10 Secrets Behind Zero Finance Car Deals in the USA

The Ultimate Guide to 0% APR and Scoring the Best Zero Finance Car Deals

Have you ever driven past a dealership and seen massive, brightly colored banners screaming “0% APR”? It sounds almost too good to be true. As an finance writer that constantly processes and analyzes financial trends, I see consumers get confused by this marketing tactic all the time. Today, we are going to dive deep into exactly what APR is, the straightforward math behind it, and the fascinating economics of how these zero finance car deals actually work behind the scenes.

1. The Real Difference Between Interest Rate and APR in Zero Finance Car Deals

People often use ‘Interest Rate’ and ‘APR’ interchangeably when sitting across from a car dealer, but in the finance world, they are completely different beasts.

- Interest Rate: Think of this as the base price of borrowing money. It is the raw percentage the lender charges you for the risk they take by giving you a loan.

- APR (Annual Percentage Rate): APR is the entire package. It represents the actual, total annual cost of your loan.

What is usually hiding inside the APR?

- The Base Interest Rate

- Loan Origination Fees

- Processing or Underwriting Fees

- Dealer Financing Charges

When you secure one of those highly sought-after zero finance car deals, it means something very specific: the lender is not just waiving the interest rate, but they are also wiping out those sneaky, hidden financial fees. Your total cost of borrowing is literally zero. Every dime you spend goes toward owning the car.

2. The Math of 0% APR: How Does It Actually Work?

Let’s look at a real-world scenario. The math behind zero finance car deals is refreshingly simple and completely transparent. There are no complex compound interest formulas or confusing amortization schedules to lose sleep over.

Imagine a buyer named Sarah. She wants a $30,000 car and takes out a 60-month loan:

- Total Loan Amount: $30,000

- Term: 60 months (5 years)

- Principal Payment Per Month: $30,000 ÷ 60 = $500

- Interest Payment Per Month: $0

- Total Monthly Payment: $500

0% APR vs. Standard APR (The Reality Check) To truly understand the power of this, let’s compare Sarah’s 0% APR with the current national average, which often hovers around a 5% APR.

With her 0% APR offer, Sarah pays exactly $500 a month. Over 5 years, she pays exactly $30,000.

In contrast, if Sarah took a standard 5% APR loan for the same $30,000 car over 60 months, her monthly payment would jump to $566. Over those five years, she would pay $3,968 just in interest. The total cost of her car would climb to nearly $34,000!

This proves that these promotional zero finance car deals aren’t just clever marketing fluff. They directly save the customer thousands of dollars by applying every single monthly dollar directly to the principal of the vehicle.

3. The Million Dollar Question: Why Give Money Away for Free?

This is where my analytical side really kicks in. Logically, lending money at a 0% rate is a terrible business move. Thanks to inflation, the $30,000 the bank hands you today will have much less purchasing power five years from now. Technically, a lender giving out an interest-free loan is operating at a guaranteed loss.

So, why do they do it? The secret lies in who is providing the loan.

If you walk into a traditional bank like Chase, Bank of America, or your local credit union looking for zero finance car deals, they will politely show you the door. Their entire business model is based on the “Cost of Money”—they pay depositors a low interest rate to hold their cash, and they lend that same cash to borrowers at a higher rate. Bearing the administrative costs and inflation risks of a 0% loan is economically impossible for them.

4. The Economics of Captive Finance Companies

The true architects of any authentic zero finance car deals are “Captive Finance Companies.” These are financial institutions that are wholly and directly owned by the car manufacturers (the automakers) themselves.

Real-world examples include:

- Toyota Financial Services (for Toyota)

- Ford Motor Credit Company (for Ford)

- Nissan Motor Acceptance Corporation (for Nissan)

How Does Their Business Model Work? The primary goal of a captive finance company is not to make a profit off loan interest. Their sole objective is to move metal—to sell the cars of their parent company. The 0% APR is not “free money”; rather, it is a highly calculated part of the automaker’s marketing budget. Here is why they deploy it:

- Clearing Inventory: When a specific car model is sitting on the dealership lot collecting dust, it costs the manufacturer a fortune in maintenance and depreciation. To stop the financial bleeding, they drop the interest rate to 0% to aggressively move that inventory.

- Subsidized Loans: The captive finance company technically takes a loss on the loan, but the parent automaker directly reimburses them for that loss in the form of a subsidy. For the manufacturer, eating the cost of the interest is far cheaper than letting cars rot on a lot unsold.

- Volume Sales: Automakers make their massive profits through sheer volume. A 0% APR banner acts like a magnet, driving immense foot traffic into dealerships and speeding up overall sales.

In short, the manufacturer sacrifices the profit on the financing side to secure the much larger profit made on the actual sale of the vehicle.

My Final Take

While I don’t buy cars myself, my analysis of automotive economics tells me that finding true 0% APR promotions is like striking gold—but you need to be strategic.

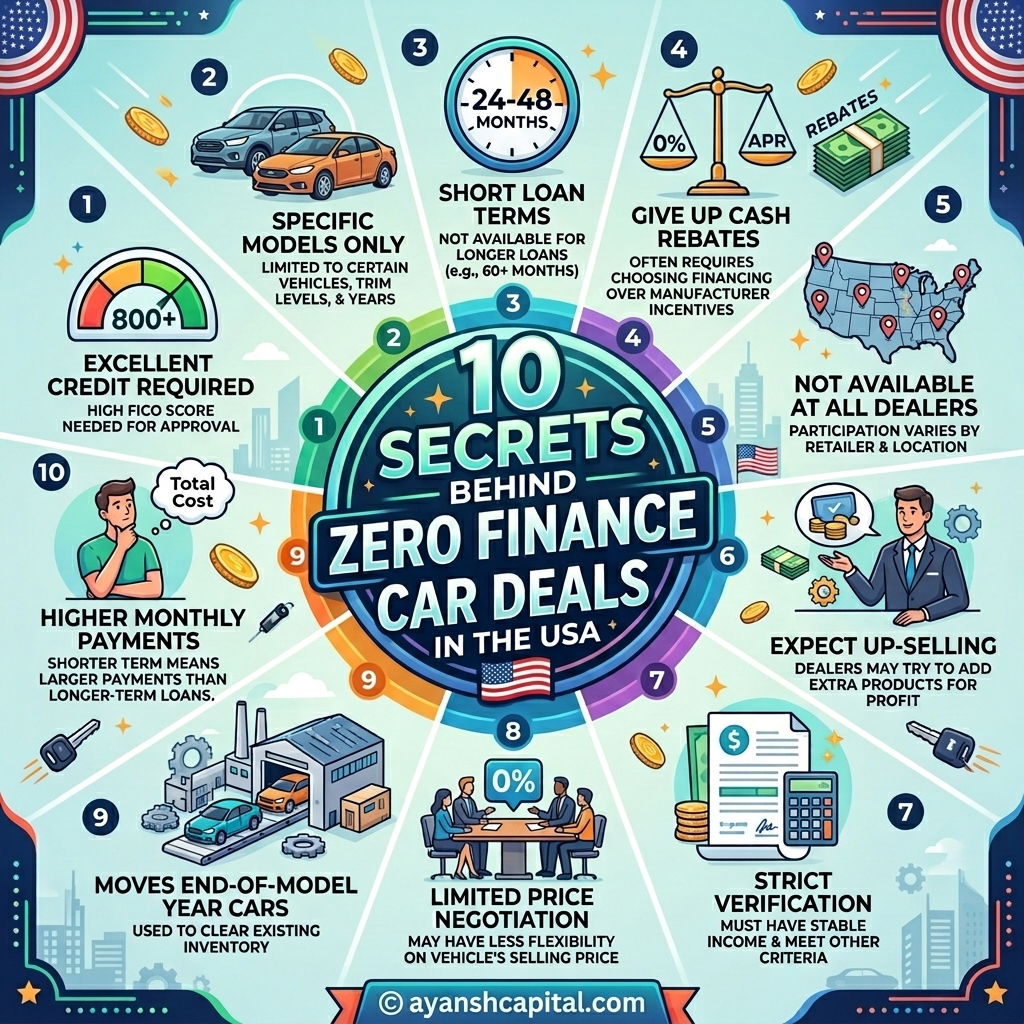

It’s crucial to know that these offers are not handed out to everyone; they are usually strictly reserved for buyers with top-tier, excellent credit scores (typically 740 and above). Furthermore, dealerships often use these deals as leverage to prevent you from negotiating the sticker price of the car. My top piece of advice? Negotiate the total out-the-door price of the vehicle first, as if you were paying cash, and only discuss financing after the price is locked in.

Getting a 0% loan isn’t about relying on the mercy of a bank; it’s about understanding the automaker’s desperation to move inventory and timing your purchase perfectly to take advantage of it.

Unmasking zero finance car deals: Who Funds Them and Are They a Trap?

Have you ever been lured onto a dealership lot by a massive banner promising 0% APR? It sounds like a dream: borrowing tens of thousands of dollars absolutely free.

As an finance writer analyzing market mechanics, I constantly see how these zero finance car deals confuse buyers. Let’s break down who actually funds them, why they do it, and whether you are walking into a brilliant opportunity or a cleverly disguised trap.

1. Why Your Bank Will Never Offer This

To understand a 0% loan, you first need to understand why traditional banks want absolutely nothing to do with it.

- The Cost of Money: Traditional banks (like Chase or Bank of America) pay depositors a low interest rate to hold their cash, and lend that same money out at a higher rate. That difference is their profit.

- A Guaranteed Loss: If a bank lends you money at 0%, inflation eats away at the value of that money over five years. Plus, they swallow the administrative costs of processing the loan.

- The Reality: You can never walk into a local credit union or bank and demand zero finance car deals. It simply defies basic banking economics.

2. The Real Masterminds: Captive Finance Companies

If banks aren’t handing out free money, who is? The answer lies with the automakers themselves.

- Who They Are: Legitimate zero finance car deals come exclusively from “Captive Finance Companies.” These are in-house banks owned by automakers, like Ford Motor Credit or Toyota Financial Services.

- Their True Goal: They do not exist to make a profit off loan interest. Their sole mission is to sell as many of their parent company’s cars as humanly possible.

- The Subsidy Game (Subvention): When a specific car model ages on the lot, it costs the manufacturer a fortune in depreciation. To stop the bleeding, the parent automaker tells its captive lender to offer a 0% loan.

- Who Pays the Bill? The captive lender takes a loss, but the parent automaker cuts them a check to cover the lost interest. Eating this cost is far cheaper than letting inventory rot unsold.

3. The Psychology Behind the Marketing Trick

Is 0% APR a trap? It is not an illegal scam, but it is a highly calculated marketing trick reliant on human psychology.

- The Ultimate Bait: The flashy promise of zero finance car deals acts as a magnet to drive immense foot traffic to the dealership.

- Emotional Investment: Imagine a buyer named Mike. He takes a test drive, smells the new leather, and spends two hours mentally taking ownership of the car. He is fully emotionally invested.

- The Switch: In the finance office, the dealer runs Mike’s credit. Even with a solid 720 score, Mike is told the 0% offer is strictly reserved for “Super Prime” scores of 780 or higher.

- The Win: Mike is offered a standard 6% rate instead. Because he is already attached to the vehicle, he signs the paperwork. The marketing trick worked perfectly—they sold a car at 6% to a buyer who came in looking for 0%.

4. The Hidden Traps in the Fine Print

Even if you have a flawless credit score, there are hidden catches you need to be intensely aware of before signing.

- The Short-Term Squeeze: Dealerships heavily advertise zero finance car deals, but the microscopic fine print often dictates the loan is only valid for 36 months. Dividing a $40,000 vehicle by 36 months results in a crippling $1,100+ monthly payment.

- The Rebate Catch: You will frequently see “0% APR OR $3,000 Cash Back.” You cannot have both.

- The Math: If you take the 0% loan, you forfeit the cash rebate and pay the full sticker price (MSRP). Sometimes, taking the $3,000 upfront discount and securing a standard loan from your own bank actually saves you more money overall.

My Final Take on Zero Finance Car Deals

Getting approved for authentic zero finance car deals feels like a massive financial victory, but you must not let the euphoria of a 0% rate blind you to the larger economic picture.

- Negotiate First: Always aggressively negotiate the total out-the-door price of the vehicle as if you were paying cash. Only bring up financing after the price is locked in.

- Look at Total Costs: A cheap loan does not guarantee a cheap car to own. Factor in your auto insurance premiums before buying. Pulling comparative quotes from major providers like USAA, GEICO, State Farm, or Progressive is crucial, as a heavy monthly insurance bill on a new car can easily wipe out every dollar you saved on loan interest.

- Be Ready to Walk: Read the fine print, do the math, and have the sheer willpower to walk away if the dealer tries to pull an emotional bait-and-switch.

The Hidden Catch Behind zero finance car deals: Your Credit Score

- Most people hunting for zero finance car deals face a rude awakening when they sit down at the dealership’s finance desk: their credit score simply isn’t good enough to play the game.

- The “Super Prime” Requirement: Lenders offering zero finance car deals take zero profit on the interest. To offset this, they demand zero risk. This means they exclusively target “Super Prime” or Tier-1 borrowers who have virtually spotless financial histories.

- The Magic Number: While you might secure a standard auto loan with a 660 FICO score, you typically need a score of 750 or higher to qualify for top-tier promotional financing. Lenders also heavily weigh your FICO Auto Score, which specifically tracks your past history with car payments.

- The 720 Illusion: Many buyers walk into the showroom with a 720 score, assuming they have “good” credit and deserve the best rate. The reality? A 720 might easily secure you a mortgage, but “free money” in the auto world is reserved for the absolute best, not just the good.

- Beyond the Score: Even with a 780, your credit file must be immaculate. I’ve seen buyers get denied because of a high Debt-to-Income (DTI) ratio (over 40%) or a “thin file” (meaning they only have a year or two of credit history).

The Math Dilemma: zero finance car deals vs. Cash Rebates

- When buying a car, dealerships often force you into a corner: take the 0% APR, or take a massive upfront cash rebate and secure your own standard loan. You cannot have both.

- The Breakdown of a $30,000 Car: Let’s look at the math for a 60-month term.

- Option A (The 0% Route): You finance the full $30,000 at $500 a month. Your total cost out the door is exactly $30,000.

- Option B (The Rebate Route): You take a $3,500 cash rebate, dropping the car’s price to $26,500. You finance that smaller amount at a standard 5% APR. Your monthly payment is $500.09. Your total cost out the door is $30,005.

- The Shocking Reality: Despite paying 5% interest in Option B, the final out-of-pocket cost is nearly identical. The $3,500 upfront cash rebate completely offsets the $3,505 in interest you will pay over the five years

When to Skip the 0% Offer

- This specific math proves that zero finance car deals aren’t always the automatic “best” financial choice for your wallet.

- When Rebates Win: If the manufacturer offers a rebate larger than $3,500, or if you secure a rate lower than 5% from your local credit union, taking the cash discount is mathematically cheaper than the 0% offer.

- Selling Early: If you plan to trade the car in after just three years, taking the upfront cash rebate immediately lowers your loan principal. This protects you against negative equity (being “underwater” on the loan), making standard loans much safer in the short term than locking into zero finance car deals.

My Final Take

- The marketing behind zero finance car deals is brilliant because it acts as an emotional blinder, causing buyers to hyper-focus on the interest rate while forgetting about the total cost of the vehicle.

- Getting approved for 0% financing feels like a massive victory, but it is ultimately just a math equation. Never let a 0% rate distract you from negotiating the total out-the-door price of the car first.

- If you do have the elite 750+ credit score required to play the game, always run the amortization math on the cash rebate option before signing any paperwork. It might just save you thousands.

The Ultimate Blueprint to Scoring the Best zero finance car deals

- As an finance writer analyzing automotive financial trends, I’ve seen countless buyers walk into a dealership expecting to easily snag a 0% APR offer, only to leave frustrated and tied to a 7% loan.

- Securing true zero finance car deals is an exclusive privilege reserved for the most prepared buyers. If you’ve done the math and decided this is your path, here is my detailed, four-step battle plan to use before ever setting foot on a dealership lot.

Step 1: Master Your FICO Auto Score Months in Advance

- In the high-stakes arena of zero finance car deals, your credit score is your VIP pass. Never rely on the dealership to check your score for the first time.

- The 3-Month Rule: I always recommend pulling your credit report at least 90 days before car shopping. This gives you ample time to fix errors, dispute inaccuracies, or pay down debts.

- The 750+ Target: You need to be in the “Super Prime” tier. A standard 720 won’t cut it. Furthermore, auto lenders look specifically at your FICO Auto Score (often versions 8 or 9), which heavily weighs your past auto loan repayment history.

- My Pro Tip: If you are hovering around a 730, the fastest way to boost your score is to aggressively pay down your credit card balances to lower your ‘Credit Utilization Ratio’. For instance, if you have a $10,000 limit, paying the balance down to below $1,000 can cause an immediate and significant jump in your score, potentially pushing you over that magic 750 threshold.

Step 2: Become a Detective with the Fine Print

- Those massive TV commercials and giant dealership billboard banners are designed to create emotional urgency, not to give you the full truth.

- Skip the Ads, Go to the Source: Before hunting for zero finance car deals, ignore the dealership flyers and go straight to the “Offers & Incentives” page of the official automaker’s website (like Ford.com or Toyota.com).

- Watch the Clock: The biggest catch I see buyers fall for is the term length. The manufacturer’s website will explicitly state how long the 0% APR lasts. It is almost always capped at 36, 48, or a maximum of 60 months. If you walk in expecting an 84-month free loan, you will be deeply disappointed.

- Inventory Clear-Outs: Check the specific models and trims eligible for the offer. Automakers rarely offer 0% on their hottest, newly redesigned models. It is usually restricted to last year’s leftover inventory or less popular base trims that they desperately need to clear off the lot.

Step 3: Brace for the “Monthly Payment Shock”

- Here is a reality check I often share: while zero finance car deals save you thousands of dollars in interest, they almost guarantee a massive monthly payment.

- The Short-Term Math: Because captive lenders restrict 0% offers to shorter terms (like 36 to 48 months), you are forced to pay off the entire principal at a highly accelerated rate.

- Let’s break down a $30,000 car:

- Over 60 months: You pay exactly $500 per month.

- Over 48 months: It jumps to $625 per month.

- Over a strict 36-month term: You are looking at a heavy $833 per month.

- My Advice: Ask yourself honestly before leaving your house—can your household comfortably absorb an $800 monthly car payment without sacrificing your emergency funds or daily lifestyle? Being “car poor” just to save on loan interest is a terrible financial trade-off.

Step 4: Arm Yourself with the Pre-Approval “Shield”

- This is arguably my most critical piece of advice: never, ever walk into a showroom entirely dependent on the dealer to secure your financing.

- Get a Plan B: A few days before your dealership visit, apply for an auto loan at your local credit union or a bank where you have a long-standing relationship. Credit unions consistently offer some of the lowest standard rates in the country.

- Block the Bait-and-Switch: Imagine sitting in the finance office. The manager looks at his screen and says, “Unfortunately, your score didn’t qualify for the 0% APR, but I got you approved at 7.5%.” If you don’t have a backup plan, you might panic and accept it.

- The Power of Leverage: However, with your pre-approval letter in hand, you hold the ultimate power. You can simply reply, “If I don’t qualify for the zero finance car deals, I will just use this 4.5% approval I already secured from my credit union.” This instantly protects you from inflated dealer markups on interest rates.

My Final Take

- Securing these elusive zero finance car deals isn’t about getting lucky on a Saturday afternoon; it is about executing a precise, disciplined financial strategy.

- By bulletproofing your credit score ahead of time, dissecting the manufacturer’s fine print, ensuring your budget can handle heavy short-term payments, and walking in fully armed with a credit union pre-approval, you take all the power away from the dealership.

- You transform from a vulnerable buyer into a highly educated consumer, ready to claim the absolute best deal the automotive market has to offer.

The Unfiltered Truth About zero finance car deals: Pros, Cons, and Real-World Strategies

- Walking into a dealership with the promise of free money feels like you’ve already won the negotiation. But as an finance writer that analyzes financial markets and automotive economics, I have to give you the unvarnished truth: these offers are a double-edged sword. Let’s break down the actual pros and cons before you sign on the dotted line.

The Pros: When the Math Actually Works

- Absolute Zero Interest Cost: This is the ultimate dream. When you score legitimate zero finance car deals, you are essentially using the bank’s money for free. If you buy a $30,000 car, you pay exactly $30,000 over five years. The thousands of dollars you save can be invested elsewhere to actually build wealth.

- Rapid Equity Building: Cars are depreciating assets—they lose value the second you drive off the lot. With a standard loan, your early payments mostly cover the bank’s interest. But with zero finance car deals, 100% of your payment hits the principal from day one. You build equity much faster, drastically reducing the risk of becoming “underwater” (owing more than the car is worth).

The Cons: The Hidden Traps of “Free Money”

- The “Super Prime” Wall: As we covered, these promotions are locked behind a massive credit score wall. Roughly 85% of buyers walk in expecting free money and walk out with a standard 6% or 7% loan. It is a brilliant marketing magnet that most people simply don’t qualify for.

- Crippling Monthly Payments: Automakers rarely hand out free money for 72 or 84 months. They condense these loans into brutal 36- or 48-month terms. A $35,000 car on a 36-month zero-interest loan still means a suffocating $972 monthly payment. I constantly see buyers ruin their household budgets because they were blinded by the 0% rate.

- Inventory Dumping: You rarely get this offer on the car you actually want. Automakers don’t offer zero finance car deals on high-demand, newly launched hybrid SUVs. They slap this offer on last year’s leftover models or the weirdly colored sedans gathering dust on the back lot. You aren’t buying your dream car; you are buying the car the manufacturer is desperate to get rid of.

- Paying the Maximum MSRP: This is the silent killer of the transaction. The dealership will almost always make you choose: take the 0% rate OR take the $4,000 cash rebate. If you take the free interest, you forfeit the discount and pay the absolute maximum sticker price for the vehicle.

The Backup Plan: What to Do When zero finance car deals Fall Through

- Picture this: You are sitting in the Finance manager’s office. You’ve spent three hours falling in love with a car. The manager looks at his screen, sighs, and says, “Unfortunately, you didn’t qualify for the 0% rate, but I can get you 7.5%.” Do not panic, and do not sign. Here is your strategy:

- Pivot to the Cash Rebate: If the door to zero finance car deals slams shut, immediately change tactics. Tell the dealer, “Fine, I’ll pass on the 0%. I want the maximum cash rebate applied to the MSRP right now.” Lowering the principal balance by thousands upfront is incredibly powerful.

- Deploy Your Credit Union: This is where your preparation pays off. Use the pre-approval you smartly secured before arriving. Taking a large cash rebate from the dealer and combining it with a fair 4.5% rate from a non-profit credit union is mathematically cheaper in many scenarios than 0% financing at full MSRP.

- Look Beyond the Car Payment: When you are forced into a standard loan, your monthly budget gets tighter. This is exactly why you must factor in the complete cost of ownership. Before finalizing the car, pull comparative quotes from major providers like USAA, State Farm, GEICO, and Progressive. A slightly higher auto loan rate can often be perfectly offset by choosing a vehicle model that is historically cheaper to insure based on state-specific regulations.

- The CPO Cheat Code: Let’s face reality—true zero finance car deals only apply to brand-new cars that lose 20% of their value the moment tires hit the pavement. If you don’t get the 0% offer, walk away from the new car smell. Buy a 3-year-old Certified Pre-Owned (CPO) vehicle. It has already suffered its worst depreciation, and paying a standard interest rate on a car that costs 40% less is often the smartest financial move you can make.

My Final Take

- Ultimately, chasing zero finance car deals is a high-stakes financial game designed by brilliant marketers. It is not an illegal scam, but it is a psychological trap meant to get you onto the lot and emotionally invested in a vehicle.

- Never let the emotional thrill of a new car or the shiny promise of a 0% rate dictate your choices. Bring a calculator, compare the total out-the-door price with and without the cash rebate, evaluate your auto insurance impact, and be ready to walk away. The dealership’s goal is to maximize their profit; your goal is to protect your wealth.

The Reality and Recap of zero finance car deals

- Based on my ongoing analysis of the American auto financing market, the truth about 0% APR is fascinating. It is not a scam; it is an entirely legal contract. But it is a highly calculated “bait and switch” marketing gimmick surrounding zero finance car deals. Automakers use this magical “0%” number to drive massive foot traffic into their showrooms.

- The Harsh Reality: The dream sold on TV and billboards is exceptionally narrow. These exclusive offers are reserved strictly for the top 10% to 15% of buyers with “Super Prime” credit (typically a 750+ FICO score) and a flawless repayment history. For the vast majority of Americans, the 0% offer is simply the bait that eventually leads them to sign a standard, higher-interest loan.

- The Hidden Trade-offs: Even if you do qualify, free money comes with heavy strings attached. You are usually restricted to short loan terms (36 to 48 months), which results in massive, budget-straining monthly payments. More importantly, choosing 0% APR almost always means you have to forfeit lucrative cash rebates, forcing you to pay the absolute maximum sticker price (MSRP) for the vehicle.

The Truth About 0% APR: Are zero finance car deals a Marketing Trick?

- Just last weekend, my neighbor Mark was ecstatic. He saw a massive billboard advertising zero finance car deals, like “0% APR Financing for 60 Months!” on a brand-new SUV. He genuinely believed he was going to buy a car without paying a single extra dollar to the bank.

- But as an Finance Writer who constantly monitors the auto financing market—where the current national average interest rate for a new car is hovering stubbornly around 6.5% to 7%—I had to give him a harsh reality check.

- There is an old saying in the financial world: “If something sounds too good to be true, there is probably a catch.” Have car dealerships suddenly become charities giving away free money? Absolutely not. Let’s uncover the reality behind these advertisements.

The “Bait” in the Showroom

- Let’s be completely clear: the concept of zero finance car deals is not an illegal scam. If you somehow jump through every single financial hoop perfectly, you truly won’t pay a dime in interest.

- However, it is arguably the most effective “bait and switch” marketing gimmick in the American automotive industry.

- Automakers and their captive finance companies use that magical “0%” number as a giant magnet. Their primary goal is simple: get you off your couch, onto their lot, and emotionally attached to the new car smell during a test drive.

The Hidden Strings Attached

The Ultimate Sacrifice: You almost always have to forfeit massive cash rebates. The dealer will force you to make a painful choice: take the 0% rate, OR take the $3,000 cash discount. You can never have both, meaning you are forced to pay the absolute maximum sticker price (MSRP) for the vehicle.

When Mark finally sat down in the dealership’s finance office, the illusion shattered. Here is what those flashy TV commercials conveniently leave out:

The Elite Credit Wall: Free money is reserved strictly for “Super Prime” borrowers. If your FICO auto score isn’t north of 750 with a flawless, years-long payment history, you will be swiftly denied. The dealer will then capitalize on your emotional attachment to the car and immediately offer you a standard 7% loan instead.

The Payment Shock: Manufacturers rarely give you a comfortable 72 months to pay off an interest-free loan. They condense these offers into brutal 36- or 48-month terms. Dividing a $40,000 vehicle by 36 months results in a suffocating $1,100+ monthly payment that can easily ruin an average household budget.

10 Quick Takeaways: Mastering the Deal

- 1. APR vs. Interest Rate: The interest rate is just the basic base cost of borrowing money. APR (Annual Percentage Rate) is the total annual cost, which includes hidden processing fees and underwriting charges. When you secure authentic zero finance car deals, both the interest rate and those sneaky administrative finance charges drop to absolute zero.

- 2. Why Banks Tap Out: Traditional banks (like Chase or Wells Fargo) make their profit by charging interest. Loaning money for free is a guaranteed financial loss for them due to inflation and overhead expenses, which is why they never fund zero finance car deals.

- 3. The Role of Captive Lenders: These 0% loans come exclusively from “Captive Finance Companies”—the in-house banks of automakers (like Toyota Financial Services or Ford Motor Credit). Their primary goal isn’t to make money on the loan itself; it’s to move metal and clear out aging inventory. The automaker subsidizes the lost interest to guarantee the sale of the car.

- 4. The “Bait and Switch” Tactic: Dealerships aggressively advertise 0% APR to act as bait. When 85% of customers inevitably fail to qualify due to strict credit requirements, the dealer “switches” them to a highly profitable 6% or 7% standard loan, capitalizing on the buyer’s emotional attachment to the car.

- 5. The FICO Requirement: A “Super Prime” score of 750+ is mandatory. But the score alone isn’t enough; lenders manually underwrite your file. A single late payment in the last five to seven years, a past bankruptcy, a “thin” credit file, or a high Debt-to-Income (DTI) ratio will trigger an immediate rejection.

- 6. The Payment Shock: These loans are condensed into short 36- to 48-month terms. Because you are paying off a $35,000+ depreciating asset in just three or four years, your monthly payment will often skyrocket past $800, creating massive strain on an average household budget.

- 7. The Ultimate Ultimatum: You cannot stack financial discounts. The automaker forces you to choose: either take the subsidized 0% loan, OR take a massive cash rebate off the car’s price. You can never have both at the same time.

- 8. The Math of the Cash Rebate: How can a 5% loan be cheaper than a 0% loan? It all comes down to amortization. If taking a $4,000 cash rebate lowers your principal loan amount significantly from day one, the total 5% interest you pay over five years might only be $3,500. The rebate completely offsets the interest, making it mathematically cheaper than paying full MSRP for zero finance car deals.

- 9. Pros and Cons Summarized:

- Pros: You save thousands of dollars in absolute interest costs, and 100% of your monthly payment hits the principal from day one, building your equity incredibly fast and protecting you from being “underwater.”

- Cons: It is practically impossible for the average buyer to qualify, you are burdened with high monthly payments, and by forfeiting the cash rebate, you pay the absolute maximum sticker price for a vehicle the manufacturer is desperately trying to clear out.

- 10. Your Backup Plan: If you get denied for zero finance car deals in the finance office, do not panic and do not accept their first counter-offer. Immediately ask to apply the maximum cash rebate to the car’s price. Then, use a pre-approved, low-interest loan you already secured from your local credit union. Alternatively, skip the massive new-car depreciation hit entirely and buy a 3-year-old Certified Pre-Owned (CPO) vehicle.

My Final Take

- As an finance writer, I don’t feel the rush of the “new car smell” or the emotional attachment of a test drive, which makes it easy for me to see the cold, hard numbers. A dealership’s primary goal is to maximize their profit, and it is entirely your responsibility to protect your wallet.

- Never make an emotional purchase based solely on the flashy allure of “free money.” Buying a vehicle must be a strictly mathematical operation where you compare the total “out-the-door” costs of every scenario.

- Ultimately, snagging genuine zero finance car deals requires impeccable timing, flawless credit, and the budget to handle aggressive, short-term monthly payments.

- If the math doesn’t work in your favor, be fully prepared to walk away. Taking a hefty cash rebate upfront and securing a standard rate from a local credit union is often the smartest financial decision you can make, proving that zero finance car deals aren’t the only way to win at the dealership.