reinstatement Fee: $10 to $20. If your policy is canceled due to non-payment and you want to reactivate it, GEICO charges this to cover the administrative underwriting costs. Prevent this by never letting your policy lapse.

- SR-22 / FR-44 Filing Fee: $15 to $25 (one-time). This covers the human and technical resources required to file mandatory high-risk driver forms with the state DMV. Avoid this entirely by driving safely and staying clear of DUIs or major tickets.

- Cancellation Fee: $0 fee. GEICO is one of the few major insurers that does not charge a “short-rate” penalty if you cancel your policy before the 6-month term ends. This is a major marketing advantage that allows customers to leave at any time without fear of hidden charges.

The Impact of Driving Violations on Premiums: A Comprehensive Breakdown

Step-by-Step Guide: Navigating the GEICO Claims Process

A car accident is incredibly stressful, and panic can easily lead to costly mistakes that delay or void your insurance claim. To keep your claim on track, follow this streamlined, step-by-step breakdown of GEICO’s digital-first claims process.

1. Immediate Response: Reporting & Digital Photo Estimation

- Step 1: Secure the Scene & File an Incident Report

- Prioritize safety first. Call the police to the scene to secure an official Police Report, which is vital for establishing fault.

- Exchange names, phone numbers, and insurance info with the other driver at the scene.

- File your claim within the first 24 hours. The fastest method is via the GEICO Mobile App (under ‘File a Claim’), or by calling 1-800-841-3000.

- Step 2: Submit a Digital Photo Estimate

- Skip waiting for an adjuster to visit in person. Use the app’s Easy Photo Estimate tool.

- The app will guide you to take clear photos of your vehicle’s damage from multiple angles in good lighting. This step takes only 15 to 30 minutes.

2. Resolution Phase: Damage Assessment, Repairs & Settlement

- Step 3: Damage Assessment by the Adjuster

- A professional GEICO Auto Damage Adjuster reviews your submitted photos and the police report to estimate repair costs. This evaluation typically takes 24 to 48 hours.

- If the car is severely damaged, they may declare it a Total Loss. If there is suspected hidden, internal damage, they will direct you to a certified garage for a teardown inspection.

- Step 4: Booking Repairs & Arranging a Rental

- By law, you can choose any mechanic. However, using GEICO’s certified Auto Repair Xpress® (ARX) network speeds up the process significantly and includes a lifetime guarantee on all repairs.

- If your policy includes Rental Reimbursement, GEICO will coordinate a rental car (via partners like Enterprise) directly at the repair facility. Repairs generally take 3 to 7 days depending on parts availability.

- Step 5: Final Payment & Claim Settlement

- Direct Pay (ARX Network): GEICO pays the shop directly. You only pay your chosen deductible (e.g., $500) straight to the garage when you pick up your vehicle.

- Check / Direct Deposit: If you use an independent mechanic or choose to keep the cash instead of repairing the vehicle, GEICO will mail a check or issue a direct deposit into your bank account immediately after the estimate is finalized.

Preparation & The Cancellation Call

- Secure a New Policy First (Step 1): Always purchase an active policy from a new provider before contacting GEICO. Even a one-day coverage gap can increase your future premiums.

- Create a Safe Overlap (Step 2): Set your new policy to start at least one day before your GEICO cancellation. Keep this overlap brief to avoid paying two companies simultaneously.

- Make the Required Phone Call (Step 3): GEICO does not offer an online cancellation button. You must call 1-800-841-1587, say “Cancel Policy” to the automated system, and have your policy number ready.

- Navigate the Retention Agent (Step 4): Agents will try to keep your business by offering lower rates or new discounts. Firmly state that you have already purchased a new policy to speed up the process.

Finalizing the Process & Post-Cancellation

- Set the Exact Cancellation Date (Step 5): You can cancel effective today or on a future date, but you cannot backdate. Ensure the cancellation is set to take effect at 12:01 AM.

- Halt Automatic Payments (Step 6): Explicitly ask the agent to stop your Auto-Pay or Electronic Funds Transfer (EFT) immediately to prevent accidental charges and delayed refunds.

- Avoid DMV Registration Issues (Step 7): Insurance companies automatically notify your state’s DMV when a policy is canceled. Ensure your new insurance data is active so your vehicle registration isn’t suspended.

- Collect Your Prorated Refund (Step 8): GEICO charges zero cancellation fees. You will receive a fully prorated refund for any unused premium, typically processed within 3 to 5 business days via direct deposit or check.

Property & Liability Bundles

- Auto + Renters (Assurant, Liberty Mutual): Saves you 3%–5%. This is the most popular bundle in the US because the auto discount essentially pays for the renters policy, making it feel almost “free.”

- Auto + Homeowners (Travelers, Homesite, Liberty): Saves you 10%–15%. With climate change driving up home insurance costs, this massive discount acts as a financial lifesaver for homeowners.

- Auto + Condo (Homesite, Assurant): Saves you 5%–10%. A highly affordable way for condo owners to secure necessary interior coverage while lowering their auto rate.

- Auto + Mobile Home (Assurant, Foremost): Saves you 5%–8%. This combination is extremely popular in rural America for mobile and manufactured homes.

- Auto + Umbrella Liability (RLI, GEICO Partners): Saves you 5%–8%. The top choice for high-net-worth individuals needing umbrella coverage to protect their assets from expensive lawsuits.

Vehicle, Lifestyle & Specialty Bundles

- Auto + Motorcycle (Directly Underwritten): Saves you 5%–10%. Because GEICO underwrites this policy directly rather than using a third party, the claims process is incredibly smooth.

- Auto + RV / Motorhome (Directly Underwritten): Saves you 5%–10%. Perfect for retirees and frequent road-trippers, offering seamless bundling directly through GEICO.

- Auto + Boat / PWC (GEICO Marine, BoatU.S.): Saves you 5%–8%. An excellent option for coastal residents in states like Florida and California, strengthened by GEICO’s robust partnership with BoatU.S.

- Auto + Life Insurance (Life Quotes Network): Saves you 3%–5%. While GEICO doesn’t sell life insurance directly, buying a term life policy through their partner network still earns you a modest auto discount.

- Auto + Pet Insurance (Embrace Pet Insurance): Saves you 0%–2%. While the auto discount is minimal, partnering with Embrace provides fantastic standalone coverage to combat skyrocketing veterinary costs.

GEICO Car Insurance: The Ultimate Verdict

GEICO is a stellar, value-for-money, and digital-first insurance option for the vast majority of drivers. Here is the final takeaway of what the company brings to the table:

The Core Strengths (Pros)

- Budget-Friendly Rates: GEICO delivers base premiums well below the industry average, complemented by heavy stackable discounts for safe drivers (Drive Easy app), military personnel, and good students.

- Cutting-Edge Technology: The highly-rated mobile app allows you to file claims, upload photo estimates, and manage your policy seamlessly with zero paperwork or phone calls.

- Unmatched Financial Stability: Backed by Warren Buffett’s Berkshire Hathaway and holding an A++ rating from A.M. Best, GEICO guarantees immense cash reserves to pay out claims safely.

The Limitations (Cons)

- No Local Agent Network: Operating on a direct-to-consumer digital model means you won’t have access to a local brick-and-mortar office for face-to-face assistance.

- Third-Party Home Bundling: GEICO does not underwrite homeowners insurance directly; instead, it coordinates these policies through a network of partner companies.

The Bottom Line: If you are completely comfortable managing your vehicle needs through your smartphone and want to secure some of the lowest premiums on the market, GEICO is an absolute winner. However, if you prefer traditional, personalized service with a dedicated neighborhood agent, legacy carriers like State Farm or Allstate may be a better fit.

Everything You Need to Know About GEICO Car Insurance

Q1: Who is GEICO auto insurance best suited for?

Answer: It is perfect for budget-conscious, tech-savvy drivers, and military personnel who prefer managing their policy entirely via a smartphone and do not need a dedicated local insurance agent.

Q2: Does GEICO underwrite its own homeowners insurance?

Answer: No, GEICO acts as an agency for home and renters insurance. They bundle these policies by selling them through a network of trusted partner companies (such as Travelers, Assurant, or Liberty Mutual).

Q3: What is GEICO ‘Drive Easy’ and what is the benefit?

Answer: DriveEasy is a telematics feature built into the GEICO mobile app that monitors your driving habits (such as speeding and hard braking). Consistently safe drivers can earn a premium discount of up to 25%.

Q4: How easy is the claims process after an accident?

Answer: It is incredibly fast and user-friendly. You can use the app’s ‘Easy Photo Estimate’ feature to upload pictures of your car’s damage. The AI and digital adjusters typically provide a repair estimate within just a few hours.

Q5: Which coverages should I drop to save money?

Answer: If your car is more than 10 years old and its actual cash value has dropped below $4,000, you should strongly consider dropping the expensive ‘Full Coverage’ (Collision and Comprehensive) and sticking to liability.

Q6: Does GEICO charge a penalty if I cancel my policy mid-term?

Answer: No, GEICO does not charge any cancellation fees or “short-rate” penalties. If you paid your premium in advance, you will receive a fully prorated refund for any unused days.

Q7: How can I avoid GEICO’s “hidden” installment and paper billing fees?

Answer: The easiest way is to pay your 6-month premium in full upfront. If that isn’t possible, you can avoid these fees by setting up AutoPay (EFT) directly from your checking account and turning on “Paperless Billing” in the app.

Q8: What exactly is GEICO’s MBI (Mechanical Breakdown Insurance)?

Answer: MBI acts as a highly affordable extended warranty for new cars. It covers the repair costs if your vehicle experiences a sudden, major mechanical failure (like engine or transmission issues) that is not related to a car accident.

Q9: How secure is GEICO’s financial strength for paying claims? Answer: It is completely secure. GEICO is backed by Warren Buffett’s Berkshire Hathaway and holds the highest possible ‘A++’ rating from A.M. Best, meaning they have massive cash reserves to comfortably pay out all claims.

Q10: When should I choose State Farm or Progressive instead of GEICO?

Answer: You should choose State Farm if you prefer personalized, face-to-face service with a local neighborhood agent. You should look into Progressive if you have a spotty driving record (like a DUI or multiple accidents), as they tend to offer better rates for high-risk drivers.