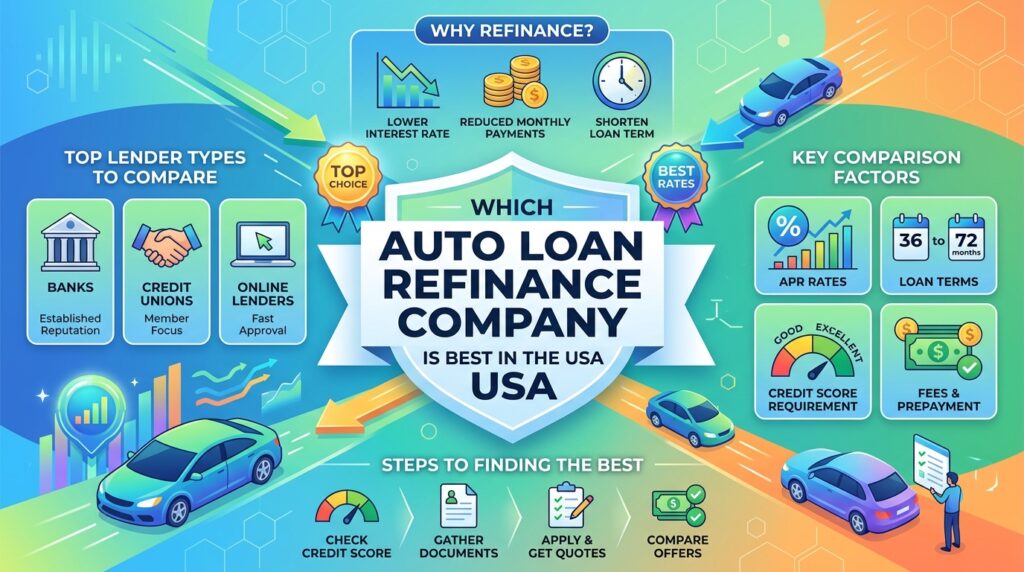

Which Auto Loan Refinance Company Is Best in the USA?

The United States offers many excellent Auto Loan Refinance options for drivers looking to reduce their monthly payments or secure a lower interest rate. These providers generally fall into two categories: Direct Lenders and Online Marketplaces.

Direct Lenders—such as banks, credit unions, and specialized finance companies—provide refinancing loans directly to borrowers. Online Marketplaces, on the other hand, allow consumers to compare offers from multiple lenders on a single platform, making it easier to find competitive rates.

It’s important to understand that Auto Loan Refinance rates are not fixed. Annual Percentage Rates (APR) can change frequently based on several factors, including Federal Reserve policies, market conditions, your credit score, income, debt-to-income ratio, and the age and mileage of your vehicle.

While interest rates vary from borrower to borrower, most lenders clearly define their refinancing criteria, including minimum credit score requirements, loan amount limits, repayment terms, vehicle eligibility rules, and associated fees. Comparing these factors carefully can help you choose the best Auto Loan Refinance company for your financial situation and maximize your potential savings.

1. AutoPay – Marketplace

- Minimum Credit Score: 575

- Loan Amount: $2,500 to $100,000

- Loan Term: 24 to 84 months

- Pros:

- Allows you to compare rates from multiple lenders at once.

- Options are available in its network even for those with bad or average credit scores.

- Offers ‘cash-back’ auto loan refinance options.

- Cons:

- You may have to pay an origination fee (processing fee) when taking a loan through AutoPay.

- Applying may result in many marketing emails and calls from partner companies.

2. RateGenius – Marketplace

- Minimum Credit Score: 550

- Loan Amount: $10,000 to $90,000

- Loan Term: 24 to 72 months

- Pros:

- Offers highly competitive interest rates due to a network of over 150 credit unions and banks.

- The company handles the entire process of paying off your old loan and transferring the vehicle title.

- Cons:

- The minimum loan amount ($10,000) is quite high, making it unsuitable for smaller loans.

- A ‘hard credit pull’ is required to view exact rates, which may slightly lower your credit score.

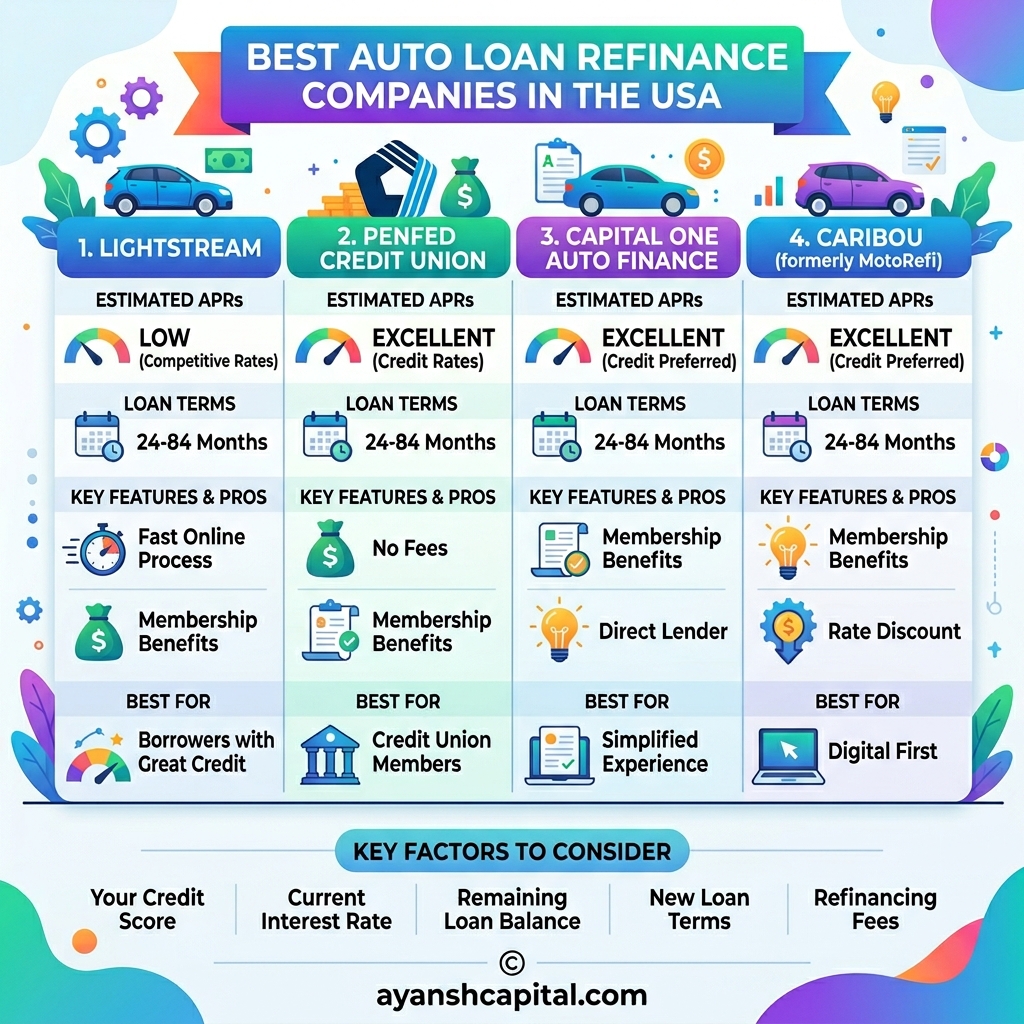

3. PenFed Credit Union – Direct Lender

- Minimum Credit Score: 650 (Estimated)

- Loan Amount: $500 to $150,000

- Loan Term: 36 to 84 months

- Pros:

- Allows you to refinance very small loan amounts (as low as $500).

- Offers some of the lowest APRs in the market for those with good credit scores.

- Cons:

- You must become a PenFed member to get a loan (though membership only requires opening a deposit account with a $5 minimum).

- Strict credit requirements; it is difficult for applicants with lower credit scores to get approved.

4. Capital One Auto Finance – Direct Lender

- Minimum Credit Score: 500

- Loan Amount: $7,500 to $50,000

- Loan Term: Up to 72 months

- Pros:

- Offers pre-qualification via a ‘soft credit check’, allowing you to see your potential rates without affecting your credit score.

- The process is completely online and transparent, with excellent customer service.

- Cons:

- Not available in Alaska and Hawaii.

- It does not offer an auto loan refinance for certain specific vehicle types (like heavy commercial vehicles or very old cars).

5. RefiJet – Full-Service Marketplace

- Minimum Credit Score: 500

- Loan Amount: $5,000 to $150,000

- Loan Term: 24 to 84 months

- Pros:

- Allows adding a co-signer, which can help secure better rates.

- Offers a payment deferral option, allowing you to skip your loan installment for the first 2 months after your auto loan refinance.

- Cons:

- The process is not 100% online; speaking with a customer service representative over the phone is mandatory to finalize the loan.

- A lump-sum processing fee may be added to your loan.

6. Upstart – AI-Based Lender

- Minimum Credit Score: 510

- Loan Amount: $9,000 to $60,000

- Loan Term: 24 to 84 months

- Pros:

- Does not rely solely on credit scores; its AI model can also approve loans based on your education and employment history.

- Excellent for individuals with a very short credit history (thin credit file).

- Cons:

- Interest rates can be very high for those with poor credit (sometimes exceeding 29%).

- Its auto loan refinance service is not available in certain states like Nevada (NV) and Maryland (MD).

7. Caribou (formerly MotoRefi) – Marketplace

- Minimum Credit Score: 650

- Loan Amount: $10,000 to $100,000

- Loan Term: 36 to 72 months

- Pros:

- Primarily partners with local credit unions and community banks, resulting in lower interest rates.

- The online application process is very fast and user-friendly.

- Cons:

- Charges a fixed processing fee (around $399) on every loan.

- Strict vehicle rules: the car must not be more than 10 years old and must not exceed 120,000 miles.

8. LightStream – Direct Lender

- Minimum Credit Score: 660 (Only for Good to Excellent Credit)

- Loan Amount: $5,000 to $100,000

- Loan Term: 24 to 84 months

- Pros:

- Does not charge any origination fees, late fees, or pre-payment penalties.

- No restrictions on vehicle age, mileage, or make/model.

- If approved early in the day, funds are transferred to your bank account on the same day.

- Cons:

- No pre-qualification option; a direct hard credit check is required to view rates.

- Only available to customers with excellent credit profiles.

9. Bank of America – Direct Lender

- Minimum Credit Score: Not publicly disclosed (Generally 650+)

- Loan Amount: Starting from $7,500 ($8,000 in Minnesota)

- Loan Term: 48 to 72 months

- Pros:

- Existing Bank of America customers receive an interest rate discount of 0.25% to 0.50% (under the Preferred Rewards program).

- Lease buyout loans are easily accessible.

- Cons:

- A hard credit inquiry is required to apply.

- The vehicle must not be more than 10 years old and must have less than 125,000 miles.

10. Ally Clearlane – Marketplace

- Minimum Credit Score: 520

- Loan Amount: $7,500 to $100,000

- Loan Term: 36 to 75 months

- Pros:

- Accepts applicants with low credit scores.

- Pre-qualification is available with a soft credit check.

- Offers GAP (Guaranteed Asset Protection) insurance alongside refinancing.

- Cons:

- Interest rates and fees depend on the specific partner lender you match with.

- It is not available in Nevada and Washington, D.C.

11. Chase Auto – Direct Lender

- Minimum Credit Score: Not publicly disclosed (generally 650 or higher)

- Loan Amount: $4,000 to $100,000

- Loan Term: 12 to 84 months

- Pros:

- It is one of the largest banks in the US. If you already have an account with Chase Bank, you can get a rate discount through auto-pay, and management becomes very easy.

- It does not charge any origination fee (processing fee) or pre-payment penalty (penalty for paying off the loan early).

- Cons:

- It does not offer a ‘soft credit check’ facility to view rates; a ‘hard credit check’ is done directly as soon as you apply.

- The car’s age must be less than 10 years, and mileage must be less than 120,000 miles. It does not refinance commercial vehicles.

12. iLending – Marketplace / Broker

- Minimum Credit Score: 510

- Loan Amount: $7,500 to $150,000

- Loan Term: 24 to 84 months

- Pros:

- This company assigns you a ‘Personal Loan Consultant’ who helps you through the entire process over the phone.

- It is a good option for those with poor credit scores and allows adding a co-signer.

- Cons:

- iLending charges an origination fee (processing fee) of approximately $399 to $499, which is often added to your new loan amount.

- The process is not 100% online; speaking with a consultant over the phone is mandatory.

13. Consumers Credit Union (CCU) – Direct Lender

- Minimum Credit Score: 640

- Loan Amount: No set minimum (usually $5,000 to $100,000+)

- Loan Term: Up to 84 months

- Pros:

- Compared to many traditional banks, it shows flexibility in refinancing even very old models (old cars).

- It is known for providing its members with some of the best and lowest interest rates (APRs) in the market.

- Cons:

- You must become a CCU member to finalize the loan (which requires opening an account by paying a one-time fee of $5).

- It requires a ‘hard credit check’.

14. Gravity Lending – Marketplace

- Minimum Credit Score: 600

- Loan Amount: $10,000 to $150,000

- Loan Term: 24 to 84 months

- Pros:

- Its customer service ratings are excellent, and it provides bilingual support.

- It keeps the process completely digital and quickly handles the task of paying off the old lender.

- Cons:

- Its minimum loan amount ($10,000) is very high. If you need to refinance a remaining loan of $5,000 or $7,000 on your car, you cannot apply here.

- You may have to pay a fixed fee when taking a loan through its partner network.

15. MyAutoLoan – Marketplace

- Minimum Credit Score: 575

- Loan Amount: $8,000 to $100,000

- Loan Term: 24 to 72 months

- Pros:

- Its online platform is very fast. Once you apply, you receive offers from 4 different lenders within minutes.

- It also offers great options for lease-buyouts and buying a car from a private party.

- Cons:

- It does not offer its services in the US states of Hawaii and Alaska.

- Its most attractive and lowest interest rates are only available to applicants with a credit score of 730 or higher.

16. Tresl – Full-Service Marketplace

- Minimum Credit Score: Around 500 to 550

- Loan Amount: $5,000 to $100,000 (depends on the lender)

- Loan Term: 24 to 84 months

- Pros:

- Provides a dedicated Financial Advisor to guide you through the entire process.

- The company handles all the paperwork for paying off your car’s old loan and transferring the title at the state’s DMV (Department of Motor Vehicles).

- Cons:

- Its partner lenders often charge an origination fee on the loan.

- You cannot complete this process 100% online; speaking over the phone is required to finalize the loan.

17. USAA – Direct Lender (for Military Members)

- Minimum Credit Score: Not publicly disclosed (generally 600+)

- Loan Amount: $5,000 to $100,000 (estimated)

- Loan Term: 12 to 84 months

- Pros:

- Does not charge any application fee or processing fees.

- One of the most reputable and trusted companies in the US in terms of customer service.

- Cons:

- Not available to the general public. Its services are limited only to active-duty US military members, veterans, and their families.

- The interest rate may be slightly higher if you do not opt for the auto-pay option.

18. Navy Federal Credit Union – Direct Lender

- Minimum Credit Score: Not publicly disclosed (flexible for members)

- Loan Amount: Starting from $250

- Loan Term: 36 to 96 months (offers very long loan options)

- Pros:

- Its minimum loan amount ($250) is the lowest in the market, making it excellent for refinancing very small remaining loans.

- One of the financial institutions offering some of the lowest interest rates (APRs) in the market.

- Cons:

- Like USAA, its membership is reserved only for military personnel, Department of Defense (DoD) employees, and their families.

- Choosing a long loan term like 84 or 96 months results in paying a lot of interest over the long run.

19. LendingTree – Marketplace

- Minimum Credit Score: No strict minimum (the platform finds lenders according to your profile)

- Loan Amount: $1,000 to $100,000

- Loan Term: 12 to 84 months

- Pros:

- You can view offers from 5 different lenders simultaneously through a ‘soft credit check’ (which does not drop your credit score).

- It has the largest network of lenders in the US.

- Cons:

- It is a lead-generation platform. After applying, you may face a high volume of marketing calls and emails from various lenders.

- The final customer service experience will depend on the bank that approves your loan, not LendingTree.

20. PNC Bank – Direct Lender

- Minimum Credit Score: Typically 650 or higher

- Loan Amount: $7,500 to $100,000

- Loan Term: 12 to 72 months

- Pros:

- PNC Bank offers a traditional and highly stable banking experience.

- You can choose your desired loan amount and term for refinancing, and the entire process is transparent.

- Cons:

- Does not offer a ‘soft credit check’ pre-qualification; a ‘hard credit inquiry’ is required to know the rates.

- Its interest rates (APRs) may be slightly higher compared to credit unions, and it does not offer some of its specific services in all 50 US states.

21. U.S. Bank – Direct Lender

- Minimum Credit Score: 660 (generally requires good credit)

- Loan Amount: $5,000 to $100,000

- Loan Term: 12 to 72 months

- Pros:

- It does not charge any origination fee or pre-payment penalty.

- If you already have a checking or savings account with U.S. Bank, you may receive a special discount on interest rates.

- Cons:

- It does not offer a ‘soft credit check’ facility to view rates; a ‘hard credit inquiry’ occurs immediately upon applying.

- Your car must not be more than 10 years old and its mileage must be under 100,000 miles, which is a slightly stricter condition compared to other lenders.

22. OpenRoad Lending – Direct Lender / Broker

- Minimum Credit Score: 500

- Loan Amount: $7,500 to $100,000

- Loan Term: 36 to 84 months

- Pros:

- It is an excellent option for people with bad or very low credit scores and helps them get loans approved.

- It also offers a ‘cash-out refinance’ feature, which means if your car’s current value is higher than the loan, you can get some cash back by refinancing.

- Cons:

- Its services are not available in Hawaii, Alaska, and a few other states.

- It does not refinance specific car brands like Oldsmobile, Daewoo, and Suzuki.

23. Digital Federal Credit Union (DCU) – Direct Lender

- Minimum Credit Score: Not publicly disclosed (generally 620+)

- Loan Amount: No set minimum limit (you can choose according to your needs)

- Loan Term: Up to 84 months

- Pros:

- It offers a special discount on the interest rate (APR) when you refinance electric vehicles (EVs) and energy-efficient cars.

- It provides the option to defer the first loan payment for up to 65 days (payment deferral).

- Cons:

- You must become a member of DCU to get a loan (though anyone can become a member by making a $10 donation to a partner charity).

- A ‘hard credit check’ is required to apply.

24. LendingClub – Direct Lender

- Minimum Credit Score: 600

- Loan Amount: $4,000 to $55,000

- Loan Term: 24 to 72 months

- Pros:

- Through a ‘soft credit check’, you can see if you pre-qualify in minutes without lowering your credit score.

- The entire process is very fast and 100% online.

- Cons:

- The maximum loan limit is only $55,000, which may not be sufficient for an auto loan refinance on expensive luxury cars or heavy vehicles.

- You may have to pay a fixed origination fee on the loan, which is added to your total loan amount.

25. Wells Fargo Auto – Direct Lender

- Minimum Credit Score: Not publicly disclosed (generally 600 or higher)

- Loan Amount: $5,000 to $100,000

- Loan Term: 24 to 72 months

- Pros:

- Being one of the largest banks in America, its stability and customer service are excellent.

- The refinance process is very easy for existing Wells Fargo customers, and there are no hidden fees.

- Cons:

- There is no online pre-qualification option; you have to submit a formal application (hard credit check) to view rates.

- Its rules regarding the vehicle’s condition and mileage are quite strict.

26. National Auto Loan Network (NALN) – Broker/Marketplace

- Minimum Credit Score: 600

- Loan Amount: Starting from $8,000

- Loan Term: 24 to 84 months

- Pros: This is an excellent network where customer service is available seven days a week. A single application gives you rates from multiple lenders, and it also offers the option to bundle auto insurance with the loan.

- Cons: A processing fee of approximately $499 may be charged on your loan by the lender. To proceed with an auto loan refinance here, your minimum annual income must be at least $18,000.

27. Auto Approve – Marketplace

- Minimum Credit Score: 580

- Loan Amount: Minimum $8,000

- Loan Term: 12 to 84 months

- Pros: This company is specifically focused on auto loan refinance. It handles closing your old bank loan and the DMV (Department of Motor Vehicles) title transfer paperwork in a highly streamlined manner. Along with cars, it also refinances motorcycles and RVs (recreational vehicles).

- Cons: Since it does not lend money directly itself, it may have a fixed broker fee that gets added to your new loan. You do not get the option for pre-qualification through a ‘soft credit check’.

28. First Tech Federal Credit Union – Direct Lender

- Minimum Credit Score: Not publicly disclosed (generally 650+)

- Loan Amount: Over $5,000

- Loan Term: 12 to 84 months

- Pros: If you refinance your car loan from another lender to First Tech, it offers a special discount of 0.50% on the approved interest rate (APR). There are no origination fees or pre-payment penalties, and it offers a ‘soft credit check’ (Check My Rate) feature without dropping your credit score.

- Cons: It is mandatory to get its membership to take a loan from here. If your credit history is very short (thin credit), you may face difficulty in approval.

29. Alliant Credit Union – Direct Lender

- Minimum Credit Score: 640

- Loan Amount: Minimum starting from $4,000

- Loan Term: 12 to 84 months

- Pros: It is known for its easy and completely digital online process. After approval, funds are sent directly to your old lender (from whom you took the previous loan) ‘overnight’, resulting in a quick loan closure.

- Cons: If you choose a long loan term like 84 months (7 years) to lower your installments, the interest rates (APR) become 1% higher. Its terms also change based on the age of the used car.

30. Truliant Federal Credit Union – Direct Lender

- Minimum Credit Score: 600 (Estimated)

- Loan Amount: Starting from $5,000

- Loan Term: 36 to 96 months (offers long loan options)

- Pros: It provides a unique feature to refinance ‘classic cars’ that are more than 20 years old. The biggest advantage is that it gives you an excellent option to skip one car installment every calendar year (Skip-A-Pay) during times of financial hardship.

- Cons: For classic cars older than 20 years, interest rates are very high (generally between 10.49% and 18.00%). Like other credit unions, it is necessary to become a member before taking a loan.

31. Innovative Funding Services (IFS) – Marketplace / Broker

- Minimum Credit Score: Approximately 500 (available for those with bad credit)

- Loan Amount: $5,000 to $150,000

- Loan Term: 36 to 84 months

- Pros:

- It is a full-service broker with 100% online options.

- The company handles all complex paperwork for your Auto Loan Refinance, such as paying off the old lender and transferring the car title at the DMV (Department of Motor Vehicles).

- It also offers excellent options for lease buyouts.

- Cons:

- This company charges a large processing fee (often $399 or more) for its brokerage services, which is usually added to the total amount of your new loan.

32. Truist Bank – Direct Lender

- Minimum Credit Score: 600 (Estimated)

- Loan Amount: $5,000 to $125,000

- Loan Term: 24 to 84 months

- Pros:

- It is a very stable and trusted traditional bank in the US.

- It does not charge any kind of pre-payment penalty (penalty for paying off the loan early).

- The process is very fast, often resulting in same-day funding.

- Cons:

- If your current car loan is also with Truist Bank, you must have paid the first 6 months of installments before you can get an Auto Loan Refinance with them.

- Additionally, a ‘hard credit check’ occurs when applying online to view rates.

33. OneMain Financial – Direct Lender (Specialized for Bad Credit)

- Minimum Credit Score: No set minimum limit (available even for very bad credit)

- Loan Amount: $1,500 to $30,000

- Loan Term: 24 to 60 months

- Pros:

- This is an excellent option for those with a very poor credit history or a score below 600.

- Its loan amount starts at just $1,500, which is highly useful for an Auto Loan Refinance on very small remaining car loans.

- They have over 1,300 physical branches across the US where you can receive in-person service.

- Cons:

- Due to the high risk of lending to individuals with bad credit, their interest rates (APRs) are among the highest in the market (sometimes up to 35.99%).

- Additionally, they can charge heavy origination fees ranging from 1% to 10%.

- The maximum loan limit is only $30,000.

34. Golden 1 Credit Union – Direct Lender

- Minimum Credit Score: Not publicly disclosed (generally flexible for members)

- Loan Amount: No set maximum limit (depends on your vehicle’s value)

- Loan Term: Typically up to 84 months

- Pros:

- It gives qualified borrowers with good credit 90 days (payment deferral) to make their first installment after they complete their Auto Loan Refinance.

- If you have been a member for more than 7 months, you receive an additional 0.25% discount on the approved interest rate.

- Cons:

- You must become a member of this credit union for the loan to be approved.

- Its roots are primarily in the state of California, so vehicle registration conditions (like smog certificates) can be strict in certain states.

35. Tenet – Specialized Electric Vehicle (EV) Lender

- Minimum Credit Score: 620

- Loan Amount: $10,000 to $150,000

- Loan Term: 36 to 84 months

- Pros:

- This is an excellent modern lender in the US built specifically to refinance only Electric Vehicles (EVs) and plug-in hybrid cars.

- It provides loans by considering your EV’s battery health and Tax Credits, unlike standard gas-powered cars.

- The entire process is transparent, and a ‘soft credit check’ feature is available.

- Cons:

- It does not refinance gas-powered (petrol or diesel) cars.

- Its minimum loan amount ($10,000) is quite high, so it is not useful for small loans.

- It is not available in all 50 US states.

36. Lantern by SoFi – Marketplace

- Minimum Credit Score: No strict limit (usually above 500)

- Loan Amount: $5,000 to $100,000

- Loan Term: 24 to 84 months

- Pros:

- This is a marketplace operated by the renowned US financial company, SoFi.

- It offers a ‘soft credit check’, allowing you to view offers from multiple lenders simultaneously without lowering your credit score.

- Cons:

- Since it is a lead-generation platform, you may receive numerous marketing emails or phone calls from partner lenders after applying.

- Your final interest rate and fees will depend on the bank you choose for your Auto Loan Refinance.

37. Santander Consumer USA – Direct Lender

- Minimum Credit Score: No set minimum limit (specialized for bad credit)

- Loan Amount: $5,000 to $75,000

- Loan Term: Up to 72 months

- Pros:

- It is one of the largest companies in the US for ‘subprime’ auto loans.

- If your credit score is very low, you have a history of bankruptcy, or you lack a credit history, the chances of getting an Auto Loan Refinance approved here are the highest.

- Cons:

- Due to the high risk involved, their interest rates (APRs) are significantly higher than the market average.

- Historically, there have been mixed customer reviews regarding their customer service.

38. BMO Bank – Direct Lender

- Minimum Credit Score: Usually 650 or higher

- Loan Amount: $5,000 to $100,000

- Loan Term: 12 to 75 months

- Pros:

- This is a major and highly stable traditional bank in the US.

- If you set up Auto-Pay for your monthly installments, it offers an attractive 0.50% discount on the interest rate.

- It does not charge any hidden origination fees.

- Cons:

- It does not offer an online pre-qualification option to check rates; you must submit a formal application directly, which results in a ‘hard inquiry’ on your credit report.

- The age of the vehicle must be less than 10 years to qualify for an Auto Loan Refinance.

39. Connexus Credit Union – Direct Lender

- Minimum Credit Score: 640 (Estimated)

- Loan Amount: $5,000 to over $100,000

- Loan Term: Up to 84 months

- Pros:

- It is a widely popular credit union for auto loans across the US.

- For individuals with excellent credit, it offers much lower interest rates compared to traditional banks.

- Its overall process is highly transparent.

- Cons:

- You must become a member to secure a loan (if you are not part of a specific eligible group, you can join by making a one-time $5 donation to the Connexus Association).

- A hard credit check is required to apply.

40. Upgrade – Direct Lender

- Minimum Credit Score: Around 600

- Loan Amount: $10,000 to $65,000

- Loan Term: 24 to 84 months

- Pros:

- It is a modern FinTech company that provides a very fast online process.

- You can check your potential rates without lowering your credit score (via a ‘soft pull’).

- If you open a checking account with them, they provide an additional rate discount.

- Cons:

- The maximum loan limit is only $65,000, which may not be enough to secure an Auto Loan Refinance on expensive trucks or luxury vehicles.

- It may charge an origination fee (processing fee) depending on your approved loan profile.

42. Avant

- Minimum Credit Score: 580

- Loan Amount: $5,000 to $55,000

- Loan Term: 24 to 72 months

- Pros: It is an emerging FinTech company that provides very fast approvals using its AI model. Its mobile app is highly modern, allowing you to manage your entire loan. It also offers a ‘soft credit check’ feature.

- Cons: Its maximum loan limit is low ($55,000). Interest rates (APRs) may be slightly higher compared to traditional credit unions.

43. Credit Karma – FinTech Marketplace

- Minimum Credit Score: No set minimum (depends on profile)

- Loan Amount: $4,000 to $100,000+

- Loan Term: Depends on the partner lender

- Pros: This is a highly popular FinTech app in the US. If you use it, it performs an automated analysis of your credit profile to show pre-approved auto loan refinance offers, which are accurate in 99% of cases.

- Cons: It is not a lender itself. You may receive many promotional and marketing notifications (emails/calls) from their platform.

44. Westlake Financial

- Minimum Credit Score: No minimum score (available even with no credit history)

- Loan Amount: $3,000 to $50,000

- Loan Term: 24 to 72 months

- Pros: It is one of the largest subprime lenders in the US. It fully helps refinance those who have very poor credit scores or who have recently had a bankruptcy discharged.

- Cons: Due to lending to high-risk customers, its interest rates (APR) can be extremely high (sometimes up to 29.99%). It does not offer cheap rates like traditional banks.

45. Prestige Financial

- Minimum Credit Score: No minimum

- Loan Amount: $5,000 to $35,000 (Maximum)

- Loan Term: Up to 72 months

- Pros: If an applicant’s credit score is below 500 or if they have defaulted on a loan in the past, this company serves as a ‘last resort’ for them. It also allows adding a joint application (co-applicant).

- Cons: Its loan limit is restricted to only $35,000. You will always have to pay a high interest rate (High APR) with this company.

46. BECU (Boeing Employees Credit Union)

- Minimum Credit Score: Around 640

- Loan Amount: Starting from $5,000 (No set maximum limit)

- Loan Term: Up to 84 months

- Pros: It is the fourth largest credit union in the US. The most unique feature is that as your credit score improves, BECU automatically lowers your loan’s interest rate (under its Reprice program). It does not charge any processing fees.

- Cons: Its membership rules are strict. It is primarily available only to residents of Washington state or employees of the Boeing company and their families.

47. Bethpage Federal Credit Union

- Minimum Credit Score: 650 (Estimated)

- Loan Amount: Minimum starting from $1,000

- Loan Term: 12 to 84 months

- Pros: Its minimum loan limit is only $1,000, which is excellent for completing an auto loan refinance on very small remaining car loans. It offers highly attractive and some of the lowest market rates for those with excellent credit.

- Cons: There is no online ‘soft pull’ feature to check rates here; a ‘hard inquiry’ occurs directly on the credit report as soon as you apply.

48. CarsDirect – Broker Network

- Minimum Credit Score: 500 (Excellent broker for bad credit)

- Loan Amount: $5,000 to $50,000

- Loan Term: Depends on the partner lender

- Pros: CarsDirect not only helps with buying new cars, but it is also a fantastic and fast broker network to find an auto loan refinance lender for people with subprime (bad) credit.

- Cons: Since it is a broker, you may have to pay a one-time brokerage fee (processing fee). It is not very useful for people with good credit (700+), as direct banks are better for them.

49. NerdWallet Marketplace

- Minimum Credit Score: 550

- Loan Amount: $5,000 to $100,000

- Loan Term: 24 to 84 months

- Pros: It is a highly reputable financial research website in the US that has its own secure ‘partner network’. Through its platform, you can view multiple secure and ‘pre-qualified’ offers simultaneously.

- Cons: It does not extend loans itself, so the entire post-approval customer service, paperwork, and policies will belong to the third-party lender (bank) you select from this platform.

50. Monevo – Marketplace

- Minimum Credit Score: 580

- Loan Amount: $1,000 to $100,000

- Loan Term: 12 to 84 months

- Pros: This is a highly powerful online marketplace for an auto loan refinance that scans databases of over 30 different US lenders (banks and credit unions) within minutes to find the best rates for you. The ‘soft credit check’ facility is fully available.

- Cons: Since more than 30 partners are connected, you may receive a flood of marketing messages from third-party banks on your phone and email once you apply.

51. Fifth Third Bank

- Minimum Credit Score: 650 (Estimated)

- Loan Amount: $5,000 to $100,000

- Loan Term: 12 to 75 months

- Pros: If you already have a checking or savings account with this bank, you get an additional 0.25% discount on your interest rate (APR). It does not charge any origination fee for the loan.

- Cons: The ‘soft credit check’ feature is not available, so a ‘hard inquiry’ is made on your credit report to find out the rates. It is more active in select states like Ohio, Michigan, and Florida.

52. Citizens Bank

- Minimum Credit Score: 680 (Good credit required)

- Loan Amount: $5,000 to $100,000

- Loan Term: 36 to 72 months

- Pros: Its digital and mobile banking experience is excellent. It offers some of the most stable and lowest rates among traditional banks for customers with high credit scores looking for an Auto Loan Refinance.

- Cons: Its minimum credit score requirement (680) is slightly higher than the market average. It does not offer its auto loan services in all 50 US states.

53. Huntington National Bank

- Minimum Credit Score: 660

- Loan Amount: Starting from $5,000

- Loan Term: Up to 72 months

- Pros: This bank is known for its excellent customer service and ‘transparent’ loan terms. If you are 24 hours late paying a loan installment, it provides a ‘grace period’ and does not immediately charge a late fee.

- Cons: Its network is primarily limited to the Midwest region of the US. It does not refinance very old or high-mileage vehicles.

54. Suncoast Credit Union

- Minimum Credit Score: 600

- Loan Amount: Depends on your vehicle’s value (LTV – Loan-to-Value)

- Loan Term: Up to 72 months

- Pros: Since it is a non-profit institution, it returns its earnings to its members in the form of lower interest rates. Its rates (APRs) are much lower compared to many large commercial banks.

- Cons: Its membership is quite limited. Primarily, only people who live or work in specific Florida counties can become members.

55. Mountain America Credit Union (MACU)

- Minimum Credit Score: Around 600

- Loan Amount: No minimum limit set

- Loan Term: Up to 84 months

- Pros: This credit union allows you to complete the Auto Loan Refinance process entirely online, which is rare among credit unions. It also offers a payment deferral of up to 90 days to pay the first installment.

- Cons: There are rules to become a member. Although it is concentrated in Utah and surrounding states, you can also become a member by donating to specific charities, which takes a little extra time.

56. Credible

- Minimum Credit Score: 600

- Loan Amount: $4,000 to $100,000

- Loan Term: 24 to 84 months

- Pros: Credible is a highly trusted marketplace in the US. Its biggest feature is its ‘Best Rate Guarantee’—if you find a better rate elsewhere, they give you a $200 bonus under certain conditions. The ‘soft pull’ feature is 100% available.

- Cons: Credible does not lend to you directly. When you accept an offer from a partner lender for an Auto Loan Refinance, all further work (like customer service and payments) shifts to that partner lender.

57. SuperMoney

- Minimum Credit Score: No set minimum (options for various profiles)

- Loan Amount: $5,000 to $100,000

- Loan Term: Depends on the partner lender

- Pros: It is an excellent financial comparison engine. It not only shows rates but also displays ‘User Ratings’ and reviews for each lender, making decision-making easier.

- Cons: Upon applying, it sends your data to multiple lenders, which may result in continuous calls and emails from several third-party companies.

58. Auto Credit Express

- Minimum Credit Score: No minimum limit (even with no credit)

- Loan Amount: Depends on vehicle type and income

- Loan Term: 24 to 72 months

- Pros: This is the largest network in the US for people who have had a vehicle repossession in the past or who have gone bankrupt. It prioritizes your monthly income (at least $1,500/month) more than your credit history.

- Cons: It is a broker network that connects you with specialized subprime dealerships or lenders. Because of this, interest rates are extremely high.

59. RoadLoans

- Minimum Credit Score: Even those below 500 can apply

- Loan Amount: $5,000 to $75,000

- Loan Term: Up to 72 months

- Pros: This is a direct subprime lender owned by ‘Santander Consumer USA’ (Santander). It provides an instant decision on online applications and allows bad credit customers to add a co-applicant for their Auto Loan Refinance.

- Cons: Its interest rates (APRs) are very expensive, and it often adds an ‘origination fee’ (processing fee) to the amount of your new loan.

60. Fiona

- Minimum Credit Score: 580

- Loan Amount: $5,000 to $100,000

- Loan Term: 24 to 84 months

- Pros: This is a very modern and fast AI-powered search engine. With just a 60-second form, you can view real-time offers from top US lenders without dropping your credit score.

- Cons: It is an aggregator. Fiona only acts as a bridge; once you choose an offer, you still have to go to that specific bank’s website and undergo a ‘hard credit check’ for the final approval.

61. KeyBank

- Score / Amount: 650+ / $5,000 to $100,000

- Pros: If you have a KeyBank account, you get an extra rate discount on auto-pay for your Auto Loan Refinance. There is no pre-payment penalty.

- Cons: Only available in the 15 states where they have physical branches.

62. TD Bank

- Score / Amount: 680+ / $7,500 to $100,000

- Pros: Has a large network on the East Coast. Their customer service for an Auto Loan Refinance is available seven days a week.

- Cons: A hard credit check is mandatory, and their rules on vehicle age are quite strict.

63. M&T Bank

- Score / Amount: 660+ / $5,000 to $100,000

- Pros: Provides excellent customer service and a local banking experience for your Auto Loan Refinance. Rates are transparent.

- Cons: No pre-qualification option; the online interface is a bit outdated.

64. BOK Financial

- Score / Amount: 650+ / $5,000 to $75,000

- Pros: This is a very stable and trusted institution for an Auto Loan Refinance in the Southwest US.

- Cons: Geographically limited. The maximum loan limit ($75,000) may fall short for expensive vehicles.

65. First Citizens Bank

- Score / Amount: 680+ / $10,000 to $100,000

- Pros: Offers some of the best rates (Low APR) in the market to customers with high credit for an Auto Loan Refinance.

- Cons: Does not process loans under $10,000.

66. Synovus Bank

- Score / Amount: 660+ / $5,000 to $100,000

- Pros: Strong presence in the Southeast US. No hidden fees during the Auto Loan Refinance process.

- Cons: High reliance on branches; lacks a fully digital experience.

67. Commerce Bank

- Score / Amount: 650+ / $5,000 to $100,000

- Pros: Features long loan terms (up to 72 months) and easy approval during the Auto Loan Refinance.

- Cons: Limited to Missouri, Kansas, Illinois, and a few neighboring states.

68. Frost Bank

- Score / Amount: 680+ / $5,000 to $100,000

- Pros: Concentrated only in the state of Texas, this bank is known for its award-winning customer service for an Auto Loan Refinance.

- Cons: Residents outside of Texas cannot apply here.

69. First Horizon Bank

- Score / Amount: 650+ / $5,000 to $100,000

- Pros: Funds very quickly and the process to close the Auto Loan Refinance is smooth.

- Cons: Interest rates (APRs) are higher compared to credit unions.

70. Zions Bank

- Score / Amount: 660+ / $5,000 to $100,000

- Pros: A major lender in Utah and Idaho. Offers very low interest rates to those with good credit seeking an Auto Loan Refinance.

- Cons: A hard credit inquiry is required, and membership is in a limited area.

71. State Employees’ Credit Union (SECU)

- Score / Amount: 600+ / No set limit

- Pros: The second-largest credit union in the US. Its rates are among the cheapest in the Auto Loan Refinance market.

- Cons: Reserved only for North Carolina state employees and their families.

72. SchoolsFirst FCU

- Score / Amount: 620+ / According to vehicle value

- Pros: Provides some of the best Auto Loan Refinance rates in the US for teachers and school employees.

- Cons: Available only to California school employees and their families.

73. America First Credit Union (AFCU)

- Score / Amount: 600+ / $5,000+

- Pros: 100% online application and an option for long terms up to 84 months for an Auto Loan Refinance.

- Cons: Limited to residents of Utah, Nevada, Arizona, and Idaho.

74. VyStar Credit Union

- Score / Amount: 600+ / $5,000+

- Pros: An excellent Auto Loan Refinance lender for Florida and Georgia residents with no origination fees.

- Cons: Unavailable for other US states.

75. Randolph-Brooks FCU (RBFCU)

- Score / Amount: 620+ / $5,000+

- Pros: One of the fastest-growing credit unions in Texas; online approval for an Auto Loan Refinance is very fast.

- Cons: It is very difficult to obtain membership outside specific Texas counties.

76. Global Credit Union (formerly Alaska USA)

- Score / Amount: 600+ / $5,000 to $100,000

- Pros: Has a very strong network in Alaska, Washington, and the West Coast of the US for an Auto Loan Refinance.

- Cons: Interest rates become very high on long-term (84 months) loans.

77. Delta Community Credit Union

- Score / Amount: 640+ / $5,000+

- Pros: Transparent loans with no hidden fees for Georgia state residents and Delta Airlines employees.

- Cons: A hard credit check is mandatory.

78. SDCCU (San Diego County Credit Union)

- Score / Amount: 620+ / $5,000+

- Pros: Very popular for low-rate refinancing in Southern California.

- Cons: No services for people outside of California.

79. Kinecta Federal Credit Union

- Score / Amount: 620+ / $5,000+

- Pros: Allows refinancing up to 130% LTV (Loan-to-Value) (meaning it is possible to refinance even if the remaining debt is more than the car’s value).

- Cons: Requires a $10 fee for membership.

80. Lake Michigan Credit Union (LMCU)

- Score / Amount: 640+ / $5,000+

- Pros: Famous for its “Guaranteed Low Rate” in Michigan and Florida.

- Cons: May refuse to refinance older cars (more than 10 years old).

81. Tinker Federal Credit Union

- Score / Amount: 600+ / $2,500+

- Pros: The largest in the state of Oklahoma. Its minimum loan limit is only $2,500.

- Cons: Access is limited outside of Oklahoma.

82. Bellco Credit Union

- Score / Amount: 620+ / $5,000+

- Pros: Excellent rates and no application fees for Colorado residents.

- Cons: Does not accept applicants from outside Colorado.

83. Wright-Patt Credit Union

- Score / Amount: 600+ / $5,000+

- Pros: Flexible loan options for military and civilians in Ohio.

- Cons: Hard credit checks and regional limitations apply.

84. Patelco Credit Union

- Score / Amount: 640+ / $5,000+

- Pros: Excellent customer service in Northern California and a 90-day deferment on the first installment.

- Cons: Strict vehicle mileage limits.

85. Logix Federal Credit Union

- Score / Amount: 650+ / $5,000+

- Pros: 100% paperless (digital) process and extremely low rates for those with good credit.

- Cons: No options for those with low credit (below 600).

86. Credit Acceptance

- Score / Amount: No minimum / Depends on the dealer

- Pros: Accepts customers with past bankruptcies and vehicle repossessions.

- Cons: Interest rates are excessive (often 25%+) and carry heavy fees.

87. Global Lending Services (GLS)

- Score / Amount: 450+ / $5,000 to $50,000

- Pros: Helps refinance those who have been rejected by traditional banks.

- Cons: Charges heavy origination fees on the loan.

88. Flagship Credit Acceptance

- Score / Amount: 500+ / $7,500 to $50,000

- Pros: Gives bad credit holders a chance to refinance through its partner network.

- Cons: Customer service ratings are quite low, and interest rates are much higher than the market average.

89. Exeter Finance

- Score / Amount: No minimum / $5,000+

- Pros: One of the biggest names in the subprime market; the approval rate is very high.

- Cons: Its interest rates and terms prove to be very expensive for the borrower.

90. United Auto Credit

- Score / Amount: No minimum / $3,000+

- Pros: Grants loans based on income, not based on credit scores.

- Cons: Works only through its dealer network; direct online application is difficult.

91. Consumer Portfolio Services (CPS)

- Score / Amount: No minimum / $5,000+

- Pros: Acts as a last resort for those with extremely poor credit profiles.

- Cons: Refinancing for a long term might result in paying more in interest than the car’s value.

92. Skopos Financial

- Score / Amount: 500+ / $5,000+

- Pros: Approves subprime loans quickly using AI.

- Cons: Not licensed in all US states.

93. Bankrate Marketplace

- Score / Amount: 550+ / $5,000 to $100,000

- Pros: A highly reliable financial website that shows rates from dozens of authentic lenders simultaneously.

- Cons: It is an aggregator; you will face marketing calls.

94. MoneyLion

- Score / Amount: 600+ / Depends on the partner

- Pros: A fintech app that finds pre-qualified offers using your existing financial data.

- Cons: It is not a lender itself, so final loan terms may change.

95. Credit.com

- Score / Amount: 550+ / $5,000+

- Pros: Provides accurate matching based on your credit profile (Experian data).

- Cons: A lot of junk emails may come from the partner network.

96. Blueharbor Automotive

- Score / Amount: 600+ / $10,000 to $100,000

- Pros: A full-service broker that handles all the payoff work from the old bank itself.

- Cons: It has its own brokerage fee that is added to the loan.

97. eAutoloan

- Score / Amount: 500+ / $5,000 to $50,000

- Pros: A lead-generation network specifically designed for bad credit.

- Cons: A website with a very outdated interface, and the quality of lenders is mixed.

98. Prosper (Peer-to-Peer)

- Score / Amount: 640+ / $2,000 to $50,000

- Pros: This is not a bank but ‘peer-to-peer’ (P2P) lending. It can be used as a personal loan to pay off vehicle debt.

- Cons: Charges an origination fee of 1% to 5%.

99. LendingPoint

- Score / Amount: 600+ / $2,000 to $36,500

- Pros: Funding within 24 hours. Often used by people to rapidly refinance their expensive car loans (via a personal loan).

- Cons: The maximum loan limit is only $36,500.

100. CarGurus Finance

- Score / Amount: 600+ / $5,000 to $100,000+

- Pros: Originally a car buying platform, but its massive lender network (with Capital One, Global Lending, etc.) also helps find excellent refinancing rates.

- Cons: Acts as a broker channel, not a direct lender.

101. Regions Bank

- Score / Amount: 650+ / $5,000 to $100,000

- Pros: It has a very large network in the Southern US. This bank does not charge any origination fee on an Auto Loan Refinance.

- Cons: Its services are limited to the 15-16 US states where it has physical branches.

102. First National Bank of Omaha (FNBO)

- Score / Amount: 660+ / $5,000 to $75,000

- Pros: If you already have an account with them, it lowers the interest rate as a relationship discount for your Auto Loan Refinance.

- Cons: Its main focus is on the Midwest states, and the maximum loan limit is $75,000.

103. Associated Bank

- Score / Amount: 650+ / $5,000 to $100,000

- Pros: Strong presence in Wisconsin and Illinois. Its rates for an Auto Loan Refinance are highly competitive.

- Cons: A hard credit check occurs as soon as you apply to check rates.

104. SouthState Bank

- Score / Amount: 660+ / $5,000 to $100,000

- Pros: Excellent customer service and local banking experience in the Southeast US.

- Cons: A 100% online pre-qualification (soft check) facility is not available for an Auto Loan Refinance.

105. Arvest Bank

- Score / Amount: 650+ / $5,000 and above

- Pros: Offers Auto Loan Refinance options up to 72 months and no pre-payment penalty.

- Cons: You often have to visit their physical branch for the best service and rates.

106. First Hawaiian Bank

- Score / Amount: 640+ / Starting from $5,000

- Pros: The best and most reliable Auto Loan Refinance option for residents of the state of Hawaii.

- Cons: It does not offer its services in mainland USA states.

107. Umpqua Bank

- Score / Amount: 660+ / $5,000 to $100,000

- Pros: Very popular on the West Coast, and there are no hidden fees in their Auto Loan Refinance process.

- Cons: Its rules regarding the vehicle’s age and mileage are quite strict.

108. Webster Bank

- Score / Amount: 650+ / $5,000 and above

- Pros: Focused in the Northeast US, this bank gives special discounts to account holders.

- Cons: Geographically limited and the online interface is a bit outdated for an Auto Loan Refinance.

109. Busey Bank

- Score / Amount: 660+ / $5,000 and above

- Pros: This bank is known for its highly personalized customer service.

- Cons: Its network of physical branches is very small for handling an Auto Loan Refinance.

110. Rockland Trust

- Score / Amount: 650+ / $5,000 and above

- Pros: Famous for transparent Auto Loan Refinance rates in the Massachusetts area.

- Cons: It is a completely localized bank.

111. Wintrust Financial

- Score / Amount: 650+ / $5,000 and above

- Pros: Very strong presence in Chicago and surrounding areas.

- Cons: High reliance on branches; the digital experience is limited.

112. Pinnacle Financial Partners

- Score / Amount: 680+ / $5,000 to $100,000

- Pros: High-end customer service and a premium banking experience.

- Cons: Prioritizes only those with an excellent credit score for an Auto Loan Refinance.

113. WaFd Bank (Washington Federal Bank)

- Score / Amount: 650+ / $5,000 and above

- Pros: Active in 8 Western US states and provides loan options up to 84 months.

- Cons: Visiting a branch sometimes becomes mandatory for loan approval.

114. Valley National Bank

- Score / Amount: 660+ / $5,000 and above

- Pros: Very active and reliable in New York, New Jersey, and Florida.

- Cons: Digital loan management tools are very basic.

115. Old National Bank

- Score / Amount: 650+ / $5,000 and above

- Pros: A large bank in the Midwest that emphasizes relationship banking.

- Cons: If you do not have an account with them, the standard APRs for an Auto Loan Refinance can be quite high.

116. Renasant Bank

- Score / Amount: 640+ / $5,000 and above

- Pros: Easy process in the Southeast US.

- Cons: Their methods for evaluating car valuation are quite strict.

117. Trustmark

- Score / Amount: 650+ / $5,000 and above

- Pros: Excellent services with flexible terms in the Southern US.

- Cons: Their underwriting process is manual, so approval for an Auto Loan Refinance may take time.

118. Simmons Bank

- Score / Amount: 650+ / $5,000 and above

- Pros: Straightforward and transparent terms in the Mid-South region.

- Cons: No pre-qualification facility; a direct hard credit check occurs.

119. Bank of Hawaii

- Score / Amount: 640+ / $5,000 and above

- Pros: Excellent interest rates for local residents in the state of Hawaii.

- Cons: Unavailable for the 49 states of the US mainland.

120. First Interstate Bank

- Score / Amount: 650+ / $5,000 and above

- Pros: Covers 14 states in the Western and Midwestern US.

- Cons: The online interface and mobile app experience is average.

121. GreenState Credit Union

- Score / Amount: 600+ / $5,000 and above

- Pros: It is the largest credit union in Iowa, but it provides loans nationwide through a partner network.

- Cons: You must become a member to get a loan.

122. ESL Federal Credit Union

- Score / Amount: 620+ / $5,000 and above

- Pros: Concentrated in New York state; it pays excellent dividends to its members every year.

- Cons: It is limited to specific counties in New York.

123. Desert Financial Credit Union

- Score / Amount: 600+ / $5,000 and above

- Pros: The largest credit union in Arizona; excellent local rates.

- Cons: People outside of Arizona cannot become members.

124. Ent Credit Union

- Score / Amount: 620+ / $5,000 and above

- Pros: Has a large network in the state of Colorado and no application fees.

- Cons: Available only to residents of Colorado and Wyoming.

125. Idaho Central Credit Union (ICCU)

- Score / Amount: 600+ / $5,000 and above

- Pros: Massive presence in Idaho and Washington state.

- Cons: A hard credit check is mandatory, and the membership area is limited.

126. Redstone Federal Credit Union

- Score / Amount: 620+ / $5,000 and above

- Pros: Famous for very low APRs in Alabama and Tennessee.

- Cons: People from other states have to join special partner charities to become members.

127. Broadview FCU

- Score / Amount: 620+ / $5,000 and above

- Pros: A powerhouse in Upstate NY with community-driven policies.

- Cons: Its area of influence is only regional.

128. Addition Financial

- Score / Amount: 600+ / $5,000 and above

- Pros: Great for Central Florida residents and teachers; fast approval.

- Cons: It has no presence outside of Florida.

129. Affinity Federal Credit Union

- Score / Amount: 640+ / $5,000 and above

- Pros: The largest credit union in New Jersey. Anyone can become a nationwide member by donating to a foundation.

- Cons: The paperwork process for membership through donation can be a bit cumbersome.

130. Chevron Federal Credit Union

- Score / Amount: 650+ / $5,000 and above

- Pros: Below-market rates for Chevron employees and select groups.

- Cons: The membership base is very niche and limited.

131. CommunityAmerica Credit Union

- Score / Amount: 620+ / $5,000 and above

- Pros: Excellent digital banking tools in the Kansas City area.

- Cons: Membership is limited only to the Kansas City metro and surrounding areas.

132. BCU (Baxter Credit Union)

- Score / Amount: 640+ / $5,000 and above

- Pros: Excellent rates for employees of large corporate companies like Target and UnitedHealth.

- Cons: A hard credit inquiry is required for approval.

133. Canvas Credit Union

- Score / Amount: 600+ / $5,000 and above

- Pros: Focused on Colorado; it provides a 90-day payment deferral on the first installment after an Auto Loan Refinance.

- Cons: A small one-time fee is required for membership.

134. Chartway Federal Credit Union

- Score / Amount: 600+ / $5,000 and above

- Pros: Active in Virginia, Utah, and Texas; it shows flexibility for those with lower credit scores.

- Cons: If your credit score is low, the APR becomes quite expensive.

135. Elevations Credit Union

- Score / Amount: 640+ / $5,000 and above

- Pros: Great rates in Colorado and a completely community-driven institution.

- Cons: Nobody other than Colorado residents can get membership.

136. Everwise Credit Union (formerly Teachers CU)

- Score / Amount: 620+ / $5,000 and above

- Pros: The largest credit union in Indiana; special benefits for teachers.

- Cons: Available only in Indiana and parts of Michigan.

137. Grow Financial FCU

- Score / Amount: 620+ / $5,000 and above

- Pros: Active in Florida and South Carolina, a great option for military members.

- Cons: Loan processing paperwork can sometimes take longer.

138. PSECU (PA State Employees CU)

- Score / Amount: 640+ / $5,000 and above

- Pros: The largest in Pennsylvania; offers some of the lowest interest rates in the market.

- Cons: Available only to Pennsylvania residents and students.

139. Landmark Credit Union

- Score / Amount: 620+ / $5,000 and above

- Pros: The largest in Wisconsin; transparent and straightforward terms for an Auto Loan Refinance.

- Cons: Geographical boundaries are very strict.

140. MSUFCU (Michigan State Univ. FCU)

- Score / Amount: 600+ / $5,000 and above

- Pros: An excellent option for Michigan residents and university students/staff.

- Cons: Undergoing a hard credit check is mandatory for approval.

141. Mariner Finance

- Score / Amount: 550+ / $1,000 to $25,000

- Pros: People often use it by taking a personal loan to complete an Auto Loan Refinance on a small remaining car debt.

- Cons: It is a subprime lender, so its APRs are very high.

142. Regional Finance

- Score / Amount: 500+ / $2,500 to $25,000

- Pros: Accepts those with bad credit and has branches in 15 US states.

- Cons: The maximum loan limit is very low ($25,000) and interest rates are expensive.

143. Bridgecrest

- Score / Amount: No minimum / Depends on profile

- Pros: It is the financing arm of the famous US dealership DriveTime. It helps to restructure or complete an Auto Loan Refinance even for people with extremely poor credit.

- Cons: Due to high-risk loans, it charges some of the most expensive interest rates in the market.

144. CarFinance.com

- Score / Amount: 550+ / $7,500 to $50,000

- Pros: It is a 100% online lender that specifically focuses on those with below-average credit scores.

- Cons: Their customer service over the phone is often difficult to reach.

145. Oportun

- Score / Amount: No credit history needed / Up to $20,000

- Pros: It uses alternative data (like utility bills or rent payments) instead of credit scores for approval. Great for immigrants.

- Cons: The loan limit is very low and interest rates are among the highest in the fintech market.

146. RateWorks

- Score / Amount: 600+ / $10,000 to $75,000

- Pros: This company specifically works only on reducing your monthly installment or lowering your auto APR.

- Cons: It adds an origination fee (processing fee) to your new loan in some cases.

147. LoanCenter

- Score / Amount: 500+ / $5,000 and above

- Pros: It specializes in auto title loans and subprime refinancing.

- Cons: If you fail to pay installments (default), their repossession rules are very aggressive.

148. Autopayplus

- Score / Amount: 600+ / According to vehicle value

- Pros: It matches you with lenders and sets up a bi-weekly payment plan to pay off your loan quickly.

- Cons: It is not a direct lender, but rather a service that charges a membership/service fee for your loan management.

149. CNAC (Byrider Finance)

- Score / Amount: No minimum / Depends on the dealer

- Pros: It is a pure subprime (buy here, pay here) lender. If your loan is with Byrider, they sometimes do an internal Auto Loan Refinance to give you relief.

- Cons: It acts like a predatory lender where interest rates touch the state’s legal maximum limits.

150. Yendo

- Score / Amount: 500+ / Up to $10,000

- Pros: It is a brand new model. It is not a traditional refinance, but instead gives you a credit card based on your car’s equity (value), allowing you to manage your old loan.

- Cons: It is not a traditional auto installment loan, and credit card rates can exceed 20%+.

This data is completely based on the financial systems of the United States and the official policies of these companies for your Auto Loan Refinance research.

Choosing the Best Option for Your auto loan refinance in the USA

When analyzing a massive database of 150 lenders, marketplaces, and credit unions, it becomes clear that there is no single “best” company for every borrower. The ideal choice for an auto loan refinance depends entirely on your personal credit profile, financial goals, and vehicle type. The market can be effectively summarized into distinct categories to help you identify the right fit:

Top Credit Unions (Best for Lowest APRs)

Institutions like Navy Federal, PenFed, and BECU consistently offer the lowest interest rates in the industry. They are ideal for borrowers with good-to-excellent credit who do not mind opening a basic savings account to establish membership. They also offer great flexibility, with some refinancing loans as low as $250 to $500.

Major Traditional Banks (Best for Relationship Discounts)

Traditional direct lenders like Capital One, Bank of America, and Chase provide high stability, seamless digital management, and substantial relationship discounts (often 0.25% to 0.50% off the APR) if you already hold a checking or savings account with them. They generally prefer borrowers with credit scores above 640 and vehicles under 10 years old.

Online Marketplaces (Best for Comparing Rates)

Platforms such as AutoPay, RateGenius, and Caribou are excellent for borrowers who want to compare multiple offers simultaneously. Most of these platforms utilize a soft credit check for pre-qualification, allowing you to view potential rates without impacting your credit score. This is highly beneficial for finding competitive rates across a network of over 100 regional banks and credit unions.

Fintech & Subprime Lenders (Best for Bad Credit or Thin Credit)

If your credit score is below 580 or you have a history of bankruptcy, specialized subprime lenders like Santander Consumer USA, OneMain Financial, and Westlake Financial offer the highest approval rates. While their APRs are significantly higher due to the increased risk, they provide an opportunity to restructure your debt and rebuild your credit history.

Specialized Lenders (Best for Niche Vehicles)

For unconventional vehicles, specialized platforms are necessary. Companies like Tenet focus exclusively on electric vehicles (EVs) by factoring battery health and federal tax credits into the loan structure. Conversely, lenders like Woodside Credit and Truliant specialize in classic or collector cars, offering extended terms up to 15 years to minimize monthly payments.

In conclusion, the best strategy is to first utilize a marketplace or a direct lender that offers pre-qualification via a soft credit check. If you qualify for membership at a top credit union or have an existing relationship with a major bank, check their direct rates as well to ensure you secure the absolute lowest APR and the most favorable terms for your situation.

Frequently Asked Questions About auto loan refinance

1. What is the minimum credit score required for an auto loan refinance in the USA?

There is no universal minimum. Specialized subprime lenders and fintech platforms can approve applicants with credit scores as low as 500, or even those with no credit history. However, traditional banks and credit unions typically require a score of 620 to 650 to secure competitive interest rates.

2. How does a marketplace differ from a direct lender?

A direct lender (like a bank or credit union) funds the loan directly and manages your payments. An online marketplace is a broker platform that takes your information and matches you with multiple lending partners, allowing you to compare various offers in one place.

3. Will checking my eligibility drop my credit score?

If the lender or marketplace uses a “soft credit check” for pre-qualification, your credit score will not be affected. However, once you select an offer and submit a formal application to finalize the loan, the lender will perform a “hard credit check,” which can temporarily lower your score by a few points.

4. Can I complete an auto loan refinance if my current loan balance is very small?

Yes, but you must choose the right institution. While many marketplaces require a minimum loan amount of $7,500 to $10,000, certain credit unions like Navy Federal and PenFed allow you to refinance small remaining balances starting from $250 to $500.

5. What vehicle restrictions do lenders typically enforce?

Most traditional banks and credit unions require the vehicle to be less than 10 years old and have fewer than 100,000 to 125,000 miles. If your car is older, you will need to look for flexible credit unions or specialized classic car lenders.

6. Is it possible to get cash back during the refinancing process?

Yes. This is known as a cash-out refinance. If your car is worth significantly more than what you currently owe on your loan (positive equity), lenders like OpenRoad Lending allow you to borrow against that equity and receive the difference in cash.

7. Can I refinance my car loan if I am currently in a lease?

Yes, this process is called a lease buyout refinance. Marketplaces like MyAutoLoan and Innovative Funding Services (IFS) specialize in providing loans to pay off the leasing company so that you can transition into full ownership of the vehicle.

8. Do these companies charge an origination or processing fee?

It varies by provider. Most traditional direct lenders like Chase and U.S. Bank charge zero origination fees. However, full-service online marketplaces and brokers often charge a processing fee ranging from $399 to $499, which is typically rolled into the total balance of your new loan.

9. Can I add a co-signer to secure a better interest rate?

Yes, many fintech platforms and marketplaces (such as RefiJet and iLending) allow you to add a co-signer or co-applicant. This is highly beneficial for borrowers with low credit scores, as it leverages the co-signer’s stronger credit history to obtain lower APRs.

10. What insurance requirements must be met to close the loan?

Almost all lenders require you to carry “full coverage” auto insurance (comprehensive and collision) for the entire duration of the loan. When shifting your loan to a new provider, you must update your insurance policy to list the new lender as the loss payee.