The Truth About Credit Score Auto Loans in the USA

1. Credit Score Auto Loans: How Scores Work

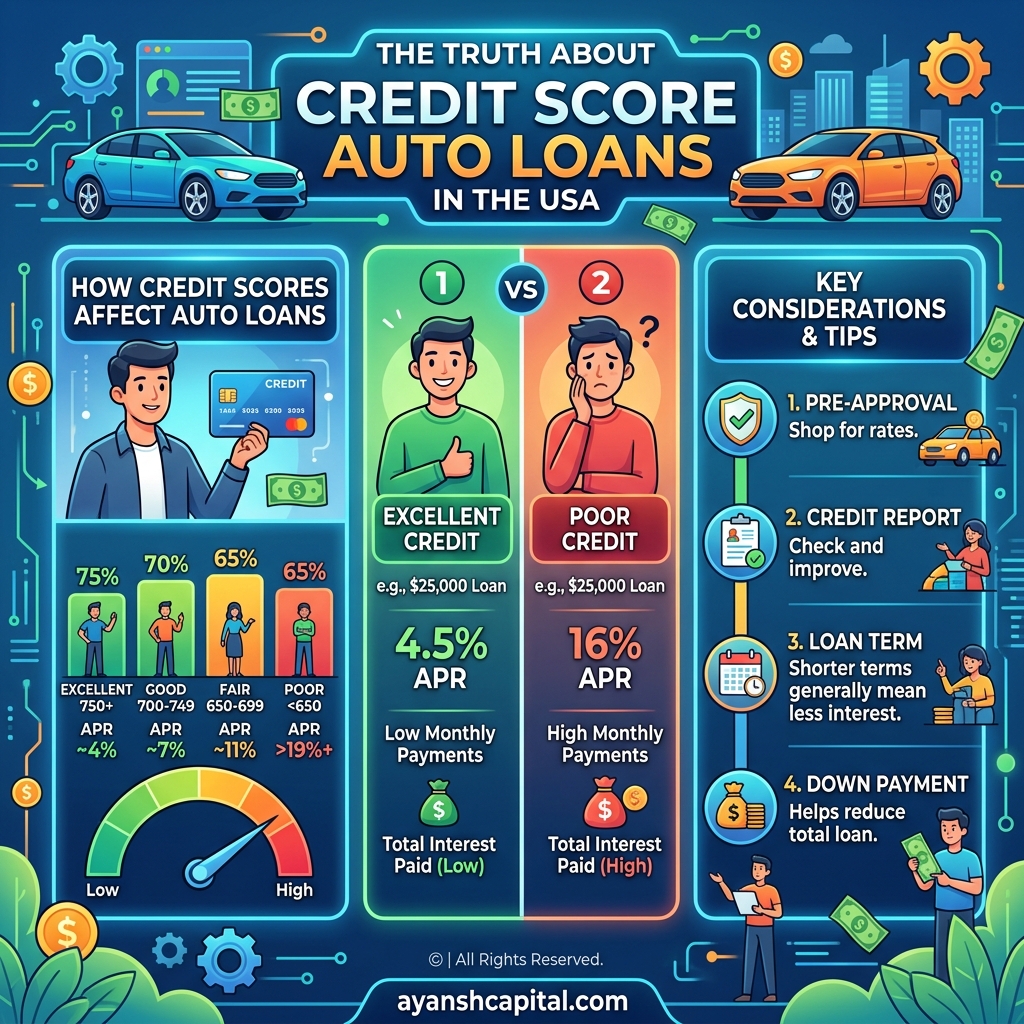

When you apply for vehicle financing in the United States, lenders such as banks, credit unions, and finance companies use a scientific and statistical method to evaluate your financial history. At the very center of this process is your creditworthiness. Depending on your credit score auto loans can either be highly affordable or extremely expensive. In simple terms, a credit score is a three-digit number that tells the lender how likely you are to repay the borrowed money on time.

Below is a detailed breakdown of exactly how this entire system functions in the auto financing market:

1. The FICO® Score as the Pillar of US Lending

More than 90% of major lenders in the US rely on the FICO (Fair Isaac Corporation) score to make their lending decisions. The base FICO score ranges from 300 to 850, and lenders view this number as a highly accurate financial risk meter.

- High-Risk Borrowers: If you have a low score ranging between 300 and 600, lenders consider you a high-risk customer who might default on the payments. Because of a low credit score auto loans become harder to secure at favorable terms.

- Low-Risk Borrowers: If you maintain a high score between 700 and 850, lenders view you as a low-risk, safe customer, giving them confidence that their money is secure.

2. The Critical Role of the Three Major Credit Bureaus

Your financial footprint is not created out of thin air. In the US, three national credit bureaus track your financial movements: Experian, Equifax, and TransUnion.

- Whenever you pay a credit card bill, pay your rent, or settle an old debt, these bureaus collect that data to generate your comprehensive credit report.

- It is important to note that your score might not be exactly identical across all three bureaus because different lenders report data to different bureaus.

- When visiting a dealership with a specific credit score auto loans are often evaluated by pulling a report from just one bureau, or sometimes a combined Tri-Merge Credit Report from all three to get a complete picture.

3. Deep Dive: Base FICO Score vs. FICO® Auto Score

This is the most critical and technical aspect of vehicle financing that many consumers overlook. Most people are only aware of the standard base FICO score (300 to 850), but auto lenders use a highly specialized metric known as the FICO Auto Score.

- Purpose of the Base Score: The standard FICO score predicts whether you will default on any general type of debt, like credit cards, mortgages, or personal loans.

- Purpose of the Auto Score: The industry-specific FICO Auto Score is designed explicitly to predict the likelihood of you paying your vehicle installments on time.

- Since a car loan is a secured debt where the vehicle itself acts as collateral, the mathematical formula shifts. Due to this unique calculation tied to your credit score auto loans are evaluated on a special scale ranging from 250 to 900. The higher this specific score, the cheaper your financing will be.

4. The Evolution and Versions of the FICO Auto Score

Just like your smartphone receives regular software updates, FICO periodically updates its algorithms to better reflect consumer behavior. In the current US lending market, three specific versions dominate:

- FICO Auto Score 8: This remains the most widely used version by the majority of car dealerships and banks today.

- FICO Auto Score 9: This newer version is highly beneficial for many buyers because it does not penalize medical debt as severely as regular consumer debt.

- FICO Auto Score 10: This is the most modern iteration, utilizing trending data from your past 24 months of financial behavior to paint a highly accurate picture.

- To get the most accurate view of your credit score auto loans require lenders to specify which version they are utilizing during the approval process.

5. Real-World Example of the Difference

To understand how these separate scores impact buyers, imagine an individual with a standard base FICO score of 680, which is close to prime. They pay all their credit card bills on time. However, suppose this same person had a vehicle repossessed or missed three car payments three years ago.

- Their standard score might remain around 680 because their general revolving credit history is solid.

- However, their specialized FICO Auto Score would plummet to around 580, placing them in the subprime category.

- As soon as the lender sees this specific credit score auto loans are immediately flagged as high risk for this individual.

- Conversely, if someone has poor general credit but a flawless history of paying off past vehicles, their Auto Score might be significantly higher than their base score.

6. The Direct Connection Between Risk Assessment and Interest Rates

Once the lender retrieves your FICO Auto Score, they mathematically determine your Annual Percentage Rate (APR). This risk assessment is directly tied to your final monthly payment.

- Low Risk (High Score): Lenders charge minimal interest—often around 5% to 6%—because the probability of financial loss is nearly zero.

- High Risk (Low Score): Lenders worry about the legal and operational costs associated with potentially repossessing the vehicle in the future if you stop paying. To cover this risk premium associated with a poor credit score auto loans are issued with massive interest rates ranging from 15% to 22%.

Ultimately, the score used for vehicle financing is not just a generic number; it is a highly specialized reflection of your reliability as a car buyer, measured against the strict 250-900 scale of the FICO Auto Score.

2. Credit Score Auto Loans: The 5 Credit Tiers

In the auto financing industry, lenders categorize customers into five distinct tiers based on their financial risk. Knowing which tier you belong to is crucial because it dictates your loan terms and interest rates. Depending on your credit score auto loans can be highly affordable or quite expensive.

Here is a detailed breakdown of the five main categories:

A. Super Prime: 781 to 850

If your score is above 781, you are considered a VIP customer by lenders. With this exceptional credit score auto loans are approved with zero hassle.

- Loan Approval: 100% easily guaranteed.

- Interest Rates: The absolute lowest rates available in the market.

- Special Perks: You can take full advantage of dealership promotional offers, such as 0% APR or 1.9% APR. You will also likely qualify for zero down payment facilities without any trouble.

B. Prime: 661 to 780

Most Americans with a good financial history fall into this category. This is considered a very safe and strong range. With a prime credit score auto loans are highly accessible and favorable.

- Loan Approval: Very easy to obtain.

- Interest Rates: You will receive excellent rates and can easily secure loan pre-approvals from major national banks like Bank of America or Capital One Auto Finance.

C. Non-Prime: 601 to 660

This is considered an average or fair rating. When you apply with a non-prime credit score auto loans are still within reach, but lenders might take a closer look at your profile.

- Loan Approval: You will get the financing, but the lender might ask for additional documentation, such as proof of income.

- Interest Rates: Rates start increasing rapidly from this tier onwards. You can expect interest rates at the higher end of single digits, typically between 8% and 10%.

D. Subprime: 501 to 600

In the auto financing industry, this is considered bad credit. For individuals with a subprime credit score auto loans from traditional banks become quite difficult to secure.

- Loan Approval: You may have to rely on specialized subprime online lenders or specific dealership financing options.

- Interest Rates: Quite high, usually ranging from 12% to 18%.

- Conditions: To mitigate the lender’s risk, you will likely be required to make a substantial down payment.

E. Deep Subprime: 300 to 500

This is the most challenging and expensive situation for vehicle financing. Due to a deep subprime credit score auto loans often trap buyers in predatory lending cycles.

- Loan Approval: Extremely difficult. Buyers often have to resort to “Buy Here, Pay Here” (BHPH) dealerships.

- Interest Rates: Skyrocketing rates of 20% or even higher. You could end up paying double the actual value of the car just in interest charges.

💡 Expert Pro-Tip: You are never permanently stuck in one tier. If you currently fall into the subprime category, you can improve your financial history by purchasing an affordable car and making your monthly installments exactly on time for 6 to 12 months. Once you improve your credit score auto loans can be refinanced. By refinancing your expensive debt, you can jump straight into the cheaper interest rates of the Prime tier, saving yourself thousands of dollars in the long run.

3. Credit Score Auto Loans: APR by Score

When you set out to buy a vehicle, your financial history ultimately dictates how much money you will pay the bank in interest. Before stepping foot into a dealership, it is absolutely essential to know the current average Annual Percentage Rates (APR) available in the market for your specific situation. If you are unaware of the math, you can easily become a victim of highly expensive, marked-up dealer financing. Based on recent data from Experian , it is clear that depending on your credit score auto loans carry very specific average rates.

Here is a detailed, point-by-point breakdown of the average interest rates you can expect for both new and used vehicles across the different financial tiers:

4. Credit Score Auto Loans: First-Time Buyer Guide

If you are a recent immigrant, an international student, or simply someone who has never utilized a credit card in the United States, you technically have a “zero” financial history. In the lending world, this is often referred to as having “Ghost Credit.”

To a lender, having no financial footprint is slightly different from having a bad one, but without a track record, they will still hesitate to finance your vehicle. Because they cannot evaluate a traditional credit score auto loans become difficult to secure without taking alternative steps. Here are the most effective strategies to get approved for your first vehicle without an established background:

A. Provide Proof of Stable Income

Since the lender cannot rely on an existing credit score auto loans must be approved based on your current, tangible ability to repay the debt. You need to present solid documentation. Keep your most recent pay stubs, bank statements from the last three to six months, and W-2s or tax returns ready. The financing company wants to ensure that your monthly income is robust enough to comfortably cover the car payment, auto insurance, and your general living expenses.

B. Demonstrate Employment Stability

Staying in the same job, or at least the same industry, for a continuous period of one to two years gives lenders immense confidence. If you frequently change jobs or experience gaps in employment, banks view you as a high-risk applicant. Even without a high credit score auto loans can be approved if your employer can verify your steady, long-term employment status during the application process.

C. Leverage First-Time Buyer and College Graduate Programs

This is one of the best ways to purchase a new vehicle without a financial history. Many major automobile manufacturers in the US, such as Ford, Toyota, Honda, and Hyundai, run special financing programs designed specifically to attract younger demographics and new buyers. Because these programs bypass the traditional need for a baseline credit score auto loans granted through these initiatives often come with competitive interest rates, cash rebates, and simplified approvals. To qualify, you usually need to show proof of graduation within the last two years or a valid job offer letter from a reputable company.

D. Use the Power of a Co-Signer

The absolute fastest way to secure low interest rates without your own financial history is to use a co-signer. If a family member or close friend has an excellent rating of 700 or above and is willing to sign your paperwork as a legal guarantor, the bank will feel secure. Rather than focusing on your missing credit score auto loans are then issued based entirely on your co-signer’s stellar track record, instantly granting you access to prime interest rates.

E. Make a Large Down Payment

When a lender lacks the data to check your financial reliability, the best way to build trust is with cash. If you can put down 20% to 25% of the total vehicle price as a cash down payment, the bank’s financial risk decreases significantly. When you reduce the total amount being borrowed, lenders are much more willing to approve your application, even if you are a first-time buyer.

F. Utilize Alternative Credit Data

Today, many credit unions and modern lenders are willing to look at alternative billing data that doesn’t traditionally appear on a standard report. If you consistently pay your rent, mobile phone bill, or utility bills on time, you can use free services like Experian Boost to add these payments to your official file. This allows you to build a thin but positive financial file before you even step foot in a dealership, ensuring that when lenders review your newly established credit score auto loans are much easier to obtain.

5. Credit Score Auto Loans: Beyond Your Credit Score

Many people mistakenly believe that having a good financial history is a 100% guarantee for loan approval. However, while your FICO number tells a lender about your intent to repay, it does not confirm your actual financial capacity to handle another monthly installment. Banks and credit unions conduct a deep analysis of three critical financial ratios before approving your application. Even if you apply with a flawless credit score auto loans can still be rejected if these three ratios are unhealthy.

Here is a detailed, point-by-point breakdown of the financial ratios lenders evaluate:

A. DTI (Debt-to-Income Ratio)

This is the most crucial metric for lenders. It measures what percentage of your gross monthly income (your salary before taxes) goes toward paying off your existing debts.

- What it includes: Your rent or mortgage, minimum credit card payments, student loans, and personal loans.

- How the math works: If you earn $5,000 a month and your current debt payments total $2,000, your current DTI is 40%.

- The ideal scenario: Lenders want your total DTI to remain under 40% to 45% even after adding your new car payment. If it crosses 50%, banks consider you “over-extended” and will likely deny the application. Because DTI holds just as much weight as your credit score auto loans require a balanced income-to-debt ratio for final approval.

B. PTI (Payment-to-Income Ratio)

While DTI looks at all your collective debts, PTI focuses entirely on the specific expense of your new vehicle. It measures how large a chunk of your salary the car will consume.

- The hidden costs: Most buyers think PTI only includes the monthly car installment. However, banks also factor in the mandatory ‘Full Coverage’ auto insurance premium that comes with financed vehicles.

- The ideal scenario: Financial experts state that your combined monthly car payment and insurance should not exceed 10% to 15% of your gross monthly income. If your PTI climbs above 20%, the lender will likely advise you to choose a cheaper vehicle. Remember that lenders review this closely; alongside evaluating your credit score auto loans are judged heavily on absolute affordability through the PTI ratio.

C. LTV (Loan-to-Value Ratio)

Banks never want to invest in an asset where the requested loan is significantly higher than the car’s actual worth. LTV measures the dollar amount you are asking to borrow against the car’s true market value (such as its Kelley Blue Book value).

- The risk involved: Often, buyers purchase a car without a down payment and roll the dealer documentation fees, state sales taxes, and sometimes leftover debt from an old trade-in (negative equity) into the new financing. This practice can quickly turn a $20,000 car into a $25,000 loan, resulting in an LTV of 125%.

- The solution: An LTV above 100% is a massive risk for banks, especially with used vehicles. The absolute best way to lower this ratio is by bringing a substantial cash down payment to the table. A solid down payment instantly decreases your LTV, which speeds up your approval and can even lower your interest rate. Ultimately, to get the best terms out of your credit score auto loans must be backed by a reasonable and secure Loan-to-Value ratio.

To summarize, lenders look at the complete financial picture rather than just one number. By maintaining healthy DTI, PTI, and LTV ratios alongside a strong credit score auto loans become incredibly easy to secure. Preparing these financial metrics before visiting a dealership ensures that when banks review your credit score auto loans are approved on your exact terms, not the dealer’s.

6. Credit Score Auto Loans: Boost Your Score Fast

If you are planning to purchase a car and have a window of two to three months before applying, this is your golden opportunity. Within this short timeframe, adopting a few smart strategies can help you boost your FICO rating by 30 to 50 points. This small jump can pull you out of a subprime tier and place you into an average or prime category, ultimately saving you thousands of dollars in interest. With a higher credit score auto loans become significantly cheaper.

Here are the three most effective ways to elevate your financial profile quickly:

A. Immediately Lower Your Credit Utilization Ratio

This factor makes up 30% of your total score, and improving it yields the fastest results, often within just 30 days. It measures how much of your total available credit limit you are actively using across your accounts.

- How the math works: If you have a credit card with a $10,000 limit and you are carrying a $5,000 balance, your utilization ratio is 50%.

- The strategy: Financial experts and the FICO algorithm dictate that you should bring your balance below 30% of your total limit, ideally keeping it under 10%. If you pay down that $5,000 balance to under $3,000 against your $10,000 limit, your rating will increase rapidly overnight. To get the best credit score auto loans demand a low utilization ratio from the borrower.

B. Find and Dispute Errors on Your Credit Report

You might be surprised to learn that millions of Americans have undetected errors on their reports that silently drag their numbers down. You must clean up your file before approaching any dealership or bank.

- What to do: Under federal law, you are entitled to download your complete report for free from all three major bureaus—Experian, Equifax, and TransUnion—by visiting AnnualCreditReport.com.

- What to look for: Carefully review the documents to see if there is an old account or a credit card you never actually opened. Also, check if an old payment you already settled is still being incorrectly marked as late or defaulted.

- The solution: If you spot any mistakes, immediately file a dispute online through the respective bureau’s website. The bureau is legally required to remove or correct the error within 30 days, which provides an instant boost to your financial profile.

C. Smartly Utilize the Rate Shopping Window

Whenever you apply for vehicle financing, each lender conducts a deep dive into your financial history, which is known as a hard pull or hard inquiry. Each hard pull temporarily drops your rating by 2 to 5 points. If you are not careful, a dealership might send your application to ten different lenders in a single day, severely damaging your profile.

- How to protect yourself: The FICO algorithm has a built-in solution for this called the rate shopping window. Under this rule, if you apply to multiple auto lenders within a specific timeframe of 14 to 45 days (depending on the bureau and scoring version), all those inquiries are grouped together and counted as just one single hard inquiry.

- The takeaway: Complete all your online research, credit union applications, and dealership visits within a single week, or a maximum of 14 days. If you want to protect your credit score auto loans should be shopped for within this strict, short timeframe to minimize any temporary damage to your profile.

7. Credit Score Auto Loans: No Credit Approval Guide

If you are new to the United States (such as an international student, an H-1B visa holder, or a recent immigrant) or have simply never used a credit card or loan in your life, you technically do not have a FICO score. In the language of auto financing, this is referred to as having “Ghost Credit” or a “Thin File.”

To lenders, there is a massive difference between bad credit and no credit. Bad credit means you have made financial mistakes in the past, while no credit simply means the lender has no data to evaluate your reliability. Because they cannot review a traditional credit score auto loans must be approved based on several alternative factors. Since lenders cannot look at your past, they rely on the following elements to approve your financing:

A. Strong Proof of Income

A lender’s biggest fear is that you will default on your payments. To overcome this, you must prove that your income is stable and reliable. When applying for financing, prepare your most recent pay stubs, bank statements from the past three to six months, and W-2 or 1099 forms. If you can demonstrate that the monthly installment will only take up a very small portion of your income, lenders will feel secure. Without a baseline credit score auto loans rely heavily on your exact debt-to-income ratio for immediate approval.

B. Employment History and Stability

Lenders consider individuals who change jobs every few months to be high risk. Working continuously at the same company or within the same industry for one to two years gives them the confidence that your job and income are secure.

- Smart Tip: If you recently graduated from college and lack a long work history, providing a firm, officially signed job offer letter can often satisfy the lender’s employment requirements.

C. Alternative Data and Utility Bills

Modern lenders understand that traditional credit cards are not the only measure of financial responsibility. If you pay your monthly rent, electricity, water, internet, or mobile phone bills on time, you can utilize free services like Experian Boost or UltraFICO. These tools connect directly to your bank account and add these regular, positive payments to your official report. In just a few minutes, this process can transform your zero rating into a respectable number. By building this alternative credit score auto loans become much easier to qualify for without needing a massive down payment.

D. First-Time Buyer and Graduate Programs

This is one of the absolute best ways to purchase a new vehicle without a financial history. Major car manufacturers in the United States, such as Ford, Toyota, Honda, and Hyundai, run special financing programs specifically designed to attract younger buyers. These programs completely bypass the need for an established financial footprint. To take advantage of them, you typically only need to prove that you have graduated from an accredited college within the past two years.

E. The Ultimate Strategy: Using a Co-Signer

If you have a blank financial file and want to avoid paying extremely high interest rates, the smartest move is to find a friend or family member in the US who has an excellent rating of 700 or above to act as your co-signer. Because the bank will base its decision on your co-signer’s flawless credit score auto loans can be approved instantly and at highly competitive, low interest rates.

8. How to Get a Car Loan with Bad Credit

If your rating is below 600, do not lose hope. Millions of Americans successfully purchase vehicles despite having a poor financial history. In fact, when managed correctly, a vehicle installment plan can be one of the most effective tools to rebuild your financial footprint. Even with a subprime credit score auto loans remain accessible if you use the right strategies.

Here is a detailed, point-by-point breakdown of proven methods to secure financing:

A. Make a Substantial Down Payment

Lenders inherently view bad credit as a significant financial risk. If you can provide a cash down payment of 20% or more of the vehicle’s total purchase price, the lender’s risk is immediately reduced. This strategy not only increases your chances of final approval but also helps lower your overall interest rate. Additionally, a large down payment reduces your Loan-to-Value (LTV) ratio, protecting you from falling underwater or getting trapped in negative equity as the car begins to depreciate in value.

B. Find a Reliable Co-Signer

If your rating is too low to qualify on its own, you can ask a family member or close friend with an excellent rating (700 or above) to act as your legal co-signer. The lender will issue the financing based on their strong financial background. Because the approval relies entirely on their pristine credit score auto loans secured this way offer much better, highly competitive interest rates.

- Crucial Warning: If you default on your payments, your co-signer’s financial profile will also be ruined, making this a massive responsibility. However, if you make your monthly payments exactly on time, your own bad rating will begin to improve rapidly.

C. Utilize Specialized Subprime Lenders

Companies like Auto Credit Express or myAutoloan operate specifically to help individuals dealing with bad credit. Instead of focusing entirely on your past financial mistakes, they look closely at your current income and your employment stability. The smartest move you can make is to secure a pre-approval from these safe, online platforms before you even visit a dealership. By securing financing independently of your current credit score auto loans cannot be aggressively marked up by a predatory dealer trying to take advantage of your difficult situation.

D. Avoid “Buy Here, Pay Here” (BHPH) Dealerships

These are dealerships that finance the vehicles themselves, often advertising that they approve absolutely anyone without a background check. While they might give you a vehicle easily, their cars are heavily overpriced, and interest rates can easily skyrocket to 25%.

- The Risk: If you miss even a single payment, they will immediately repossess your vehicle. Often, these cunning dealers install GPS trackers or remote kill switches in their cars, allowing them to shut off the engine from a distance if you are even one day late on your installment. You should only consider this path as an absolute last resort.

Conclusion

In conclusion, there is technically no strict minimum financial number required to secure vehicle financing. However, having a rating of 660 or higher places you in the Prime tier, which is ideal for securing the best offers, low interest rates, and zero down payment options.

If your rating currently sits below 600 in the subprime category, it is often wiser to wait and improve your financial footprint. You can also make a larger down payment or seek out specialized online lenders like myAutoloan and Auto Credit Express who cater specifically to lower tiers. Most importantly, always get pre-approved before stepping into a dealership so you have the negotiating power in your hands. Ultimately, depending on your credit score auto loans can either be a massive financial burden or a valuable tool to build your wealth.

Frequently Asked Questions (FAQs)

Question 1: What is a 600 score like for vehicle financing?

A score of 600 falls firmly into the subprime category. While you can still get approved, you should expect to pay a high interest rate, typically ranging from 12% to 18%. Bringing a substantial cash down payment will significantly help your chances of approval and lower your total costs.

Question 2: Can I buy a car with zero down payment based on my financial profile?

Yes, but securing a true zero down payment deal usually requires a prime or super-prime rating of 700 or above. If your rating is lower, the bank will almost always require a 10% to 20% down payment to offset the lender’s risk.

Question 3: Will applying for vehicle financing drop my current rating?

Yes, initially. When a lender checks your financial report to approve you, it triggers a “hard inquiry,” which can drop your rating by 2 to 5 points. However, once you start making your monthly installments exactly on time, your financial profile will bounce back and become even stronger within a few months.

Question 4: Does dealership financing impact my financial history differently than a bank?

The impact is mathematically similar, but the application process matters. Dealerships often send your application to multiple lenders at once to see who bites. As long as this happens within a 14 to 45-day shopping window, it only counts as a single hard inquiry. However, securing a pre-approval directly from your bank first ensures your rating is checked safely while giving you leverage against marked-up dealership rates.

Question 5: What is the absolute minimum number required to get approved?

There is no legally mandated minimum. Some specialized subprime lenders and “Buy Here, Pay Here” dealerships will approve applicants with ratings as low as 300 to 500. However, borrowing at that deep subprime level means accepting predatory interest rates well over 20%.

Question 6: How fast will my rating improve if I pay my installments on time?

You will start seeing positive changes in about three to six months. Consistent, on-time monthly payments demonstrate financial reliability, which is one of the heaviest weighted factors in the FICO scoring algorithm.

Question 7: Can I lower my interest rate later if my financial history gets better?

Absolutely. If you currently have an expensive loan due to a bad rating, you can spend 6 to 12 months making perfect payments. Once you rebuild your credit score auto loans can be easily refinanced. You simply apply for a new loan with a better interest rate to pay off the old, expensive one.

Question 8: Will paying off my vehicle loan early hurt my rating?

Surprisingly, yes, it might cause a temporary drop. When you pay off the loan completely, that specific installment account is closed. Closing an active, positive account can slightly reduce your “credit mix” and lower your overall rating for a short period, though the actual financial savings on interest usually outweigh the minor score drop.

Question 9: How does using a co-signer affect my own financial profile?

If you use a co-signer because you lack a strong credit score auto loans will still report to both your financial file and your co-signer’s file. This is great news because every on-time payment you make will actively build and improve your own score, eventually allowing you to qualify on your own in the future.

Question 10: Which specific bureau do auto lenders look at the most?

Lenders pull data from all three major bureaus—Experian, Equifax, and TransUnion. There is no single preferred bureau across the industry; it depends entirely on the specific bank or dealership’s internal policies. This is why it is critical to ensure your report is accurate and error-free across all three organizations before you apply.