USA Auto Loan Guide: Avoid Costly Mistakes & Get Approved

Buying a car in the US is a major decision, and an even bigger one is choosing the right auto loan. If you walk into an American dealership unprepared, you could end up losing thousands of dollars purely in interest and hidden fees.

Economics of US Auto Loans

In the US, a car loan is a ‘secured loan’, which means your car itself serves as the collateral for the loan. If you default on your payments, the bank has the legal right to repossess your car without needing a court order.

Amortization and the Math of Loans

Car loan payments operate based on an amortization schedule. During the initial months, a large portion of your EMI goes purely toward paying the interest, and the principal amount decreases very slowly.

How Does an Auto Loan Work?

Before signing any loan contract, you must understand exactly how the different components of an auto loan function together. A detailed, point-wise breakdown of its main components is provided below:

1. Principal (The Amount You Borrow) The principal of an auto loan is not just the sticker price (MSRP) of the car. It is the total amount for which you request a check from the bank.

- What is added to it? Dealer fees (Doc fees), state sales tax, and any extra accessories you have purchased.

- How is it reduced? If you are buying a $35,000 car and you make a $5,000 down payment or exchange your old car as a trade-in for $3,000, your principal will decrease to $27,000. For this auto loan, the bank will only charge interest on this remaining $27,000.

2. Interest Rate vs. APR People often consider the interest rate and the APR of an auto loan to be the exact same thing, but there is a subtle difference between them:

- Interest Rate: This is the percentage the lender charges you in exchange for lending the money.

- APR (Annual Percentage Rate): This is the total sum of the interest rate plus the bank’s hidden fees, such as an origination fee.

- How does it work? A standard auto loan generally works on simple interest. This means that interest is calculated every day on your remaining principal balance. The faster you pay off the principal, the less interest you will be charged.

3. Loan Term This is the timeframe in which you have to repay your auto loan (typically 36, 48, 60, 72, or 84 months).

- Short Term (36 or 48 months): Your monthly installment (EMI) will be much higher, but you will pay very little interest to the bank.

- Long Term (72 or 84 months): The installments become smaller, making the budget feel easier to manage, but you end up paying thousands of dollars just in interest over the long run.

- Current Trend: According to an Experian report, due to the rising prices of cars in Current , approximately 36% of new auto loan contracts are exceeding 72 months.

4. The Negative Equity Trap (Upside Down) This is considered the most dangerous part of an auto loan. Cars are a depreciating asset. A new car loses 10% to 20% of its value the moment it is driven off the dealership lot.

If you have taken a long 84-month term or did not make a down payment, it is possible that after two years, your car’s market value might drop to $20,000, while your bank balance still stands at $24,000.

This situation is called being “underwater” or having negative equity. In such a scenario, if the car crashes or you want to sell it, you will have to pay $4,000 out of your own pocket to the bank to clear the auto loan.

5. Amortization When you pay your monthly installment (EMI), a very large portion of your money initially goes solely toward paying the interest, while a very small portion reduces the principal. As your auto loan gets older, this ratio flips, and your money starts reducing the principal amount.

Understanding the Auto Loan Financing Process

Understanding the auto loan financing process in depth is the most crucial step for any car buyer. In today’s digital age, securing an auto loan has become much more transparent and faster than before. Setting up your financing from the comfort of your home before visiting the dealership gives you the power of a “cash buyer.”

Below is a detailed, accurate, and point-wise analysis of the entire auto loan financing process in the US:

1. Preparation & Documentation

Before applying for an auto loan online, you must have the correct information and documents ready so the process runs smoothly without any interruptions.

- Proof of Income: The lender wants to see if you are capable of repaying the auto loan. This requires your recent 2-3 pay stubs, W-2 forms, or tax returns from the past two years.

- Proof of Identity and Residence: You will need a valid driver’s license, your Social Security Number (SSN), and a utility bill (like an electricity or water bill) confirming your current address.

- Credit Report Check: At least one month before applying for an auto loan, be sure to check your credit reports (Experian, Equifax, TransUnion) to correct any errors.

2. Online Pre-qualification (Soft Credit Check)

This is the first digital step where you estimate your potential interest rate without damaging your credit score.

- Soft Credit Pull: Companies like Capital One or MyAutoloan initially perform only a “soft inquiry.” This lets you know how much money and at what APR you could get for your auto loan, and it has no impact on your credit score.

- Comparison: During this stage, you should compare the rates of at least 3 to 4 different lenders (such as a bank, a credit union, and an online lender).

3. Getting Pre-Approved (Hard Credit Check)

After pre-qualification, once you select a lender, you officially apply for a pre-approval.

- Hard Inquiry: In this stage, the lender pulls your complete credit report. This can cause a minor drop of 2 to 5 points in your score.

- Rate Shopping Window: According to FICO (Fair Isaac Corporation) rules, if you trigger multiple hard inquiries for an auto loan within a window of 14 to 45 days, it is only counted as a single inquiry. Therefore, do not panic and actively search for the best rate.

- Pre-Approval Letter (Blank Check): After approval, the bank gives you a letter or digital certificate. It clearly states the maximum amount the bank is willing to lend you (e.g., $35,000) and the interest rate (e.g., 5.5% APR) for your auto loan. This letter remains valid for 30 to 60 days.

4. Using Pre-approval as Leverage at the Dealership

This is the most important stage where your pre-approval acts as a powerful weapon in negotiations.

- Separate Car Price and Loan: When speaking with the dealer, never initially reveal that you have a pre-approval or that you are trading in your old car. First, strictly negotiate and finalize the final “Out-the-Door” price of the car.

- Avoid Dealer Markup: If you go without a pre-approval, the dealer gets a base rate (Buy Rate) from the bank based on your credit (say, 5%), adds their commission (Dealer Reserve), and offers you 7%. Having a pre-approved auto loan completely prevents the dealer from playing this trick.

- The “Beat My Rate” Challenge: Once the final price is settled, show your pre-approval letter and say: “My bank gave me a rate of 5.5%; if your financing department can give me 5%, I will take the auto loan from you.” Often, to successfully sell the car, dealers will offer a better rate. If not, you simply use your bank’s money.

5. Final Paperwork & Closing

Once the financing is finalized, you must sign the contract (Truth in Lending Act Disclosure).

- Avoid Add-ons: At this time, the Finance Manager (F&I Manager) will try to sell you extended warranties, tire protection, and GAP insurance. Keep in mind that all these extra costs get added to the principal of your loan, meaning you will end up paying interest on them for years.

- Payment to the Bank: If you opted for your pre-approved bank, the dealership contacts that bank directly, the bank sends the funds to the dealer, and your loan officially begins with your bank.

By following this exact point-wise process, you can completely avoid the mental stress at the dealership and protect yourself from hidden fees and inflated interest rates.

Banks vs. Credit Unions: What’s Right for Your Auto Loan?

As soon as you enter the auto loan market, you will immediately encounter two main types of financial institutions: Traditional Banks and Credit Unions. Dealerships do not use their own money to fund your vehicle; they simply act as middlemen for these institutions. Choosing the right lender for your auto loan depends heavily on whether you prioritize maximum convenience or maximum financial savings. Let us deeply analyze how these institutions operate and differ.

1. Traditional Banks (The For-Profit Giants)

Institutions like Bank of America, Chase, and Wells Fargo operate strictly on Wall Street rules and prioritize shareholder profits.

- Business Model: Their primary goal is to generate profit. Because of this, the interest rates (APR) they charge on a standard auto loan are generally higher compared to credit unions.

- Technology and Ecosystem: This is their biggest advantage. Their mobile banking, auto-pay systems, and customer service are highly advanced. If you already have a checking account or an existing auto loan with them, you can conveniently manage everything from a single digital dashboard.

- Relationship Discounts: If you are a loyal customer with a healthy account balance, many banks offer a rate discount ranging from 0.25% to 0.50% on your auto loan when you set up an auto-pay system.

- The Disadvantages (Strict Rules): Traditional banks have extremely strict underwriting guidelines. If there is any flaw in your credit history or your score is below 660, they might instantly reject your auto loan application or charge heavily inflated interest rates.

2. Credit Unions (The Non-Profit Community)

Institutions like PenFed, Navy Federal, and Alliant are non-profit organizations. They are not owned by outside investors, but rather by their own account holders, who are referred to as “members.”

- Business Model: Because they do not have to pay dividends to shareholders, they return their profits to their customers in the form of lower fees and a lower APR on an auto loan. This is exactly why their rates are typically 1% to 2% lower than those of traditional banks.

- Empathetic Underwriting: Credit unions do not just look at your credit score when reviewing an auto loan application; they look at your entire story. If your credit score is only average but you have a stable and secure job, a traditional bank might reject you, but a credit union is much more likely to approve your auto loan.

- The Membership Myth: Many people mistakenly believe that opening an account at a credit union is very difficult. The truth is that in today’s digital age, you can instantly become a member of large institutions like PenFed or Consumers Credit Union by simply making a small, specific donation (such as $5) before applying for your auto loan.

- The Disadvantages: Their digital technology is often not as modern as the giant banking corporations, and they usually have far fewer physical branch locations available for in-person auto loan support.

The Foolproof Auto Loan Strategy

Buying a car is a financial game, and the dealership’s Finance and Insurance (F&I) Managers are the absolute masters of this game. Their primary job is not just to sell you a car, but to sell you an auto loan. To save yourself thousands of dollars, you must follow these four specific strategies in a strict order:

1. One to Three Months Before Applying: Check Your Credit Report

Dealerships never want you to know your exact credit score before you apply for an auto loan.

- What to do: Visit AnnualCreditReport.com and pull your free reports from all three major credit bureaus (Experian, Equifax, and TransUnion).

- Why do it: Check the reports for any errors and dispute them immediately. Furthermore, bring your credit card utilization ratio below 30%. If your current score is 680 and you improve it to 720 (Prime Tier) before applying for an auto loan, you can save anywhere from $1,500 to $2,500 in interest over a 60-month term.

2. Before Visiting the Dealership: Get a Pre-Approval

This is the single most important rule of car buying: never go to a dealership empty-handed, relying solely on them to find you an auto loan.

- The Strategy: One week before visiting the dealership, apply for an auto loan at a minimum of one major bank (like Capital One) and one credit union (like PenFed).

- FICO’s Rate-Shopping Rule: Many buyers fear that applying at multiple places will drop their credit score. However, under the FICO model, all auto loan applications submitted within a 14 to 45-day window are treated as just a “Single Hard Inquiry.” Therefore, feel free to shop around at 3 to 4 different lenders.

- The Pre-Approval Letter: Print the pre-approval letter (which acts like a blank check) from the institution offering the lowest rate and keep it in your pocket. This gives you the ultimate negotiating power of a cash buyer.

3. At the Dealership: Negotiate the Out-the-Door Price, Not the EMI

This is where dealerships trap the most customers using the infamous “Four-Square Method” to manipulate your auto loan.

- The Trap: The salesman will ask, “How much of a monthly installment (EMI) do you want to pay?” If you answer, “I want a $400 EMI,” they will readily agree. What do they actually do? They simply extend your auto loan term from 60 months to 72 or 84 months. Your EMI hits $400, but you end up paying thousands of dollars more than the car’s actual worth in interest.

- The Solution: Dodge the EMI question completely. Clearly state: “I will discuss the auto loan financing later; first, tell me the exact Out-the-Door (OTD) price of this vehicle.” The OTD price means the base price of the car (MSRP) + Dealer Fees (Doc Fees) + Taxes + Registration. Do not mention your pre-approval letter until the OTD price is definitively locked in.

4. The Final Strike: Challenge the Dealer to Beat Your Rate

Once the car’s OTD price is locked on paper, head into the Finance Manager’s office.

- Dealer Markup (Dealer Reserve): When the dealer secures an auto loan for you from a bank, the bank gives them a wholesale ‘Buy Rate’ (let’s assume 5%). The dealer adds their own commission to it and offers you 7%. That 2% middleman profit goes directly into the dealership’s pocket.

- Your Move: Place your pre-approval letter on the table and explicitly say: “I already have a 5.5% APR offer from my credit union for this auto loan. If you can give me a rate of 5.2% or lower, I will take the financing from you. Otherwise, I will use my bank’s check.”

- The Result: Dealers have strong wholesale relationships with banks. To save the sale and make at least some profit on the auto loan, they will often “beat” your bank’s rate. If they do, you win. If they cannot, you already have your pre-approved financing safely secured.

Secret Tips to Save Thousands in Interest on Your Auto Loan

If for some reason (such as having a high Loan-to-Value ratio) you are unable to refinance, do not panic. By simply hacking the math behind amortization, you can easily secure massive savings on your current auto loan. Here is a detailed guide on how to do it:

1. The Math Behind the Bi-Weekly Payment Strategy Most people make their monthly installment (EMI) once a month. Instead of doing this, cut your EMI in half and make a payment to the bank every two weeks (14 days).

- How the magic works: There are 12 months in a year, but there are exactly 52 weeks.

- For example: If your auto loan EMI is $500, you pay $6,000 over the course of the year (12 x $500). But if you pay $250 every 14 days, you will make 26 payments in a year (26 x $250 = $6,500).

- The Result: By the end of the year, you have unknowingly made an entire extra payment (a 13th month) to the bank. This extra money goes 100% toward reducing your principal balance, meaning a 60-month auto loan can be paid off in approximately 54 months.

2. Round Up Your Payments This is both a psychological and mathematical strategy that can significantly impact your auto loan.

If your monthly installment is $362, go into your auto-pay system and round it up to $400. The additional $38 you pay every month will be deducted directly from your principal balance. In a standard auto loan, daily interest is calculated strictly on the remaining principal. The faster the principal drops, the faster the interest charged on it disappears.

- Warning: When setting up your auto-pay, you must give written instructions to the bank stating that “any extra amount must strictly be used for principal reduction, and not applied as an advance payment for the next month’s auto loan installment.”

3. The Power of Bundling with Your Auto Insurance Provider The cost of a car is not just the vehicle itself; it is the combined expense of the debt plus the insurance. Many people do not realize that top insurance companies in the US are also heavily active in the financing market.

- USAA: If you come from a military background, USAA not only provides some of the lowest insurance premiums in the market, but their auto loan rates are also exceptionally low. When you bundle both your insurance and your vehicle financing with USAA, your total monthly cost drops significantly.

- State Farm and Progressive: These companies offer excellent financing options to their policyholders through specific bank partner programs. Furthermore, if you are a safe driver and utilize their telematics programs (like Progressive Snapshot or State Farm Drive Safe & Save), state-specific regulations might allow you to get up to a 30% discount on insurance. This massively reduces the overall cost of maintaining your auto loan and vehicle.

- GEICO: GEICO has its own dedicated partner network that provides instant financing or refinancing facilities to existing policyholders. Keeping both your insurance and your auto loan within the same ecosystem makes the paperwork incredibly simple and fast.

4. Avoid Expensive Dealership Add-ons (Especially GAP Insurance) The biggest profit for a dealership’s Finance Manager is hidden in the extra add-ons they sell you at the closing desk. These include extended warranties, tire protection, and most prominently, GAP (Guaranteed Asset Protection) insurance.

- What is GAP? If your car is stolen or totaled in an accident, a standard insurance company will only pay the “Actual Cash Value” (the current market value) of the car. If that value is lower than your remaining balance, you must pay the difference (the gap) out of your own pocket. GAP insurance covers this exact difference.

- The Dealership Scam: The dealer will charge you anywhere from $800 to $1,200 for this exact GAP insurance and roll it directly into the principal of your auto loan. This means you will be paying interest on that massive markup for up to 5 years.

- The Smart Strategy: Never buy GAP from the dealership. Call your current insurance company, whether it is State Farm, Progressive, or GEICO. They will simply add this exact same GAP coverage to your existing insurance premium for merely $20 to $40 per year (about $2 to $3 per month). This one tiny adjustment will save you hundreds of dollars over the lifespan of your auto loan.

Biggest Auto Loan Mistakes to Avoid

Choosing the right lender is only half the battle; falling for common mistakes at the dealership can easily turn thousands of dollars in savings into massive financial losses. When purchasing a car , you must absolutely ensure that you avoid these critical financial traps related to your auto loan:

1. Focusing Only on the Monthly Installment (EMI) This is universally recognized as the biggest and most common mistake made by car buyers seeking an auto loan.

- The Dealer’s Trick: When you tell a dealer that your strict budget is $350 per month, they will simply stretch the auto loan term from a standard 60 months to a lengthy 84 months.

- The Damage: While your EMI drops to your desired $350, you end up paying an extra two years of interest to the bank. Because of this, a car originally priced at $25,000 will ultimately cost you $32,000.

- The Solution: Always negotiate strictly on the total “Out-the-Door” cost of the vehicle, never on the EMI.

2. Rolling Over Negative Equity into a New Auto Loan If you still owe $15,000 on your old auto loan, but the car’s current market value is only $10,000, you are sitting in $5,000 of “Negative Equity” (also known as being underwater).

- The Mistake: Many buyers choose to roll over this remaining $5,000 deficit directly into the principal of their new auto loan.

- The Consequence: You end up paying high interest on a vehicle you do not even own anymore. If possible, always pay off your negative equity in cash. Never roll it over into your new auto loan.

3. Skipping the Fine Print on the Auto Loan Contract There is immense psychological pressure inside the dealership’s Finance and Insurance (F&I) office, causing buyers to hastily sign dozens of complex pages without reading them.

- What to do: Always carefully read the “Truth in Lending” box, which is legally required to be on the very first page of your auto loan contract. It explicitly states your exact APR (interest rate), the total Finance Charge (total interest), and the sum of your Total Payments.

- Warning: Always verify that there is no “Pre-payment Penalty” secretly added to your auto loan, which would legally punish you financially for paying off your debt early.

Financing vs. Leasing a Car: What’s Right for You?

If you want to avoid the currently high interest rates associated with a standard auto loan, “leasing” a car is a very popular alternative. However, there is a fundamental difference between the two financial paths:

1. Car Financing (Taking an Auto Loan) When you take an auto loan, you are borrowing money from a bank with the ultimate goal of owning the car outright.

- The Advantages: Once the final payment on the auto loan is made, the car is 100% yours. You can drive it for unlimited miles without any penalties, and you can freely customize or modify the vehicle however you wish.

- The Disadvantages: Your monthly installments (EMI) will be noticeably higher compared to a lease. Furthermore, once the factory warranty expires, all maintenance and major repair costs come directly out of your own pocket.

2. Car Leasing Leasing a car means you are essentially renting the vehicle for a fixed period (typically 3 years). You are only paying for the depreciation that the car experiences during the exact time you are driving it, rather than paying off the full value via an auto loan.

- The Advantages: The monthly payments are significantly lower than a standard auto loan. You get to drive a brand-new car every three years, and the vehicle is always covered under the factory warranty, eliminating unexpected repair bills.

- The Disadvantages: You will never actually own the car. Leases come with extremely strict mileage limits (such as 10,000 miles per year). If you exceed this limit or return the car with excessive wear and tear, you will face massive financial penalties.

Rules for Used Car Loans and Bad Credit Financing

Financing a used car is slightly different compared to taking out an auto loan for a brand-new vehicle. Banks and financial lenders generally consider used cars to be “high risk” assets. The primary reason for this is vehicle depreciation. If you fail to repay your auto loan, the bank will repossess and sell the car, and it is notoriously difficult to accurately estimate the future resale value of an older, used car.

Because of this inherent risk, the interest rates (APR) on a used auto loan are almost always 2% to 4% higher than the rates offered for new cars. When you apply for a used auto loan, you will likely encounter these three major rules:

- Age Limit: Most mainstream lenders will simply refuse to provide an auto loan for a vehicle that is more than 10 years old. Some specific credit unions might extend this limit to 12 years, but the interest rates will be significantly higher.

- Mileage Limit: If a car has already been driven for more than 100,000 miles, many banks will deny financing. Some specialized online lenders may approve an auto loan for cars with 120,000 to 150,000 miles, but the lending conditions will be extremely strict.

- Clean Title Requirement: Lenders will never finance cars that carry a “Salvage” or “Rebuilt” title. These are vehicles that have been completely totaled in an accident and subsequently rebuilt. Banks require a clean title to approve any auto loan.

How to Get an Auto Loan with a Bad Credit Score

In the United States, your credit score is the absolute key to your financial life. If your credit score drops below 600, you are placed into the “Subprime” or “Deep Subprime” category by lenders. Having bad credit directly means that you will be forced to pay a massive interest rate on your auto loan.

While exact numbers fluctuate, data consistently shows how severely your credit score impacts the APR you are offered for both new and used vehicles.

- Crucial Note: If your credit score is below 500 (Deep Subprime), the interest rate for a used auto loan can easily skyrocket above 20%.

If your credit is poor, you must keep these vital strategies in mind when securing an auto loan:

- Make a Large Down Payment: Putting down at least 20% of the vehicle’s price significantly reduces the lender’s financial risk. This dramatically increases your chances of getting the auto loan approved and helps secure a much better interest rate.

- Bring a Co-signer: If someone in your family has an excellent credit score, adding them as a co-signer on your application can cause your auto loan interest rate to drop heavily. The bank will rely on their good credit history to approve the financing.

- Provide Solid Proof of Income: For borrowers with bad credit, banks urgently want to verify that your job is highly secure. Always have your most recent pay stubs and utility bills ready to prove your income stability when applying.

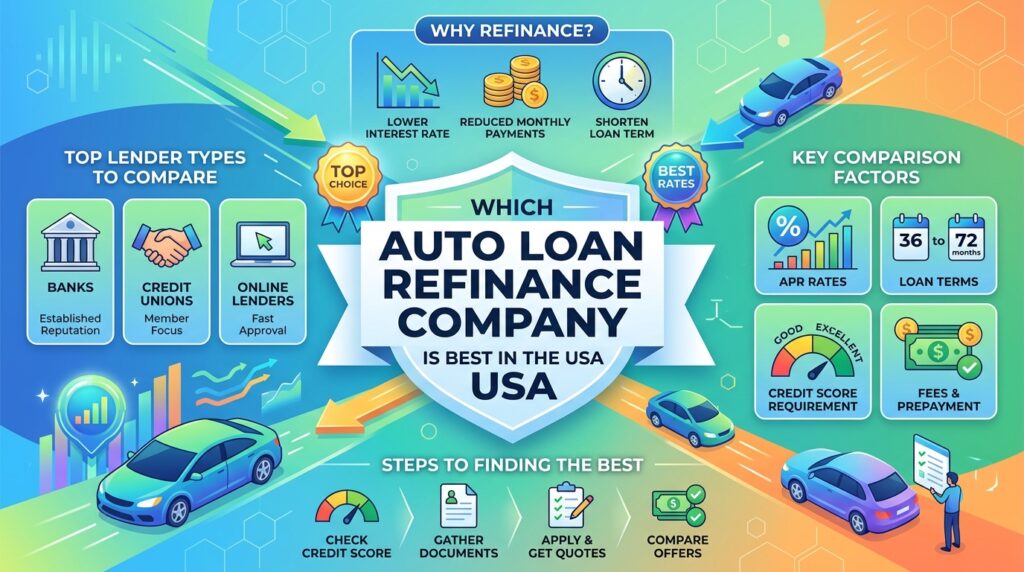

How to Refinance Your Auto Loan

Many people continue paying heavy interest throughout their entire loan term, thinking that once an auto loan is taken, it cannot be changed. But the truth is that you can refinance your auto loan at any time.

Refinancing simply means taking a new auto loan from a new lender (or the same lender) at a new and better interest rate to pay off your existing car loan.

When Should You Refinance Your Car?

- Your Credit Score Has Improved: If your credit score was 600 when buying the car, but now it has become 720+, you should refinance immediately. This can cut your interest rate in half.

- Market Rates Have Dropped: If the Federal Reserve has lowered interest rates in Current due to changes in the economy, take advantage of it.

- You Got a Bad Deal from the Dealership: If you hastily signed the dealership financing and now feel that you were ripped off, you can refinance it with a credit union after just a few months.

4 Easy Steps for Refinancing:

- Step 1: Know the Payoff Amount: Call your current lender and ask exactly how much money you need to pay off the auto loan completely as of today’s date.

- Step 2: Check Your Car’s Current Value: Check your car’s current resale value on Kelley Blue Book (KBB) or Edmunds. If your car’s price is less than your remaining balance (this is called being ‘underwater’ or having ‘negative equity’), refinancing will be difficult.

- Step 3: Apply for New Rates: Apply for refinancing your auto loan with at least three different lenders (especially credit unions).

- Step 4: Choose the New Loan and Close the Old One: The new lender will send a check directly to your old bank and close your old account. Now, you will start paying the new (and lower) installments to the new lender.

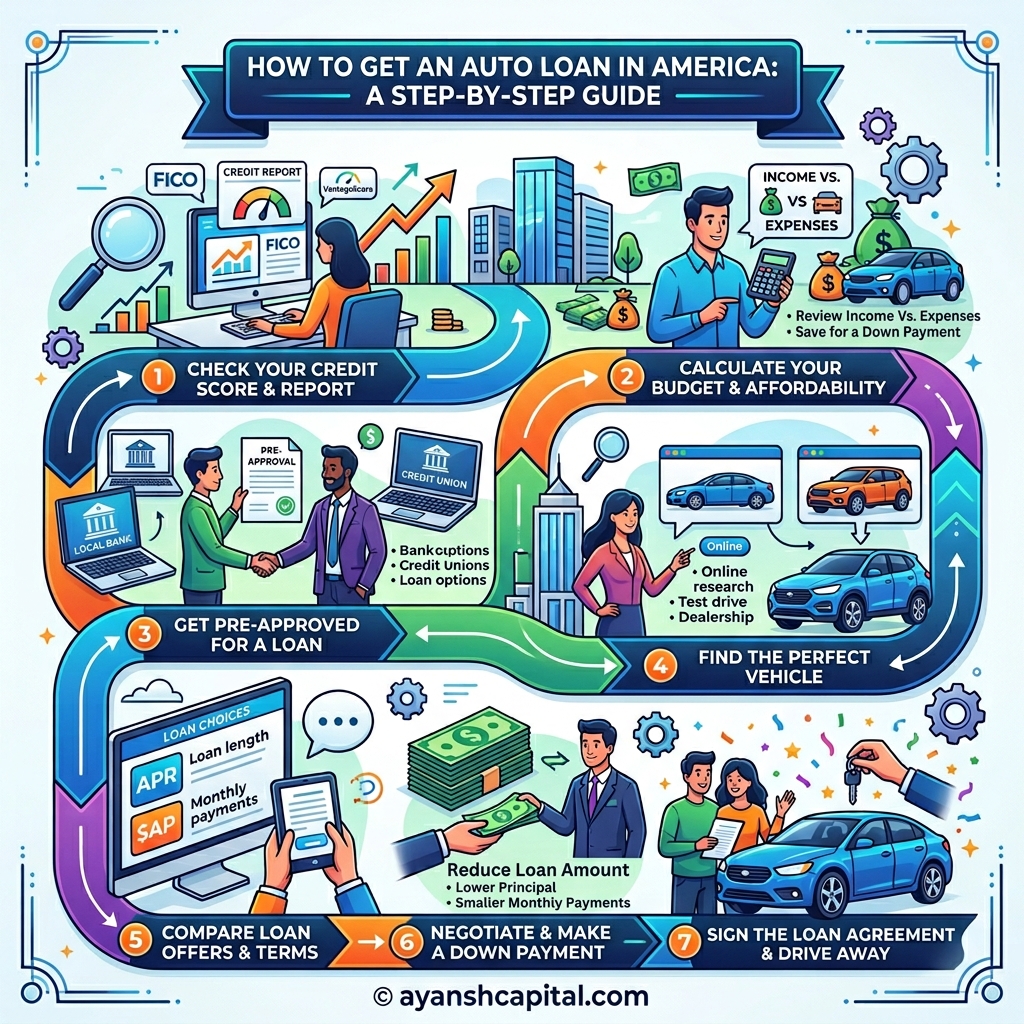

The Detailed 8-Step auto loan Process

Following this detailed process in the exact order is essential. Breaking this sequence means handing over your financial power to the dealership.

Step 1: Set a Realistic Budget (The 20/4/10 Rule) Strictly follow this rule to avoid market fluctuations and severe vehicle depreciation:

- 20% Down Payment: New cars lose 20% of their value in the first year alone. Paying 20% in cash ensures you never become ‘underwater’ on your auto loan.

- 4 Years (48 Months) Term: Aim to completely finish your auto loan in 48 months (maximum 60 months).

- 10% Income Limit: The total cost of the car’s EMI, fuel, and especially auto insurance should strictly remain between 10% and 15% of your take-home salary.

Step 2: Freeze and Audit Your Credit Report Visit www.annualcreditreport.com exactly 30 days before applying for an auto loan. Check your report for any errors. If there is an old, incorrect collection account, dispute it immediately.

Step 3: Get Pre-Approved (The Golden Key) The dealership’s Finance & Insurance (F&I) department works closely with lenders to place a markup on your APR. For example, if the bank officially approves you for 6%, the dealer will tell you it is 8% and pocket the 2% difference.

- Where to Go: Local credit unions typically offer the best rates. Institutions like PenFed or Navy Federal (if eligible) are excellent options for a cheap auto loan.

- Soft vs. Hard Pull: When checking rates, lenders perform a ‘soft pull’, which does not drop your credit score. When you officially apply, a ‘hard pull’ occurs. Note: FICO treats all auto loan hard pulls made within a 14 to 45-day window as a single inquiry, so shop for rates aggressively.

Step 4: Negotiate Only on the OTD (Out-the-Door) Price At the dealership, the salesman’s very first question will be: “How much do you want to pay per month?” This is a classic trap designed to manipulate your auto loan.

- Your Answer: “I will discuss the financing later; first, let’s finalize the Out-the-Door (OTD) price.”

- What OTD Includes: The vehicle price + Destination Fee + State Taxes + DMV Registration + Dealer Documentation Fees.

Step 5: Keep the Trade-In Separate If you are trading in your old car, never mix it with the new vehicle’s purchasing process. First, finalize the OTD price of the new car, then say: “Now let’s talk about what value I will get for my old car.” Get a written offer from CarMax or Carvana beforehand so the dealer cannot lowball you and unfairly inflate your new auto loan.

Step 6: Face the Finance and Insurance (F&I) Room This is the most profitable room in the dealership. Here, the finance manager will aggressively try to sell you add-ons to increase your auto loan principal:

- Extended Warranty: Usually extremely expensive. (Decline)

- Tire/Wheel Protection: (Decline)

- VIN Etching: (Decline, this is a known scam) Here, you will present your bank pre-approval. Only accept the dealer’s lender (like Toyota Financial) if they can offer you a legitimately lower APR for your auto loan.

Step 7: The Crucial Connection Between Car Insurance and Your Loan When you finance a vehicle, in addition to state insurance laws, the lienholder (lender) has their own strict requirements. You cannot get away with just holding basic liability insurance.

- Full Coverage is Mandatory: The bank will demand that you securely maintain Comprehensive (theft, weather damage) and Collision (accidents) coverage throughout the entire life of the auto loan.

- This requirement can dramatically increase your monthly expenses. Therefore, before finalizing the car, take the specific VIN and conduct a deep comparative analysis. Evaluating policies across major providers like USAA (for military families), State Farm, GEICO, and Progressive will reveal significant differences in premiums.

- Set coverage limits according to various state regulations and adopt the strategy of bundling your auto policy with renters or home insurance to actively lower the premium.

Step 8: Read and Sign the Contract Before signing, carefully examine the “Truth in Lending Act (TILA)” box. It must clearly state four specific things regarding your auto loan:

- APR (Annual Percentage Rate)

- Finance Charge (The total interest you will pay)

- Amount Financed (The exact loan amount)

- Total of Payments (What the car will ultimately cost at the end)

How GAP Insurance Works

When you make a down payment of less than 20%, ‘GAP Insurance’ becomes absolutely crucial for your auto loan.

- What is it: Suppose you take out an auto loan for $30,000. A month later, the car is ‘totaled’ (destroyed). The insurance company will only write a check for the current market value (let’s say $24,000). You will now have to pay the remaining $6,000 to the bank out of your own pocket. GAP insurance strictly covers this $6,000 ‘gap’ or difference.

- Where to get it: The dealership will aggressively try to sell this to you for $800 to $1,000. Instead, add it to your monthly policy through your auto insurance provider (this usually costs only $4 to $5 per month) rather than permanently adding it to your auto loan.

Options for New Immigrants, F1/H1B Visa Holders, and Those Without an SSN

Entering the American financial market without a US credit history is a challenge, but clear solutions exist to successfully secure an auto loan:

- Credit Building Programs: Major manufacturers like Ford, Toyota, and Honda have ‘Foreign Professional’ and ‘College Graduate’ programs. They offer excellent Tier-1 or Tier-2 rates based strictly on your employment Offer Letter and Visa status, completely bypassing the need for prior credit history.

- Using an ITIN: If you do not have an SSN, several credit unions and banks (such as Bank of America) will actively process your auto loan using an Individual Taxpayer Identification Number (ITIN).

- Alternative Data Lenders: Fintech companies like Lendbuzz and Nova Credit evaluate your default risk based on your home country’s credit data (like India or the UK), cash flow in your bank statements, and regular utility bill payments.

- Co-Signer: If someone with a 750+ FICO score (a relative or friend) safely guarantees your application, you will instantly get a fantastic APR on your auto loan. (Keep in mind, if you default, their credit will be completely ruined).

Common Dealership Financial Traps to Avoid

- Yo-Yo Financing (Spot Delivery Scam): The dealer lets you enthusiastically take the car home on the weekend. A few days later, they call saying, “Your auto loan was not approved at that rate; you must come back and sign a new (more expensive) contract.” To avoid this: Do not take the keys until you receive the direct ‘Final Approval’ document from the bank.

- Packed Payments: The dealer artificially inflates your quoted EMI (e.g., $450 instead of $400). When you easily agree to the $450, they silently ‘pack’ hidden warranties and add-ons into that $50 per month difference. This is why you must always negotiate strictly on the OTD price, never the EMI.

- Monthly Payment Syndrome (Negative Equity Cycle): If you are ‘underwater’ on your old car (meaning the outstanding debt is higher than the car’s current value), the dealer will roll that remaining debt over into your new auto loan. This is considered a highly toxic cycle in the financial world. Always try to clear the debt on your old car first before trading it in.

Crucial US Finance Terminology to Understand

Before officially starting the process of securing an auto loan, it is absolutely essential to deeply understand these specific American financial terms. Dealerships often use complex financial jargon to confuse buyers and maximize their own profits. Mastering this vocabulary ensures that you remain in complete control of your auto loan agreement from start to finish.

1. APR (Annual Percentage Rate) The APR represents the actual, true annual cost of borrowing money from a financial institution. Unlike a simple base interest rate, the APR on an auto loan includes not just the interest, but also any mandatory processing fees, origination fees, or hidden lender charges. Comparing different APRs is the single most accurate way to find the cheapest financing available in the market.

2. MSRP (Manufacturer’s Suggested Retail Price) This is commonly known in the industry as the “sticker price” of the car. It is simply the price the manufacturer highly recommends the dealer sell the vehicle for. You should almost never buy a vehicle at the full MSRP. Instead, treat it strictly as the starting point for your negotiations before locking in the total amount for your auto loan.

3. OTD (Out-the-Door Price) This is the most critical number in the entire car-buying process. The OTD price is the absolute final, total cost of the vehicle to legally drive it off the lot. It includes the negotiated price of the car, plus state sales tax, title transfer fees, registration costs, and all dealership documentation fees. You must always negotiate with the dealer based on the OTD price, and your final auto loan must be based strictly on this exact number, never on the desired monthly payment.

4. Down Payment A down payment is the initial upfront cash you pay directly to the dealership out of your own pocket on the day of the purchase. In the US market, financial experts strongly recommend making a down payment of at least 10% to 20% of the vehicle’s total cost. A larger down payment immediately reduces the principal amount of your auto loan, which in turn lowers your monthly installments and drastically decreases the total interest you will pay to the bank over time.

5. GAP Insurance (Guaranteed Asset Protection) Cars depreciate very quickly. If you buy a brand-new vehicle and it gets stolen or completely “totaled” in a severe accident just a few months later, your standard vehicle insurance will only pay you the current depreciated market value of the car. If you still owe more money to the bank than the car is actually worth, GAP insurance steps in. It strictly covers the financial difference between the car’s current cash value and the remaining balance on your auto loan. Having this protects you from paying thousands of dollars out of pocket for a destroyed vehicle, making your overall auto loan experience financially safer.

The Impact of Credit Scores on Interest Rates

In the world of auto loans, your credit score (FICO Score) is your most powerful weapon. It ultimately determines exactly how much extra money you will end up paying to the lender over the life of your loan. interest rates vary significantly depending on where you fall within the different credit tiers.

Here is a detailed breakdown of how your credit score dictates your auto loan rates:

Note: The Super Prime category is considered the safest tier by lenders, rewarding borrowers with fantastic, market-leading rates. On the other hand, Deep Subprime borrowers face a massive interest burden.

Top 10 Auto Loan FAQs for US Car Buyers

Q1: What is the first step before applying for a vehicle financing plan?

Answer: The first step is to check your credit score, as it directly impacts your Auto Loan interest rate and approval chances.

Q2: How much down payment is recommended in the US?

Answer: A 20% down payment is highly ideal to secure a better Auto Loan term and prevent negative equity on your new vehicle.

Q3: Should I get financing from the dealership or a bank?

Answer: It is always smarter to get pre-approved for an Auto Loan from a bank or credit union before visiting the dealership.

Q4: What is the recommended duration for repayment?

Answer: Financial experts suggest keeping your Auto Loan duration to 48 or 60 months maximum to avoid paying excessive interest.

Q5: What is the classic 20/4/10 budgeting rule?

Answer: It means 20% down, a 4-year term, and keeping your Auto Loan payments plus car insurance under 10% of your monthly income.

Q6: How does the Annual Percentage Rate (APR) affect my monthly bills?

Answer: A higher APR increases your total interest, making the overall cost of your Auto Loan significantly more expensive over time.

Q7: Can I negotiate the interest rate at the dealership?

Answer: Yes, you can use your pre-approved Auto Loan offer to force the dealership’s finance department to beat your bank’s rate.

Q8: What happens if I choose a 72-month or 84-month term?

Answer: Longer terms lower your monthly bill, but you risk being underwater on your Auto Loan, owing more money than the car’s actual worth.

Q9: Do I really need gap insurance for my car?

Answer: If your down payment is low, gap insurance covers the difference between your vehicle’s value and your remaining Auto Loan balance if totaled.

Q10: Can immigrants without a credit history get vehicle financing in the US?

Answer: Yes, specialized lenders and programs can approve an Auto Loan using alternative data, a co-signer, or your US work visa and employment offer.