Auto Loan : How to Get the Lowest Rate Today in the USA

Current Auto Loan Rates: A Market Analysis

Navigating the US auto loan market can be challenging, especially as it has witnessed continuous fluctuations recently. Whether you are planning to finance a brand-new ride or looking for a reliable pre-owned car, understanding current auto loan interest rates is crucial for your financial planning.

Due to recent Federal Reserve policies and shifting economic conditions, auto loan interest rates (APR) have decreased slightly from their previous highest levels. However, they still remain at historically high levels, making it essential to research and compare your options carefully before visiting a dealership.

Average Auto Loan Rates by Vehicle Type

When applying for an auto loan, the Annual Percentage Rate (APR) you receive heavily depends on whether you are buying a new or used vehicle. Lenders generally offer lower interest rates for new cars because they are easier to value and carry less risk.

Here is a breakdown of the current 60-month average APR for a standard auto loan:

| Car Type | 60-Month Average APR |

| New Vehicles | ~7.04% |

| Used Vehicles | Above ~10.60% |

Why Are Auto Loan Rates Fluctuating?

The primary driver behind the current auto loan landscape is the broader economic environment. The Federal Reserve’s monetary policies directly influence how much it costs financial institutions to borrow money. When rates are adjusted to balance the economy, lenders pass those costs directly onto consumers.

While we have seen a slight dip from the peak levels recently, the cost of securing an auto loan remains elevated compared to past historical norms. This makes lender comparison more important than ever.

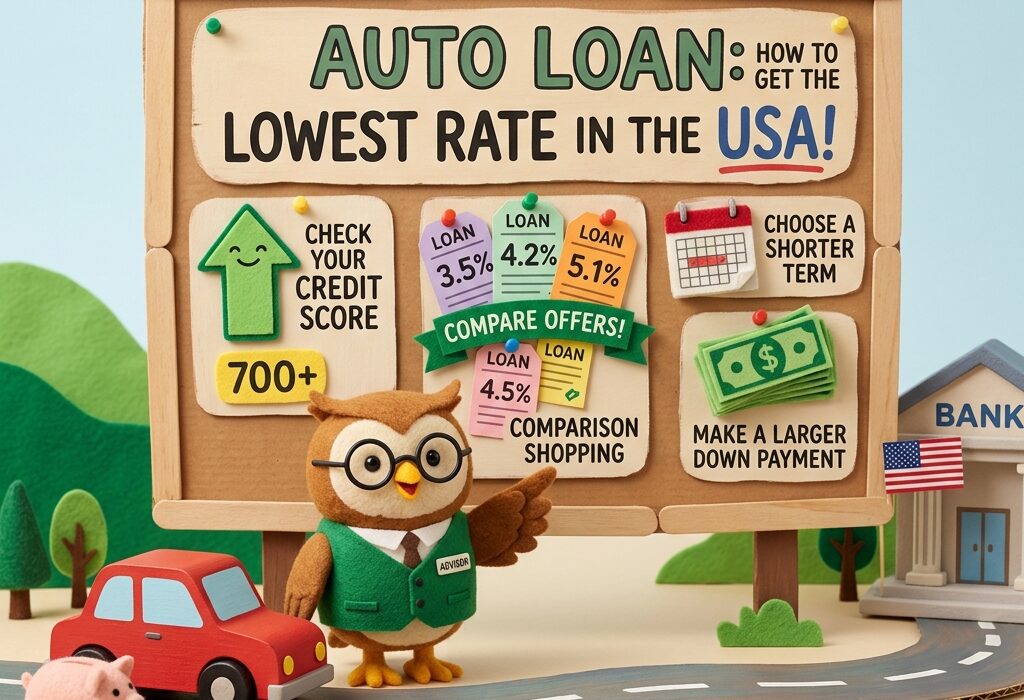

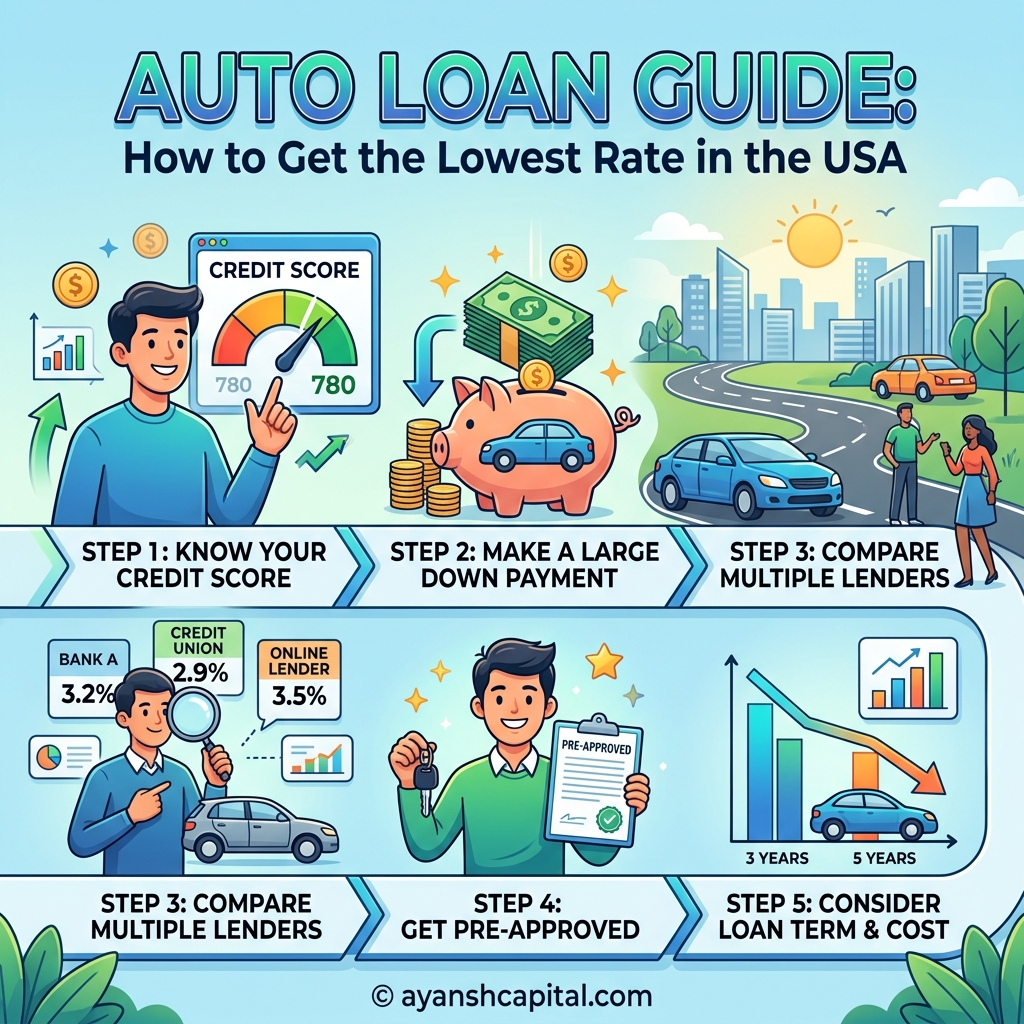

Tips for Securing the Best Auto Loan

If you are looking to secure the most favorable auto loan in today’s market, consider the following strategies:

- Check Your Credit Score: A higher credit score is the single most effective way to secure a lower APR on your auto loan. Check your report for errors before applying.

- Shop Around: Don’t just accept the dealer’s financing offer. Compare auto loan terms from traditional banks, local credit unions, and online lenders.

- Consider a Shorter Term: While a 60-month term is standard, choosing a 36-month or 48-month auto loan can significantly lower your interest rate and the total interest paid over the life of the vehicle.

- Make a Larger Down Payment: Putting more money down reduces the total amount of your auto loan, which decreases the lender’s risk and can help you negotiate better terms.

Conclusion

While finding an affordable auto loan currently requires navigating historically high interest rates, being well-informed gives you a distinct advantage. By understanding the market averages—around 7.04% for new vehicles and over 10.60% for used ones—you can set realistic expectations, plan your budget accurately, and negotiate the best possible auto loan for your next vehicle purchase.

The Impact of Credit Scores on Interest Rates

In the world of auto loans, your credit score (FICO Score) is your most powerful weapon. It ultimately determines exactly how much extra money you will end up paying to the lender over the life of your loan. According to Current data, interest rates vary significantly depending on where you fall within the different credit tiers.

Here is a detailed breakdown of how your credit score dictates your auto loan rates:

Note: The Super Prime category is considered the safest tier by lenders, rewarding borrowers with fantastic, market-leading rates. On the other hand, Deep Subprime borrowers face a massive interest burden.

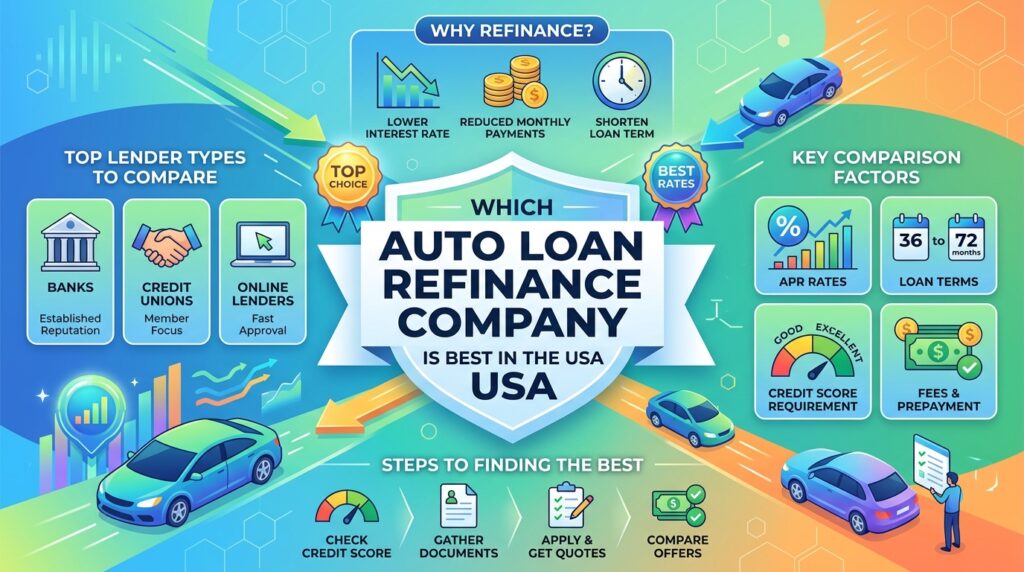

Banks vs. Credit Unions (For Excellent Credit Scores)

If your credit score is 780 or above (Excellent Credit), you possess the leverage to secure the absolute lowest auto loan rates available in the market. When deciding where to get your vehicle financed, the choice usually comes down to Credit Unions versus Traditional Banks.

Here is how the Current data compares for top-tier borrowers:

- Credit Unions: Institutions like PenFed or Navy Federal operate as non-profit organizations. Because of this structure, they generally offer better terms to their members. In Current , credit unions are offering average rates of around 5.75% for a 60-month new car loan. With certain special conditions, institutions like PenFed are offering rates as low as 3.39%. For used cars, the average rate for a 48-month term sits around 5.82%.

- Traditional Banks: Major traditional banks, such as Bank of America or Chase, usually offer slightly higher auto loan rates compared to credit unions. For an excellent credit borrower, the average rate for a 60-month new car loan is approximately 7.49% (though lenders like Bank of America have a starting rate of 5.44%). For a used car loan, you can expect an average rate of about 7.79%.

Quick Comparison: Traditional Banks vs. Credit Unions

Top 25 Auto Loan Companies in the USA:

Selecting the most suitable auto loan requires a thorough evaluation of the lending landscape. In the US market, finding the right auto loan provider depends heavily on your credit profile, target vehicle, and debt structure. Below is an in-depth analysis of the top 25 financing companies and marketplaces to secure an auto loan, detailing their core features alongside their positive and negative impacts.

1. Bank of America

Bank of America features an attractive auto loan product for borrowers who prefer a large, established financial institution, particularly those with pre-existing checking or savings accounts.

- Starting APR: Approximately 5.44% for new cars and 5.64% for used cars.

- Loan Amount: Starts at a minimum of $7,500.

- Specialty: Members of the Preferred Rewards Program can qualify for an interest rate reduction of 0.25% to 0.50% on a new auto loan. Rates can be locked online for up to 30 days.

- Positive Impacts (Pros): Offers significant relationship discounts for loyal bank customers and a helpful 30-day rate lock feature.

- Negative Impacts (Cons): Borrowers are restricted to buying vehicles from a specific authorized dealer network, and older, high-mileage cars face strict exclusions.

2. PenFed Credit Union (Pentagon Federal Credit Union)

Credit unions consistently deliver lower rates than national corporate banks, and PenFed remains an industry leader for securing a low-interest auto loan.

- Starting APR: Starts around 4.19% for competitive short-term financing.

- Loan Amount: Funding available up to $150,000.

- Specialty: Ideal for tier-one borrowers with excellent credit histories. It provides competitive pricing on late-model vehicles with low mileage.

- Positive Impacts (Pros): Delivers highly competitive interest rates and provides financing for up to 125% of the vehicle’s retail value.

- Negative Impacts (Cons): Borrowers must establish credit union membership to finalize their auto loan, and the lowest advertised rates require shorter terms.

3. Capital One Auto Finance

Capital One offers a modern, digital-first financing environment for car buyers who want to view their financing terms clearly prior to shopping.

- Minimum Income: Approximately $1,500 to $1,800 per month.

- Minimum Loan Amount: $4,000.

- Specialty: The proprietary Auto Navigator tool allows buyers to pre-qualify for an auto loan with a soft credit pull, keeping their credit score safe.

- Positive Impacts (Pros): Highly transparent pre-qualification process and a low minimum financing threshold of $4,000.

- Negative Impacts (Cons): Exact loan terms are finalized only at a participating physical dealership, and financing is unavailable in Alaska and Hawaii.

4. U.S. Bank

U.S. Bank is an outstanding choice for consumers looking to purchase a pre-owned vehicle directly from an individual owner.

- Starting APR: Close to the standard national market average (~6.50%).

- Term Limits: Repayment terms extend up to 72 months.

- Specialty: While many traditional banks avoid private party lending, U.S. Bank provides clear peer-to-peer financing for an auto loan.

- Positive Impacts (Pros): Excellent streamlined framework for private seller transactions and accessible customer support.

- Negative Impacts (Cons): Enforces rigid age and mileage restrictions on used inventory, and does not offer online soft-pull pre-qualification.

5. Navy Federal Credit Union

As the largest credit union in the United States, Navy Federal is a premier choice for military personnel, veterans, and their immediate families seeking an auto loan.

- Starting APR: Highly competitive baseline rates starting around 4.09%.

- Term Limits: Extended repayment timelines up to 96 months are available.

- Specialty: Provides exceptional financing flexibility for both factory-new and late-model pre-owned vehicles.

- Positive Impacts (Pros): Extended repayment horizons to reduce monthly obligations, low baseline APRs, and zero hidden origination fees.

- Negative Impacts (Cons): Membership eligibility is strictly restricted to the military community, and the online tracking interface can feel slow.

6. LightStream

For consumers possessing excellent credit scores (750+), LightStream provides an entirely unique and unrestricted borrowing experience.

- Starting APR: Roughly 5.99% when enrolled in their automated payment program.

- Loan Amount: Funding parameters reach up to $100,000.

- Specialty: Operates by delivering an unsecured personal loan rather than a traditional, collateral-backed auto loan. The bank deposits cash directly into your account.

- Positive Impacts (Pros): No restrictions on the vehicle’s manufacturing year, make, or mileage, giving you the leverage of a cash buyer.

- Negative Impacts (Cons): Underwriting standards are incredibly high, completely shutting out subprime applicants.

7. Chase Auto

Chase Auto provides a highly integrated, frictionless financing path for consumers who already utilize the broader Chase banking ecosystem.

- Starting APR: Very competitive tiered pricing specifically for current account holders.

- Specialty: Fully integrated management of your auto loan within the native Chase mobile banking application.

- Positive Impacts (Pros): Superb digital management features and access to a massive national network of partner dealerships.

- Negative Impacts (Cons): Does not offer private party financing options, and baseline rates rarely beat non-profit credit unions.

8. Consumers Credit Union (CCU)

For those unable to satisfy the military constraints of other credit unions, CCU provides an accessible, open-membership alternative to fund an auto loan.

- Starting APR: Base rates begin near 5.24%.

- Specialty: Open membership available to the general public via a simple, one-time $5 historical donation.

- Positive Impacts (Pros): Frictionless onboarding process, competitive interest rates, and lucrative options to refinance a car.

- Negative Impacts (Cons): Interest rates climb drastically for older used cars, and physical branching is concentrated entirely in Illinois.

9. Ally Bank

Ally Bank operates as a digital-only lender that specializes in accommodating a wide variety of diverse credit profiles through dealership partnerships.

- Starting APR: Highly variable based on the dealer network and consumer credit file.

- Specialty: An established leader in indirect digital lending markets.

- Positive Impacts (Pros): Highly accommodating for applicants with average credit scores, supported by 24/7 client services.

- Negative Impacts (Cons): Consumers cannot apply for a direct auto loan on the website; they must visit an authorized partner dealership.

10. PNC Bank

PNC Bank provides a structured financing option called the ‘Check Ready’ program, empowering consumers during the high-pressure sales process.

- Starting APR: hovers near 6.00% for well-qualified applicants.

- Loan Amount: Caps out at $75,000.

- Specialty: Upon approval, PNC issues a physical blank check up to a pre-approved amount, allowing you to pay the exact out-the-door price.

- Positive Impacts (Pros): The physical check grants the immediate negotiating power of a cash buyer, and current account holders receive rate discounts.

- Negative Impacts (Cons): Lacks an online soft-pull pre-qualification mechanism, and standard rates sit slightly above credit union baselines.

11. USAA

USAA is a top-tier financial institution focused on providing auto insurance and vehicle financing exclusively to the military community.

- Starting APR: Baseline financing starts around 5.49%.

- Specialty: Offers noticeable rate deductions for buyers utilizing their automated payment platform.

- Positive Impacts (Pros): Highly praised customer satisfaction metrics and a completely digitized, hassle-free lending process.

- Negative Impacts (Cons): Membership is strictly limited to military personnel, veterans, and their dependents.

12. Truist

Formed via the large-scale merger of SunTrust and BB&T, Truist operates as a highly modern bank known for rapid liquidity.

- Starting APR: Standard market tiers averaging around 6.24%.

- Loan Amount: Minimum borrowing tier starts at $5,000.

- Specialty: Exceptional focus on rapid funding turnaround times for an approved auto loan.

- Positive Impacts (Pros): Imposes zero structural loan origination fees and features a quick online processing interface.

- Negative Impacts (Cons): The lowest interest rates require a pre-existing relationship, and credit profiles below 680 face higher rates.

13. Alliant Credit Union

For buyers intent on purchasing a hybrid or fully electric vehicle (EV), Alliant stands out as an exceptionally focused lender.

- Starting APR: Tiers begin near 5.75% for modern eco-friendly inventory.

- Specialty: Features distinct “green” interest rate deductions for sustainable transportation choices.

- Positive Impacts (Pros): Fantastic financing rates for Tesla and competitive EV models, with same-day loan closing possibilities.

- Negative Impacts (Cons): Standard credit union onboarding criteria apply, and terms for aging, used internal-combustion vehicles are limited.

14. TD Bank

TD Bank caters effectively to East Coast car buyers, offering extended financing structures to manage payment size.

- Starting APR: Tiers sit around 6.74%.

- Term Limits: Extended repayment horizons up to 84 months are available.

- Specialty: Focuses heavily on helping consumers lower their monthly obligations via longer lending timelines.

- Positive Impacts (Pros): Long loan terms up to 84 months and the rare convenience of physical branches operating on weekends.

- Negative Impacts (Cons): Funding is restricted geographically to specific states, and an 84-month timeline increases the total interest paid over time.

15. AutoPay

AutoPay operates as a highly useful online lending marketplace focused on helping consumers find a lower rate through refinancing.

- Starting APR: Tiers start near 4.99% based on their vast lender network.

- Specialty: Generates a high volume of competing offers from a single digital application.

- Positive Impacts (Pros): Excellent platform for rate comparison and an incredibly straightforward mechanism to lower existing debt costs.

- Negative Impacts (Cons): Certain niche lending partners in the marketplace may charge separate administrative fees.

16. Digital Federal Credit Union (DCU)

DCU is nationwide credit union widely recognized for offering some of the lowest interest rates on a consumer auto loan.

- Starting APR: Highly competitive base rates starting near 4.49%.

- Specialty: Offers an additional 0.25% discount for energy-efficient vehicles.

- Positive Impacts (Pros): Consistently beats traditional bank rates and features an easy membership path through minor association donations.

- Negative Impacts (Cons): Achieving the absolute lowest advertised APR requires setting up direct deposit into a DCU checking account.

17. Wells Fargo Auto

Wells Fargo manages a massive indirect lending footprint, providing an auto loan option through a vast network of dealerships nationwide.

- Starting APR: Varies dynamically based on dealership negotiation and credit score.

- Specialty: Deeply integrated into thousands of franchise dealership financing offices across the country.

- Positive Impacts (Pros): Extremely high availability at the point of sale and substantial relationship lending options.

- Negative Impacts (Cons): Individual consumers cannot apply for a direct pre-approval on the website; everything must go through a dealer.

18. Citizens Bank

Citizens Bank offers flexible financing solutions for individuals searching for factory-new or certified pre-owned vehicles.

- Starting APR: Baseline tiers sit near 6.49%.

- Loan Amount: Minimum financing starts at $5,000.

- Positive Impacts (Pros): Transparent rate structures and solid payment discount options when using automated electronic payments.

- Negative Impacts (Cons): Primarily serves borrowers located within their specific regional footprint, and requires higher credit scores for top rates.

19. LendingTree

LendingTree functions as an expansive financial marketplace, allowing users to shop for an auto loan across hundreds of competing lenders simultaneously.

- Starting APR: Highly variable depending on the specific lender matched to your profile.

- Specialty: Multi-lender match engine that introduces transparent competition to secure your business.

- Positive Impacts (Pros): Maximizes your chances of finding a specialized lender regardless of your credit score tier.

- Negative Impacts (Cons): Submitting your information can result in an influx of marketing calls and automated emails from various financial institutions.

20. MyAutoloan

MyAutoloan is an efficient online comparison engine that delivers multiple customized auto loan certificates within minutes of applying.

- Minimum Credit Score: 575.

- Specialty: Fast processing speeds that return up to four direct offers for pre-purchase, private party, or refinancing needs.

- Positive Impacts (Pros): Transparent side-by-side comparison matrix and subprime-friendly matching parameters.

- Negative Impacts (Cons): Requires a minimum monthly income of $1,500 to qualify for the marketplace comparison engine.

21. Carvana

Carvana integrates an internal auto loan financing mechanism directly into its nationwide online vehicle purchase platform.

- Minimum Credit Score: No structural minimum credit score requirement.

- Specialty: Seamless digital checkout that includes vehicle picking, delivery scheduling, and loan signing.

- Positive Impacts (Pros): Transparent terms with soft credit pulls and highly accessible financing for thin credit profiles.

- Negative Impacts (Cons): The interest rates provided are typically higher than those you could secure independently from an outside credit union.

22. OpenRoad Lending

OpenRoad Lending specializes explicitly in helping consumers optimize their current financial situation through an auto loan refinance program.

- Minimum Credit Score: 560.

- Specialty: Focused heavily on dropping monthly payments for subprime borrowers locked into expensive dealer contracts.

- Positive Impacts (Pros): High approval ratios for borrowers with less-than-perfect credit and a streamlined digital loan swap process.

- Negative Impacts (Cons): Does not offer financing for original vehicle purchases; handles refinancing exclusively.

23. RefiJet

RefiJet provides a highly personalized, white-glove marketplace approach to restructuring your current auto debt.

- Minimum Credit Score: 500.

- Specialty: Assigns a dedicated loan specialist to guide you through replacing your current high-APR contract.

- Positive Impacts (Pros): Highly supportive customer care team and flexible options to change loan terms or remove co-signers.

- Negative Impacts (Cons): Imposes a documentation processing fee that is rolled into the principal of the new contract.

24. Santander Consumer USA (RoadLoans)

Santander Consumer USA, operating its direct-to-consumer division via RoadLoans, is an established giant in subprime vehicle financing.

- Minimum Credit Score: Highly flexible with no firm baseline.

- Specialty: Delivering auto financing to consumers recovering from deep credit issues or past bankruptcies.

- Positive Impacts (Pros): Exceptional approval rates for high-risk credit tiers and straightforward online voucher delivery.

- Negative Impacts (Cons): The Annual Percentage Rates (APR) issued carry a significant subprime premium, increasing total loan costs.

25. Westlake Financial

Westlake Financial works directly with an extensive network of independent and franchise dealers to provide flexible lending options.

- Minimum Credit Score: No baseline requirement.

- Specialty: Providing automated, instant lending decisions for buyers who have been rejected by traditional institutions.

- Positive Impacts (Pros): Highly advanced risk-modeling that accepts almost all credit profiles and supports credit building.

- Negative Impacts (Cons): Demands a higher down payment from subprime buyers and attaches elevated interest rates to low-tier scores.

Top 20 Auto Loan Companies for Bad Credit in the USA

1. MyAutoloan

- Minimum Credit Score: 575

- Conclusion: This is a highly popular online marketplace. By filling out just one secure form, you can receive auto loan offers from four different subprime lenders in a matter of minutes. This platform allows you to clearly compare different interest rates without damaging your credit score, which is incredibly useful before physically visiting a dealership.

2. Carvana

- Minimum Credit Score: No fixed limit (Minimum income of $4,000 per year).

- Conclusion: This platform takes the entire car buying and financing process 100% online. Its biggest feature is that it provides a precise EMI and interest rate using a “soft credit check.” It is an excellent option for customers who want an auto loan without the hesitation or anxiety of haggling with dealership salesmen.

3. Credit Acceptance

- Minimum Credit Score: No minimum (Deep Subprime).

- Conclusion: This company is a fantastic alternative for individuals who have extremely poor credit or have recently declared bankruptcy. To approve your auto loan, they rely heavily on your current income and job stability rather than focusing on your damaged past credit history. However, be prepared to encounter considerably higher interest rates on a subprime auto loan.

4. Capital One Auto Finance

- Minimum Credit Score: Flexible rules (No strict minimum).

- Conclusion: Among large traditional banks, Capital One is the most generous and flexible toward subprime customers. Their highly popular “Auto Navigator” tool allows you to pre-qualify for an auto loan from the comfort of your home before ever visiting the dealership. Furthermore, their authorized dealer network is massive across the USA.

5. DriveTime

- Minimum Credit Score: No minimum (Approximately 99% approval rate).

- Conclusion: This is one of the largest companies operating on the “Buy Here, Pay Here” (in-house financing) model. They sell the cars themselves and provide the auto loan themselves. If your application has been rejected everywhere else, there is a very high probability of getting approved here.

6. Auto Credit Express

- Minimum Income Requirement: $1,500 per month.

- Conclusion: This is not a direct lender but a highly effective matchmaking service. It connects people who have faced bad credit, bankruptcy, or car repossession directly to local “special finance dealerships” willing to provide an auto loan. It is perfect for buyers who need personalized, local-level assistance.

7. CarMax

- Minimum Credit Score: No minimum.

- Conclusion: Similar to Carvana, CarMax is a massive retailer of used cars offering no-haggle pricing. They operate their own in-house financing department and simultaneously collaborate with multiple subprime companies to safely secure your auto loan. The financing process here is known for being extremely transparent and reliable.

8. Car.Loan.com

- Minimum Credit Score: None (No Credit / Bad Credit).

- Conclusion: This specific platform targets first-time car buyers who lack a credit history, as well as individuals with severely bad credit. It seamlessly connects you to a network of dealerships that specialize entirely in providing an auto loan to high-risk customers.

9. Santander Consumer USA (RoadLoans)

- Minimum Credit Score: Very flexible.

- Conclusion: This is one of the largest and most well-known subprime lenders in America. They provide direct financing to consumers (under the RoadLoans brand) as well as indirectly through dealerships. While they readily approve an auto loan for very low credit scores, their exact interest rates can be somewhat strict.

10. Westlake Financial

- Minimum Credit Score: None.

- Conclusion: Westlake is famous for utilizing its extensive dealer network to finance almost every type of credit profile, whether it is bad, zero, or involves a recent bankruptcy. Their highly advanced technology helps dealers secure instant auto loan approvals for their customers on the spot.

11. Prestige Financial

- Minimum Credit Score: None (Minimum income is usually $2,250 per month).

- Conclusion: This company is a genuine blessing for individuals going through severe financial crises, such as a Chapter 7 or Chapter 13 bankruptcy. While other financial institutions instantly reject applications that merely mention bankruptcy, Prestige easily provides an auto loan to such recovering customers.

12. Upstart

- Minimum Credit Score: Approximately 510.

- Conclusion: Upstart is a highly modern, AI-based platform. Instead of relying purely on a traditional credit score, it deeply analyzes your education, college degree, and overall employment history to properly grant an auto loan. It is a superb option for young professionals or individuals with a “thin file” (minimal credit history).

13. Byrider

- Minimum Credit Score: No minimum.

- Conclusion: This is a massive “Buy Here, Pay Here” franchise network that lends money directly from the dealership. Their unique selling point is that they often include on-site service and warranties alongside their used vehicles. It is geared towards buyers with low down payments who cannot physically secure an auto loan anywhere else.

14. LendingTree

- Minimum Credit Score: Varies (Depending heavily on different lenders).

- Conclusion: This is one of the largest online financial marketplaces in the United States. Once you securely enter your details, it matches subprime customers with multiple lenders perfectly suited to their specific profiles. It serves as an excellent tool to clearly compare current subprime auto loan rates in the market.

15. OneMain Financial

- Minimum Credit Score: No strict minimum (Generally under 600 is widely acceptable).

- Conclusion: OneMain Financial is an excellent choice for individuals who prefer taking a secured loan by using a personal asset or car as collateral rather than seeking an unsecured option. They also successfully maintain physical branches all over the USA, allowing customers to have comfortable face-to-face meetings regarding their auto loan.

16. CarsDirect

- Minimum Credit Score: None.

- Conclusion: CarsDirect operates as a massive online auto broker network. It specifically connects buyers with poor credit histories directly to local dealers and lenders who are entirely willing to approve an auto loan despite specific adverse financial situations, such as exceptionally low income or a severely damaged past record.

17. Lendbuzz

- Minimum Credit Score: No minimum (Eligible even without any US credit history).

- Conclusion: This innovative company smartly utilizes artificial intelligence and machine learning to underwrite your next auto loan. It is the absolute best option for individuals like international students or expats who lack a standard US credit score. It carefully assesses your true financial capacity based purely on your employment status and personal bank statements.

18. OpenRoad Lending

- Minimum Credit Score: 560.

- Conclusion: This company specializes exclusively in vehicle refinancing specifically tailored to modify an existing auto loan. If you currently hold an extremely expensive car loan with incredibly high rates, utilizing this platform can seamlessly improve your auto loan terms and significantly lower your ongoing monthly payments.

19. First Investors Financial Services

- Minimum Credit Score: Flexible (Strongly subprime focused).

- Conclusion: Having operated reliably in the subprime auto loan financing sector for several decades, this is a highly trusted institution. It primarily operates through a select network of authorized dealerships, specifically targeting consumers who are actively trying to recover from bankruptcy or severe credit setbacks.

20. RefiJet

- Minimum Credit Score: Above 500.

- Conclusion: This is another top-tier vehicle refinance marketplace that can handle a subprime auto loan. It exists solely to assist people with poor credit who desperately want to reduce their current inflated interest rates or heavily modify the duration of their existing terms. Their customer care team is widely renowned for being highly personalized and exceptionally helpful throughout the auto loan process.

Top 10 Auto Loan FAQs Every Car Buyer Should Know

Q1: What is the current average interest rate for a new auto loan?

A1: The current average interest rate for a new auto loan in the US market is approximately 7.04% for a standard 60-month financing term.

Q2: Why are used car financing rates higher than new car rates?

A2: Used cars carry higher risk for financial institutions due to unpredictable vehicle depreciation, pushing the average used car APR above 10.60%.

Q3: How does a consumer’s credit score directly affect an auto loan APR?

A3: Lenders use credit tiers to determine risk; borrowers with Super Prime scores (781+) unlock the lowest rates, while subprime tiers face heavily inflated interest charges.

Q4: Should I choose a traditional bank or a credit union for vehicle financing?

A4: Non-profit credit unions consistently offer lower interest rates and flexible underwriting, whereas for-profit traditional giant banks provide superior digital management ecosystems.

Q5: What is the 20/4/10 rule in car purchasing?

A5: It is a budgeting strategy recommending a 20% down payment, a maximum loan duration of 4 years, and keeping total transport costs under 10% of your take-home income.

Q6: What are the typical age and mileage restrictions for a used auto loan?

A6: Most mainstream financial institutions will refuse financing for pre-owned vehicles that are more than 10 years old or have exceeded 100,000 miles.

Q7: What is the operational difference between the base interest rate and the APR?

A7: The interest rate is strictly the percentage charged for borrowing the principal, while the APR represents the true total cost, including hidden administrative fees.

Q8: Can I refinance my auto loan if national market rates drop?

A8: Yes, you can replace your current contract by securing a refinance auto loan at any time to capture a lower monthly payment if market conditions improve.

Q9: What is negative equity, and how can a buyer easily avoid it?

A9: Negative equity occurs when your outstanding balance is higher than the car’s actual resale value; you can avoid this trap by making a larger upfront down payment.

Q10: Why should a buyer get a pre-approved auto loan before visiting a dealership?

A10: Walking in with a pre-approved auto loan grants you the absolute negotiating power of a cash buyer and effectively protects you from dealership financing markups.