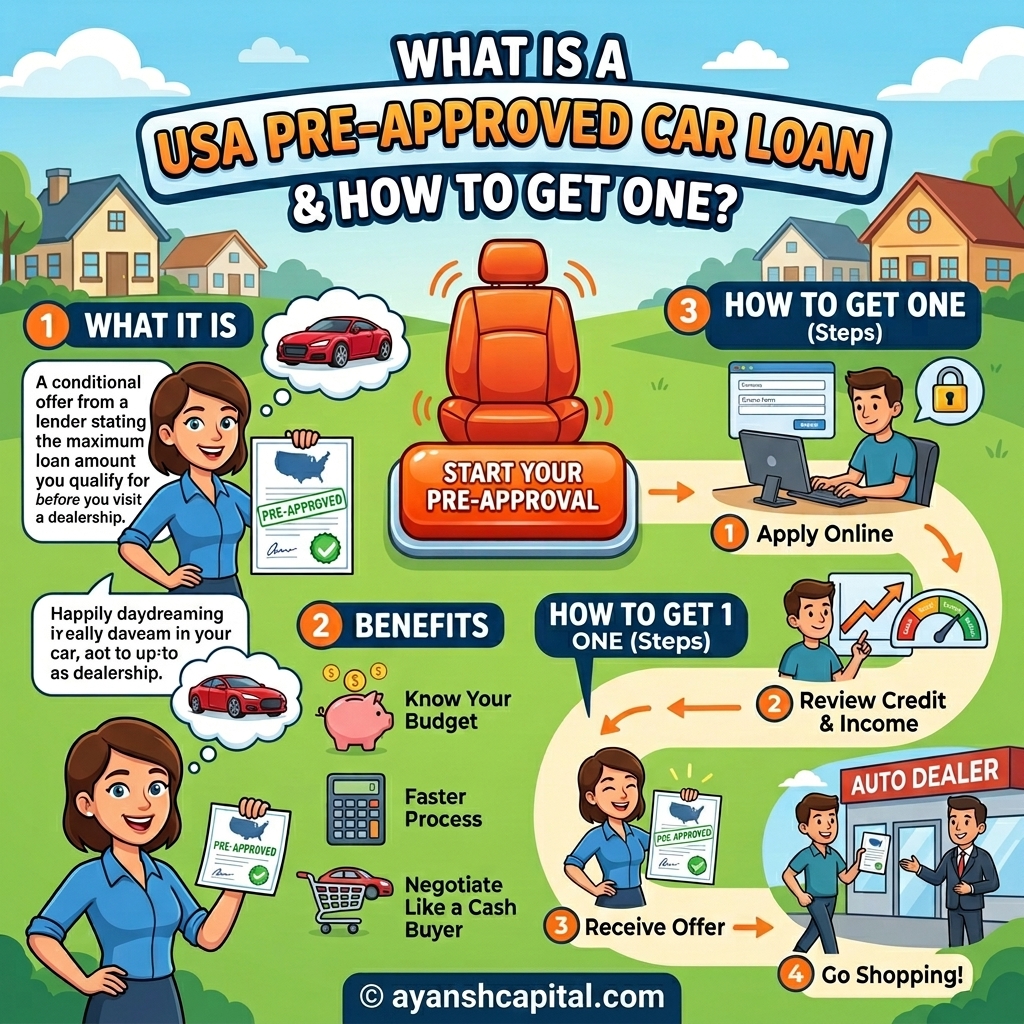

What Is a USA Pre Approved Car Loan and How to Get One?

A Pre Approved Car Loan is essentially an official and formal document issued by a lender (bank, credit union, or online loan provider). It serves as solid proof that the lender has thoroughly examined your financial records (credit score, income, and debt-to-income ratio) and is willing to lend you money to buy a car under specific terms.

To understand this system deeply, the main components and the working mechanism of a Pre Approved Car Loan are explained in detail below:

1. What is included in a Pre-Approval Letter?

When a bank gives you a Pre Approved Car Loan, it provides you with a letter or a digital certificate in which the following 4 crucial pieces of information are clearly stated:

- Maximum Loan Amount: The maximum limit (e.g., $30,000) the bank is willing to provide you. You can buy a car for less than this, but not more (unless you pay an additional down payment out of your pocket).

- Annual Percentage Rate (APR / Interest Rate): The exact interest rate applicable to your loan. This is determined based on your credit score and remains fixed.

- Loan Term: The time you will get to repay the loan (e.g., 48, 60, or 72 months).

- Expiration Date: A Pre Approved Car Loan does not last forever. It is usually valid for 30 to 60 days. During this period, you need to select a car and finalize the deal.

2. How Do You Become a “Cash Buyer”?

In the dealership world, a “cash buyer” (a customer who pays in cash) is considered the strongest. A Pre Approved Car Loan letter puts financial control in your hands, placing you right in this category. Its mechanism works as follows:

- Freedom from the Dealer’s Trap: Car dealers often make more profit by selling you their expensive loan (In-house Financing) than by selling the car itself. Instead of telling you the total price of the vehicle, they trap you in the maze of a “low monthly payment.” Having a Pre Approved Car Loan ensures you do not fall into this trap.

- Money Guarantee: The lender gives you a pre-approved check (blank check) or draft. Once the car’s price is finalized at the dealership, you hand over that check to the dealer. The dealer gets full payment immediately from the bank in exchange for that check. Therefore, to the dealer, you are exactly like a person who has walked in with a suitcase full of cash.

3. The Power You Get in Negotiation

Strategic Advantage: When you have a Pre Approved Car Loan, the entire dynamic of negotiation at the dealership changes. You are in an offensive position rather than a defensive one.

- Discussing Only the ‘Out-the-Door’ Price: You can directly tell the dealer: “My financing is already sorted. I just need to know the final out-the-door price (including taxes and fees) for this car.” This prevents the salesman from adding any unnecessary expenses or hidden fees.

- Power to Challenge the Dealer: You can play your Pre Approved Car Loan card in front of the dealer. For example, if your bank is offering you a 5% APR, you can tell the dealer’s finance manager, “I have an offer of 5%. Only if you can give me a lower rate (like 4.5%), will I take a loan through you.” Often, dealers offer better rates than the bank just to boost their sales.

In short, a Pre Approved Car Loan is a solid financial agreement between you and the lender. By showing it, you can negotiate solely on the true price of the car at the dealership without any mental stress, just like a king.

Pre-Qualification vs. Pre-Approval: Detailed Differences in the USA Financial Market

When understanding the car loan process in the United States (USA) auto finance market, the two most confusing terms are “Pre-Qualification” and “Pre-Approval”, especially when seeking a Pre Approved Car Loan. Often, people consider them to be the same, which can prove to be an expensive mistake upon visiting the dealership.

Although both of these help you estimate how much you can spend on a car, their working mechanism and their impact at the dealership are completely different. Let us understand the difference between these two in detail based on the points provided by you:

1. Credit Check: Soft Pull vs. Hard Pull

Lenders in the USA use your FICO credit score to approve your loan. The method of checking credit is completely different in both of these processes:

- Pre-Qualification (Soft Pull): When you pre-qualify, the bank only does a superficial check of your credit history. This is called a ‘soft inquiry’. The biggest advantage is that your credit score does not drop at all from this. It is only to see whether you meet the basic criteria before eventually applying for a Pre Approved Car Loan.

- Pre-Approval (Hard Pull): For a Pre Approved Car Loan, a serious and detailed check is conducted. The lender pulls a complete copy of your credit report (like from Experian, Equifax, or TransUnion). This is called a ‘hard inquiry’. This can cause a temporary minor drop (usually 2 to 5 points) in your credit score. This is necessary for the lender so that they can accurately assess your complete financial situation for a Pre Approved Car Loan.

2. Data Accuracy: Estimated vs. Verified

The interest rate (APR) and loan amount the bank will offer you depends on the accuracy of the data.

- Pre-Qualification (Estimated Data): This is entirely based on the information provided by you. You fill in your income, debt, and employment status in an online form, and the bank provides an estimated offer based on that without asking for any documents. Because documents are not verified in this, the final rates may change when you actually pursue a Pre Approved Car Loan.

- Pre-Approval (Accurate and Verified Data): Securing a Pre Approved Car Loan is a rigorous process. In this, the bank does not blindly trust the information provided by you. You have to submit documents like proof of income (such as Pay Stubs, W-2 forms, tax returns), proof of residence, and Social Security Number (SSN). The bank verifies these documents, therefore the offer you get is 100% accurate.

3. Importance at the Dealership: Simple Estimate vs. Power of a “Cash Buyer”

When you go to a dealership to buy a car, the dealer decides the negotiation approach with you just by looking at the letter in your hand.

- Pre-Qualification (Dealers do not take it seriously): If you show your pre-qualification letter to the dealer, they will consider it merely a “marketing tool” or an initial estimate, not a genuine Pre Approved Car Loan. The dealer knows that this loan is not yet guaranteed, so they will try their best to take you to their financing department (F&I Office) and sell you their expensive loan.

- Pre-Approval (Dealers treat it equal to “Cash”): In the dealership world, a Pre Approved Car Loan letter is an ultimate weapon. When you present this letter to the dealer, you effectively become a “Cash Buyer”. The dealer knows that your bank has given a solid guarantee to provide the money. After this, you do not need to rely on the dealer’s financing options, and you can negotiate purely on the ‘final price of the car’ with full confidence.

4. Guarantee: Raw Promise vs. Solid Offer

Does that piece of paper guarantee you will get the loan? The answer depends on what that paper is:

- Pre-Qualification (No Guarantee): This is not a guarantee of getting a loan in any way. It only tells you that “if the information you provided turns out to be true, you could possibly get this much loan.” When you officially apply for a Pre Approved Car Loan, the bank might even reject you.

- Pre-Approval (Solid Offer): This is an official and firm offer from the bank. The bank has checked you and is ready to give the money. Although it is not entirely “unconditional” (for example, you will have to give the car’s title to the bank, or the car must be within a certain age/mileage limit), if you meet the lender’s basic conditions, your Pre Approved Car Loan is 100% guaranteed.

Conclusion: What Should You Choose?

- If you are just considering right now and want to know how expensive a car you can dream of (without ruining your credit score), then pre-qualification is right.

- However, if you are fully prepared to buy a car in the next few days or weeks and are heading to the dealership, having a Pre Approved Car Loan is mandatory. This is the tool that gives you true negotiation power.

Why is it necessary to get a Pre Approved Car Loan before going to the dealership?

When buying a car in the USA, securing a Pre Approved Car Loan is the most important step for your financial security. The four main reasons you mentioned are absolutely accurate. Let’s understand these four points deeply to make it clear how a Pre Approved Car Loan saves your money, time, and peace of mind:

1. Protection from Dealer Markup

In the US auto finance market, dealerships often work on the “Indirect Lending” model. This is a huge source of profit for them.

- How it works: When you take a loan through the dealer’s finance manager instead of having a Pre Approved Car Loan, they send your credit profile to various banks. Suppose your credit score is very good and the bank offers the dealer a base interest rate of 5% (called the ‘Buy Rate’).

- Hidden profit: The dealer does not tell you this real rate (5%). Instead, they add 1% to 3% (or even more) of their own profit to it and offer you a rate of 7% or 8% (called the ‘Contract Rate’). This extra interest goes straight into the dealership’s pocket.

- Advantage of a Pre Approved Car Loan: When you already go with an approval letter from a bank or credit union, you connect directly with the lender. This eliminates the middleman (dealer), and you completely avoid this hidden ‘markup’, which can save you thousands of dollars over the term of the loan.

2. Budget Clarity

Going to buy a car without a Pre Approved Car Loan is like going to a supermarket without a list, where you fall for the dealer’s enticing words and spend beyond your capacity. A Pre Approved Car Loan letter completely clarifies your financial scope. It contains the exact math of three main things:

- Maximum Purchasing Power: You know exactly the maximum amount the bank is willing to lend you through your Pre Approved Car Loan. This saves you from getting attracted to those expensive cars or unnecessary upgrades at the dealership that are out of your budget.

- Monthly Payment (Monthly EMI): Your interest rate (APR) and loan term are predetermined, so you know exactly how much money will be deducted from your bank account every month. There is no guesswork involved.

- Down Payment Clarity: If the total price of your preferred car exceeds your Pre Approved Car Loan amount, it becomes clear to you that you will have to pay the remaining amount out of your pocket (as a down payment). Because this math is predetermined, you do not experience any financial shock at the dealership.

3. Negotiation Power

The biggest psychological game at a dealership is played on ‘monthly payments’.

- The Trap of Monthly Installments: A clever car salesman will always ask you, “How much do you want to pay every month?” If you tell them a small amount, they will increase the loan term from 48 months to 72 or 84 months. This makes your monthly installment look small, but in reality, you will be paying much more interest than the price of the car.

- Focus on the ‘Out-the-Door’ Price: Having a Pre Approved Car Loan completely cuts through this trap. Your answer is straightforward: “My financing is already fixed, I don’t want to talk about installments.” After this, the entire focus of the conversation shifts solely to reducing the real and final price of the car—the “out-the-door” price (which includes the car’s value, taxes, and all necessary fees). You act like a cash buyer, which makes you completely dominant in the negotiation.

4. Time Saving

The car-buying process in the USA can be extremely exhausting. After selecting a car, the real wait begins outside the Finance and Insurance (F&I) office.

- Time Taken in Dealer Financing: If you get financing from the dealer, the F&I manager fills out your application, sends it to several banks, waits for their response, and then prepares a deal for you. This entire process can sometimes take 3 to 5 hours.

- Time Saving with a Pre Approved Car Loan: If you already have your Pre Approved Car Loan check or letter, all this hassle is eliminated. You don’t have to wait for the bank’s approval. The paperwork time is instantly cut in half (or even less). You just have to finalize the car’s price, sign the purchase agreement, hand over your pre-approved check, and drive home with your new car keys in very little time.

Step-by-Step Process to Get a Pre Approved Car Loan

Getting a Pre Approved Car Loan in the USA is not a simple task; it is a strategic process. If you do it correctly, you can not only secure the best interest rate (Best APR) but also save thousands of dollars at the dealership.

Let’s deeply analyze these 6 crucial steps you mentioned to secure a Pre Approved Car Loan:

1. Check Your Credit Score (FICO Score)

In USA auto finance, your FICO score is the key that opens the doors to cheap interest rates for a Pre Approved Car Loan.

- Importance of FICO Auto Score: Banks do not just look at your standard credit score; they look at the ‘FICO Auto Score 8 or 9’. This specific score puts more emphasis on how you have repaid past car loans (if any).

- Checking for Errors: Sometimes wrong late payments or old debts remain recorded on the credit report, which drops the score. Pull your report from AnnualCreditReport.com and get any error ‘disputed’ and corrected at least 30 days before applying for a Pre Approved Car Loan.

- Tip: If your score is below 660, consider adding a co-signer to get a better rate on your Pre Approved Car Loan.

2. Determine Your Budget and DTI (Debt-to-Income) Ratio

Lenders do not just look at how much you earn, but they look at how much is left from your earnings.

- The Math of DTI (Debt-to-Income Ratio): Divide your total monthly income (before taxes) by all your monthly debts (credit card bills, mortgage, other loans). Banks want this figure to stay below 36%. If your DTI is above 45-50%, getting a Pre Approved Car Loan becomes very difficult.

- The 10-15% Golden Rule: A car is not limited to just the EMI. It also includes insurance, gas, and maintenance. Therefore, the total car expenses should not exceed 15% of your take-home salary. This will save you from becoming “car-poor” (having a car but empty pockets).

3. Gather the Necessary Documents

Financial regulations in the USA are very strict (under the Patriot Act). If you do not upload the correct documents while applying, your Pre Approved Car Loan will go into ‘pending’ status.

- Nuances of Proof of Income: If you are employed (W-2 Employee), banks will look at your recent ‘pay-stub’ which has the ‘Year-to-Date’ (YTD) income recorded. If you are self-employed (1099), banks will not just accept bank statements; they will need the last 2 years of tax returns (Schedule C).

- Proof of Residence: Your utility bill (electricity/water bill) must 100% match the address provided on your application.

- Advantage of Preparation: If you have these documents ready in PDF format, you can get a digital Pre Approved Car Loan within 15 minutes of applying online.

4. Shop Around Among Lenders

Never rely entirely on your primary bank (where you have your checking account). Rates vary everywhere:

- Credit Unions: These are non-profit organizations, so their interest rates are always 1% to 2% lower than traditional banks. PenFed or Navy Federal (if you are from a military family) or your city’s local credit union are the best options for a Pre Approved Car Loan.

- Traditional Banks (Chase, Bank of America): If your credit is very good and you have an old account with these banks, they can give you a ‘relationship discount’ (0.25% to 0.50% off).

- Online Lenders (LightStream, Capital One): These are technologically very advanced. You can easily check rates through their apps, and their money transfer is also the fastest.

5. Apply within a 14-45 Day Window (Rate Shopping Window)

The biggest myth among car buyers is that “applying for a loan every time will drop my credit score drastically.” This is not true.

- FICO Rate Shopping Rule: The FICO scoring model knows that consumers shop around for the best rates. If you apply (Hard Pull) for a Pre Approved Car Loan at 5 different banks within a timeframe of 14 to 45 days (depending on different bureaus), its impact on your credit score will not be of 5 inquiries, but only 1 inquiry.

- Strategy: Complete all your applications within 2 to 3 days (like over a weekend) so you can choose the best rate without the fear of your credit score dropping.

6. Review Offers and Receive the Pre-Approval Letter

After receiving offers from all lenders, the real math begins. Don’t just look at the ‘monthly installment’, but understand the complete math of your Pre Approved Car Loan:

- APR vs. Interest Rate: Always check the APR (Annual Percentage Rate) because it includes the loan processing fees along with the principal interest.

- The Trap of Long Loans (72-84 months): The installment looks very small in an 84-month loan, but it is a financial disaster. The car’s value depreciates rapidly. In an 84-month loan, you will soon end up in ‘negative equity’ (underwater)—meaning you will owe the bank more than your car’s market value. Always choose a 48 to 60-month loan.

- The Power of the Blank Check: When you choose the best offer, the bank sends you a ‘blank check’ or an authorization code. Now you can take this check to the dealership. The dealer will know that you have guaranteed money, and the deal will be completed the same day.

How to Use Pre-Approval at the Dealership?

When you enter a dealership holding a Pre Approved Car Loan letter or a blank check, you hold a massive strategic advantage. However, dealers are highly skilled negotiators. If you do not utilize this power at the right moment, you will not reap its full benefits. Let’s understand in detail how to use a Pre Approved Car Loan at the dealership:

1. Disclose Your Financing at the End (The Art of Withholding Information)

Salesmen at US dealerships often use the “Four-Square Method”—combining the car’s price, trade-in value, down payment, and monthly installments to confuse you. Their primary goal is to find out how much you can pay every month.

- Strategy: When the salesman asks, “How will you finance?” or “What is your monthly budget?”, you need to adopt a firm but polite stance. Do not reveal your Pre Approved Car Loan yet.

- What to Say: “I only want to negotiate the cash ‘Out-the-Door’ price of the car right now. Once we agree on the correct price of the car, we will discuss financing.”

- The Benefit: Doing this forces the dealer to lower the car’s price. If you reveal initially that you have a Pre Approved Car Loan check from the bank, the dealer will show absolutely no interest in lowering the car’s price (MSRP) because they know they will not get any extra profit (markup) from the financing.

2. Let the Dealer Beat Your Rate

Once you reach a written agreement on the ‘Out-the-Door’ price (including taxes, title, and dealer fees), you head into the dealer’s Finance and Insurance (F&I) manager’s office. Here is where you play your Pre Approved Car Loan card.

- Manufacturers’ Captive Lenders: Often, car manufacturers have their own finance companies (e.g., Toyota Financial Services, Ford Motor Credit). To boost sales of their cars, these companies frequently offer heavily subvented rates, such as 0%, 0.9%, or 1.9% APR. Your bank can rarely compete with these rates.

- How to Talk: Show your letter to the F&I manager and say, “I have a firm offer of a 5% APR with my Pre Approved Car Loan from my credit union. If you can give me a lower rate—without extending the loan term—I am willing to take your financing.”

- Warning: Ensure that the dealer does not extend the loan term (e.g., from 60 to 72 months) in their attempt to lower your rate. With an extended term, you will end up paying more interest overall despite the lower rate.

3. Avoid the Yo-Yo Financing Scam (Spot Delivery Scam)

This is a highly notorious scam in the US car market, also known as ‘spot delivery’.

- How the Scam Works: If you get financing through the dealership on a weekend (when banks are closed) or in the evening, the dealer hands you the keys and says the financing is “Pending Approval.” You happily take the car home (the Yo-Yo rolls out). A few days later, the dealer calls saying “your loan wasn’t approved” and forces you to return to the dealership to sign papers for a higher interest rate or a larger down payment (the Yo-Yo is yanked back).

- Safety Net: If you have your Pre Approved Car Loan check, you are 100% safe from this scam. Your bank has already guaranteed the money. There is no “pending” status. The deal is finalized at that very moment.

Validity and Limitations of a Pre-Approval Letter

A Pre Approved Car Loan is not an “open-ended” check. It has its own strict financial and legal limitations; ignoring them can cause your check to bounce or the lender to withhold funding.

1. Time Limit (Expiration)

In the auto finance market, interest rates change daily according to the Federal Reserve’s policies and market fluctuations.

- Limitation: Therefore, no lender can guarantee the same rate forever. In the USA, a Pre Approved Car Loan from most banks, credit unions, and online lenders is valid for only 30 to 60 days.

- Impact: If you do not buy a car within this timeframe, your Pre Approved Car Loan letter will expire. You will have to reapply, which means another ‘hard pull’ (hard inquiry) on your credit, potentially causing your score to drop slightly again.

2. Vehicle Age and Mileage Restrictions

Lenders view the car as collateral. If you default on the loan, they will repossess the car and auction it.

- Age and Mileage Limits: Older cars with high mileage lose their resale value very quickly and carry a higher risk of breaking down. Therefore, most major banks (like Chase or Bank of America) will refuse to let you use a Pre Approved Car Loan check for cars that are more than 10 years old or have an odometer reading exceeding 100,000 miles.

- Tip: If you want to buy such an older car, you will need to speak with specific “used car lenders” or local credit unions whose rules are slightly more flexible.

3. Branded Titles (Salvage or Rebuilt)

Apart from cars with a ‘Clean Title’, some cars in the USA have branded titles.

- Salvage: When a car is so severely damaged in an accident, flood, or fire that the cost of repairing it exceeds its value (totaled), the insurance company declares it ‘salvage’.

- Rebuilt: When that same salvage car is repaired and made roadworthy again.

- Limitation: Almost 99% of traditional lenders will not let you use your Pre Approved Car Loan to buy a car with a branded title. Banks cannot accurately determine the value of such cars, and getting full coverage insurance for them in case of an accident is extremely difficult.

4. Maximum Loan-to-Value Limit

Banks approve you for a certain amount (e.g., $35,000) for a Pre Approved Car Loan, but this doesn’t mean you can use this amount any way you please. Banks take the LTV (Loan-to-Value) ratio very seriously.

- The Math of LTV: If the actual market value of the car (e.g., KBB – Kelley Blue Book value) is $25,000, the bank will not give you $30,000 for that car, even if your Pre Approved Car Loan is for $35,000. They typically finance only 100% to 120% of the car’s value (to cover taxes, etc.).

- Impact of Out-the-Door (OTD) Price: When buying a car in the USA, State Sales Tax, Title fees, and Dealer Documentation Fees (Doc Fees) combined increase the car’s price by 8% to 10%. If this total amount exceeds the maximum limit of your Pre Approved Car Loan check, you must pay that extra difference out of your pocket as a cash down paymen

Main Reasons for a Pre Approved Car Loan Denial: A Detailed Analysis

If you have applied for a Pre Approved Car Loan and the lender (bank or credit union) has denied it, there is no need to be disappointed. In the USA auto finance market, lenders follow strict standards to mitigate risk. Rejections are usually based on the following solid financial reasons:

1. High Debt-to-Income (DTI) Ratio

In the USA, after your FICO score, lenders pay the most attention to your DTI (Debt-to-Income) Ratio.

- What it is: The percentage of your Gross Monthly Income that goes towards paying your existing debts (e.g., credit card bills, student loans, personal loans, and mortgage payments).

- Reason for Denial: Most American lenders prefer a DTI between 36% and 43%. If you earn $5,000 a month and $2,500 is already going into other installments (meaning your DTI is 50%), the lender will feel that you will not be able to bear the burden of a new car installment. In such a situation, despite having an excellent credit score, your application for a Pre Approved Car Loan will be rejected.

2. Lack of Credit History (Thin Credit File or No Credit)

The financial system in the USA runs entirely on credit history. “No Credit” is often considered as risky as “Bad Credit”.

- Who it affects: If you have recently immigrated to the USA, have recently graduated from college, or have never used a credit card or loan, your credit file will be considered ‘Thin’.

- Lender’s Perspective: Since you do not have a past record of taking a loan and repaying it, the lender cannot predict how responsible you will be towards a car loan, which is why they reject the application for a Pre Approved Car Loan.

3. Employment Instability

A Pre Approved Car Loan is a long-term commitment (4 to 6 years), so lenders need stability in your employment.

- Lack of Continuity: If you have changed jobs 3 or 4 times in the last year, or if there are long gaps in your employment history, it is a ‘red flag’ for the lender. USA lenders generally want to see a continuous employment history of 1 to 2 years in the same company or at least the same industry.

- Self-Employed (1099): If you are not a W-2 employee and do freelancing or run your own business, proving income is difficult. If you cannot present tax returns for the last 2 years, the application for your Pre Approved Car Loan may be rejected.

4. Derogatory Marks on Credit Report

Negative events recorded in your credit history scare lenders the most.

- Serious Reasons: If your report shows a recently filed bankruptcy (Chapter 7 or 13), a repossession of a previous car (car seized for non-payment of installments), or a foreclosure, traditional banks will immediately reject a Pre Approved Car Loan.

- Late Payments: Payments delayed by 30, 60, or 90 consecutive days on credit cards or old loans, or any account sent to ‘Collections’, become a major reason for the denial of a Pre Approved Car Loan.

Solutions: What to do after a denial?

If your application is rejected, you have three strong options:

- Add a Co-signer: Find a family member or friend whose FICO score is excellent (700+) and has a low DTI. The co-signer provides a legal guarantee that if you do not pay, they will. This eliminates the lender’s risk, and the loan is approved.

- Increase the Down Payment: If you make a 20% or 30% cash down payment upfront, the bank will have to lend less money (LTV will decrease). Due to the lower risk, they might consider approving the loan.

- Choose a Cheaper Car: If your Pre Approved Car Loan was rejected because the car was out of your budget, choose a lower-priced car so that your potential monthly installment falls within your DTI ratio limits.

Frequently Asked Questions (10 FAQs) – USA Pre Approved Car Loan

1. Will getting a Pre Approved Car Loan lower my credit score?

Yes, but the impact is very minimal. When the lender does a “Hard Pull” (Hard Inquiry) to check your profile, your FICO score can temporarily drop by 2 to 5 points. However, the FICO model allows for ‘Rate Shopping’. If you apply to even 4-5 lenders within a 14 to 45-day window, the credit bureaus combine them all and consider it as only a single inquiry.

2. Can I use a Pre Approved Car Loan at any dealership?

In most cases, yes. The blank check the bank gives you is easily accepted by franchised dealerships like Ford, Honda, Toyota, or large used car dealers (like CarMax). However, some small independent dealers, known as “Buy Here Pay Here” (BHPH), do not accept outside financing because they only want to sell their own expensive loans.

3. If I have secured a Pre Approved Car Loan, do I have to buy a car from the dealership?

Absolutely not. A Pre Approved Car Loan is merely an ‘offer’ from the bank, not an ‘obligation’ for you. If you do not find a car of your choice or at the right price within 30-60 days, that offer will automatically expire. You will not have to pay any cancellation fees or penalties to the bank for this.

4. Can a Pre Approved Car Loan be taken for a used car?

Yes, absolutely. But remember that the interest rate (APR) for used cars is usually 1% to 3% higher than for new cars. The reason for this is that used cars lose their value (Depreciation) quickly, making the investment riskier for the lender. Also, lenders can impose conditions on the age (e.g., not older than 10 years) and mileage (under 100,000 miles) of the used car.

5. How long does the Pre Approved Car Loan process take?

This process has become very fast in the USA now. If you apply to online lenders or large banks (like Capital One, Chase) and your documents are perfect, AI-based systems can give you a digital Pre Approved Car Loan letter in just a few minutes. If there are complications in your application (like being self-employed), manual review can take 24 to 48 hours.

6. Does a Pre Approved Car Loan letter lock in my interest rate?

Yes. This is the biggest advantage of pre-approval. The APR (e.g., 6.5%) printed on your letter is locked in for its validity period (usually 30 to 60 days). Even if the ‘Federal Reserve’ increases interest rates in the meantime, the bank is legally obligated to give you the loan at that same old (lower) rate.

7. Can I get a Pre Approved Car Loan even with bad credit (Subprime)?

Yes, you can, but you will have to look for ‘Subprime Lenders’ instead of traditional banks. Pre-approval is even more crucial for those with bad credit, because if you go to a dealership without it, the dealer can take advantage of your bad score and impose dangerous interest rates like 20-25% on you.

8. What happens if the price of the car I want is higher than my Pre Approved Car Loan amount?

Your maximum limit is set in the pre-approval letter (let’s say $30,000). If the ‘Out-the-Door’ price (including taxes and fees) of the car you are buying comes to $35,000, the bank will not give you the extra money. You will have to pay the remaining amount of $5,000 out of your own pocket to the dealer as a cash down payment.

9. Can I use a Pre Approved Car Loan to buy a car from a ‘Private Party’?

Yes, but the rules for this are slightly different. You must tell the lender in advance that you are buying a car from an individual, not a dealership. The bank will give you a specific “Private Party Auto Loan”. In this, the bank checks the car’s title and condition more strictly to ensure that the car is not stolen or ‘salvage’.

10. What is the difference between a Co-signer and a Co-borrower?

Understanding this difference is crucial when getting pre-approval. A Co-signer only guarantees to repay the loan, but their name is not on the car’s title (ownership). On the other hand, a Co-borrower (like a spouse) shares both the responsibility of the loan and the ownership (Title) of the car. In both cases, the credit scores of both individuals are checked.

Conclusion

Buying a car in the US automotive market is not just about picking a vehicle; it is a major financial decision that impacts your budget for years to come. A dealership is a business, and their main objective is to maximize their profit through financing (F&I office).

Getting a Pre Approved Car Loan before going to the dealership is the ‘shield’ that protects you from this game of profits. It not only saves you thousands of dollars but also gives you peace of mind.

Start your financial journey by checking your FICO report, create a realistic budget according to your income and debt (DTI), and rate shop among banks, credit unions, and online lenders for the best interest rates. When you step through the dealership doors holding an approved blank check, you will not be a scared customer, but a ‘Cash Buyer’. At that moment, you will have complete control of the entire negotiation—you will be strong, secure, and fully prepared to crack a great deal without compromising your financial future.