Credit Score for Car Loan: Get Approved with Bad Credit

How to Get a Car Loan in the USA with Bad Credit

In the United States, it is difficult to imagine daily life without a car. Whether commuting to work, taking children to school, or running errands, having a reliable vehicle is essential. However, if your Credit Score for Car Loan is low, securing auto financing can be challenging. Lenders use your Credit Score for Car Loan as a key indicator of financial responsibility, and a lower score may result in higher interest rates, stricter loan terms, or fewer financing options.

That said, a poor credit score does not mean you cannot qualify for a car loan. With the right strategy, accurate information, and proper preparation, you can improve your chances of approval, find suitable lenders, and even take steps to strengthen your credit profile for future borrowing opportunities.

The Mathematics of Credit Scores and Their Impact on Auto Loans

In the United States, auto financing is heavily dependent on your credit history. However, it is important to understand exactly how lenders evaluate this data and how it directly dictates the overall cost of your vehicle.

Understanding the FICO Auto Score When reviewing your application, most auto lenders in the US do not just look at a standard Credit Score for Car Loan; they rely specifically on the FICO Auto Score.

- The Range: This specialized score ranges from 250 to 900.

- The Purpose: Unlike a general Credit Score for Car Loan, the FICO Auto Score is tailored to measure how you have managed auto loans in the past. It is specifically designed to predict the likelihood of you repaying a vehicle loan.

Credit Tiers and Interest Rates (APR) When you apply for a car loan, lenders evaluate your FICO Auto Score and place you into a specific “Credit Tier.” Your assigned tier determines the Annual Percentage Rate (APR) you will be offered based on your Credit Score for Car Loan. A lower score indicates a higher risk for the lender, which translates into a significantly higher interest rate for the borrower.

Here is a detailed breakdown of how your credit tier affects the average APR for both new and used vehicles:

The Financial Reality: Why This Math Matters To truly grasp the impact of these numbers, consider the severe financial consequences of purchasing a vehicle while falling into the lowest tier of a Credit Score for Car Loan.

- The Scenario: Imagine you are categorized in the Deep Subprime tier (score between 300 and 500).

- The Purchase: You decide to finance a used car with a principal amount of $20,000.

- The Terms: Because of your credit tier, you are assigned an APR of 21% on a standard 60-month (5-year) loan term.

The Outcome: Under these conditions, you will end up paying approximately $12,000 in extra interest alone over the life of the loan. This means your $20,000 used car will actually cost you around $32,000 by the time you make your final payment. This staggering extra cost highlights exactly why understanding credit tiers and adopting the right borrowing strategy for your Credit Score for Car Loan is absolutely crucial for a subprime borrower.

Credit Score for Car Loan: The Complete Roadmap to Auto Loan Approval

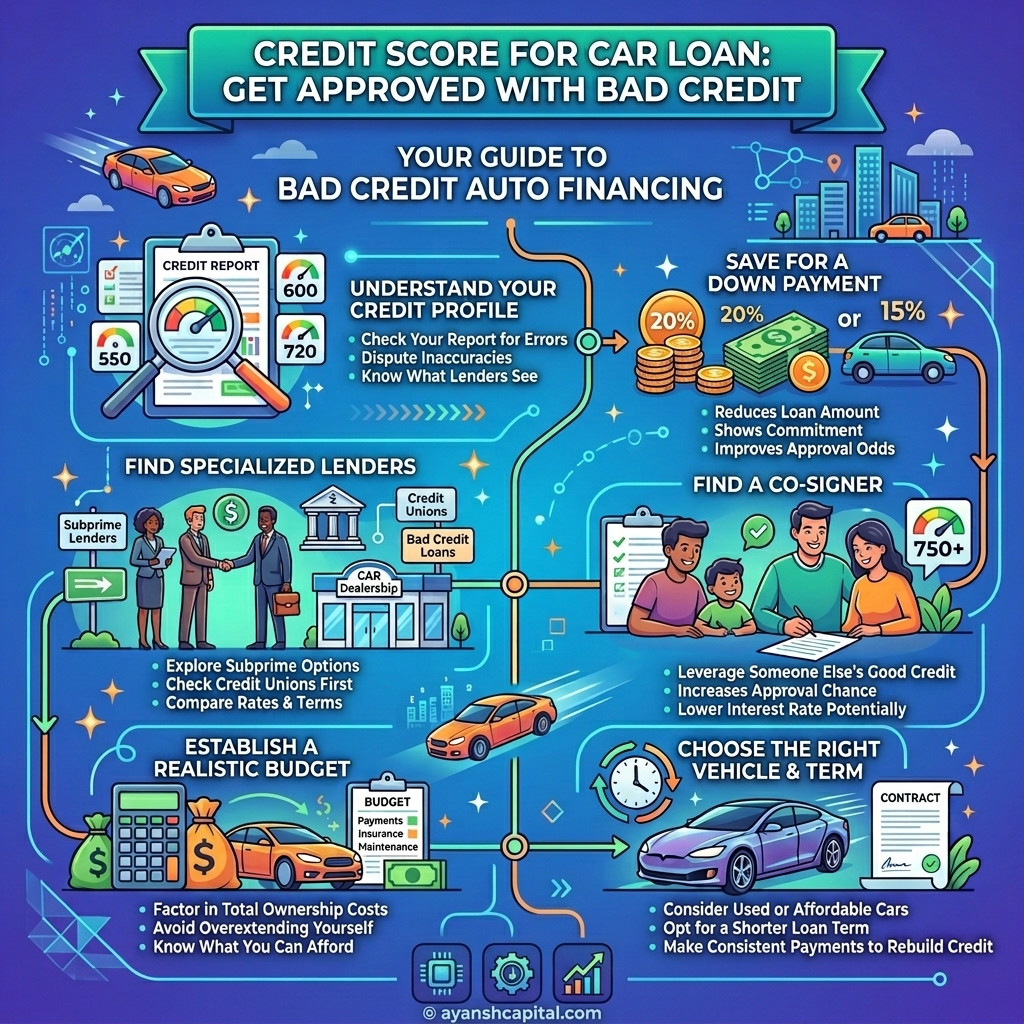

Walking directly into a dealership with bad credit without prior preparation is one of the biggest financial mistakes a subprime borrower can make. To secure an auto loan, you must proactively lower your “Risk Profile” in the eyes of the lender.

Here is a detailed, point-by-point guide on the essential steps you need to take to increase your chances of loan approval, focusing strictly on the strategies you outlined:

1. Check Your Credit Report and Dispute Errors

Before applying for any auto loan, you must know exactly what lenders will see. Often, a low Credit Score for Car Loan is dragged down further by outdated debts, inaccurate late payments, or incorrect entries.

- The Strategy: Pull your official credit reports from the three major US credit bureaus: Equifax, Experian, and TransUnion.

- The Tool: Utilize AnnualCreditReport.com, the official, federally mandated website to get your free reports.

- The Timeline: Do this 30 to 60 days before you plan to apply for the loan. If you spot any discrepancies (such as a debt you already paid off or an account that doesn’t belong to you), initiate a “Dispute” with the credit bureau immediately to get the error removed and potentially boost your Credit Score for Car Loan.

2. Arrange a Strong Down Payment (Aim for 20%)

When you are a subprime buyer with bad credit, cash is king. Lenders view bad credit as a high risk of default; bringing your own money to the table directly mitigates that risk.

- Lowering the LTV Ratio: Lenders calculate the Loan-to-Value (LTV) ratio. If you put down 20% or more, you are borrowing significantly less than the car is worth. A lower LTV ratio makes the lender feel much safer, drastically increasing your chances of approval and sometimes even qualifying you for a lower interest rate.

- Preventing Negative Equity: New and used cars experience rapid depreciation (loss of value) the moment you drive them off the lot. A strong down payment acts as a buffer, preventing you from becoming “underwater” on your loan—a dangerous financial situation where you owe the lender more money than the car is actually worth.

3. Gather Proof of Income and Residence

For traditional Prime borrowers, lenders rely heavily on the Credit Score for Car Loan. For Subprime borrowers, lenders rely heavily on your Ability to Repay. You must definitively prove that you have the steady cash flow to handle the monthly car payments.

- Income Requirements: Subprime lenders typically require proof of a stable gross monthly income of at least $1,500 to $2,000.

- Required Documentation: Do not go to a lender empty-handed. Prepare a physical or digital folder containing:

- Pay Stubs: Your most recent pay stubs covering the last 30 days.

- Tax Documents: Your W-2 forms from the past 2 years to prove sustained employment.

- Proof of Residence: A recent utility bill (such as electricity, water, or gas) in your name at your current address to verify your stability.

4. Find a Reliable Co-Signer (Optional but Highly Effective)

If your Credit Score for Car Loan falls into the Deep Subprime tier and you are facing guaranteed rejection or predatory interest rates, utilizing a co-signer can be an absolute game-changer.

- How It Works: A co-signer is a trusted friend or family member with a strong, established credit history who agrees to put their name on the loan alongside yours. The lender will primarily base the loan approval and the APR on the co-signer’s excellent credit rather than your bad credit.

- The Serious Risk: While this guarantees you a better deal, it is a massive responsibility. If you miss a payment, make a late payment, or default on the vehicle entirely, the co-signer is held legally and financially responsible. Their Credit Score for Car Loan will be ruined alongside yours. This step should only be taken if you are 100% certain of your ability to make every payment on time.

Types of Lenders: Who Approves Auto Loans for Bad Credit Borrowers?

When navigating the US auto market with a subprime Credit Score for Car Loan, knowing exactly which doors to knock on is critical. Not all lenders operate under the same underwriting algorithms, and applying to the wrong institutions will result in hard inquiries that further damage your credit.

Here is a detailed, point-by-point breakdown of the primary lender categories available to subprime borrowers:

A) Credit Unions (The Best First Option)

Credit unions are non-profit financial cooperatives owned by their members. Unlike major national commercial banks (such as Chase or Bank of America), which rely heavily on rigid, automated Credit Score for Car Loan algorithms, credit unions offer a more humanized lending approach.

- Relationship-Based Lending: Credit unions are generally more forgiving and willing to look past a low three-digit score. They focus heavily on your current debt-to-income (DTI) ratio, employment history, and your relationship with the institution.

- The Power of Explanation: If your credit was damaged due to an understandable life event—such as a sudden medical emergency, a layoff, or a divorce—you can often sit down with a loan officer and explain your situation. If you can prove a stable income now, they are much more likely to manually underwrite and approve your loan.

- Better Rates: Because they are non-profit, their interest rates are legally capped and generally much lower than what traditional banks offer to subprime borrowers.

B) Online Subprime Auto Lenders

The digital auto financing market in the US has expanded massively, creating platforms specifically engineered to cater to buyers with less-than-perfect credit.

- Capital One Auto Navigator: This is one of the most powerful tools for a subprime buyer. It allows you to pre-qualify for an auto loan using a “Soft Pull” (Soft Inquiry) on your credit report. This means you can see your real interest rate, loan terms, and maximum borrowing amount without dropping your FICO Credit Score for Car Loan by a single point.

- Carvana / Vroom (Digital Dealerships): These online platforms act as both the dealership and the lender, offering seamless in-house financing. They are highly motivated to sell cars and are known for easily accepting poor credit profiles.

- The Trade-off: While approval is easier and highly convenient, be aware that the actual sticker price of the vehicles on these platforms is often slightly higher than traditional market value to offset the financing risks they take.

C) “Buy Here, Pay Here” (BHPH) Dealerships — (Proceed with Extreme Caution)

You will easily recognize these lots by their aggressive advertising: “No Credit? Bad Credit? No Problem!” or “Your Job is Your Credit!” In this model, the dealership does not use a third-party bank; they finance the loan themselves. This should strictly be your absolute last resort.

- Massive Price Markups: To protect themselves against high default rates, BHPH dealers routinely inflate the sticker price of their vehicles, often selling cars for 20% to 30% above their actual Kelley Blue Book (KBB) market value.

- Predatory Interest Rates: They almost always charge the maximum legal interest rate allowed by the state, which frequently ranges between 20% and 25% APR.

- Aggressive Repossession Tactics (The ‘Kill Switch’): Because they cater to deep subprime borrowers, BHPH dealers install GPS trackers and starter-interrupt devices (commonly known as “Kill Switches”) in the cars. If you are even one day late on your weekly or bi-weekly payment, the dealer can remotely disable the car’s engine so it will not start, and immediately send a tow truck to repossess it.

- No Credit Building: Many BHPH dealerships do not report your on-time payments to the three major credit bureaus (Equifax, Experian, TransUnion). This means even if you pay off the car flawlessly, your Credit Score for Car Loan will not improve.

Credit Score for Car Loan: Smart Dealership Negotiation Strategies

When you walk into a dealership with bad credit, considering your Credit Score for Car Loan, the sales team often perceives you as a desperate or vulnerable buyer. To maximize their profit, they frequently utilize a psychological sales tactic known as the “Four Square” method. This technique is specifically designed to confuse you, distract you from the total cost of the vehicle, and force you to focus entirely on an affordable “monthly payment.”

To avoid falling into the dealer’s financial traps despite your Credit Score for Car Loan, you must employ strict negotiation rules. Here is a detailed, point-by-point breakdown of how to protect yourself:

Rule 1: Negotiate Only on the “Out-the-Door” (OTD) Price

The most dangerous question a car salesman will ask you is: “How much are you looking to pay per month?” You must never answer this question with a dollar amount.

- The Monthly Payment Trap: If you tell the dealer you want to pay exactly “$300 a month,” they will manipulate the math to make that happen. However, they will achieve this by extending the term of your loan from a standard 48 months to a grueling 72 or even 84 months.

- The Financial Consequence: While your monthly payment stays at $300, extending the loan term keeps you in debt longer and forces you to pay thousands of dollars in additional, compounded interest.

- The Solution: You must strip away the dealer’s ability to manipulate the numbers. Memorize and use this exact script: “I do not want to discuss monthly payments. Please provide me with the exact Out-the-Door (OTD) price of this vehicle, which includes all taxes, documentation fees, and registration costs.”

Rule 2: Weaponize Your Pre-Approval

Walking into a dealership relying solely on their Finance and Insurance (F&I) department to find you a loan for your Credit Score for Car Loan puts you at a massive disadvantage. You must secure independent financing first.

- The Power Dynamic: Obtain a pre-approval letter from a local credit union or an online lender like Capital One Auto Navigator before you ever set foot on the lot. This effectively turns you into a “cash buyer” and immediately shifts the negotiating power back to you.

- The Challenge Strategy: Dealership F&I managers have established relationships with dozens of different banks and lending institutions. Once you have negotiated the lowest possible OTD price for the car, present your pre-approval letter.

- Making Them Compete: Tell the dealer: “I am already pre-approved at a 14% APR. If your lending network can beat this rate and offer me 12% or lower, I will gladly use your financing. If not, I will use my own bank.” Use their desire to make a commission on the financing to secure a better deal for yourself.

Rule 3: Beware of the “Yo-Yo Financing” Scam (Spot Delivery)

This is one of the most common and devastating traps designed specifically for subprime borrowers struggling with their Credit Score for Car Loan. It relies on your emotional attachment to the new car.

- The Scam Mechanics: The dealer will let you sign initial paperwork, hand you the keys, and allow you to drive the car home over the weekend, even though the bank has not officially funded the loan. This is known as a “spot delivery.”

- The Trap Springs: A few days or weeks later, the dealership will call you with “bad news.” They will claim that your financing “fell through” or the bank rejected the terms.

- The Ultimatum: They will then demand that you immediately return the car to the lot or come back in to sign a brand-new contract. Unsurprisingly, this new contract will feature a significantly higher interest rate and require a larger down payment because of your Credit Score for Car Loan. Because you have already shown the car to your family and friends, the psychological pressure to keep it is immense, leading many to sign the predatory contract.

- The Protection Strategy: Never drive a vehicle off the dealership lot unless the finance manager can provide definitive proof that the loan is 100% approved, finalized, and officially funded by the bank. If they say the approval is “pending,” leave the car at the dealership and walk away until the paperwork is legally binding.

The Exit Strategy: Your Auto Loan Refinancing Masterplan

Accepting a bad credit auto loan should never be viewed as a permanent financial sentence; rather, it is a temporary stepping stone. When you are forced to take a subprime loan, you must enter the agreement with a strict, pre-planned “Exit Strategy.”

Your ultimate goal is to use the high-interest loan to repair your Credit Score for Car Loan, and then escape the predatory terms as quickly as possible. Here is the detailed, step-by-step masterplan to execute this strategy successfully:

1. The 6 to 12-Month Consistent Payment Phase (The Credit Builder)

- The Action: Accept the subprime loan, but commit to making every single payment exactly on time for the next 6 to 12 months. It is highly recommended to set up automatic payments (AutoPay) so you do not miss a single deadline by accident.

- The Science Behind It: Auto loans are classified as Installment Loans. In the FICO credit scoring model, your payment history accounts for 35% of your total score. Consistently paying an installment loan on time is one of the fastest and most effective ways to aggressively rebuild a damaged Credit Score for Car Loan, proving to future lenders that you are now a reliable borrower.

2. Aggressively Lower Your Credit Utilization Ratio

- The Action: While you are flawlessly paying your car loan, simultaneously focus on your revolving debt, specifically your credit card balances.

- The Target: Pay down your credit card bills and strictly keep your usage below 30% of your total credit limit (for example, if your credit card has a $1,000 limit, never let the balance exceed $300).

- The Science Behind It: “Amounts Owed” (primarily Credit Utilization) makes up 30% of your FICO score. While the auto loan builds your installment history, slashing your credit card balances will provide a rapid, simultaneous boost to your overall Credit Score for Car Loan.

3. Execute the Refinance (Pulling the Trigger)

- The Action: Continuously monitor your credit report. As soon as you observe that your FICO Credit Score for Car Loan has jumped by 60 to 100 points from where it was when you bought the car, it is time to take action.

- The Execution: Do not stay with your current subprime lender. Instead, gather your new, improved credit profile and apply for a refinance loan with a completely different lending institution. Credit Unions are highly recommended for this step, as they specialize in refinancing and offer the most competitive, low-interest rates to consumers with improving Credit Score for Car Loan.

4. The Financial Result (Reaping the Rewards)

- The Transformation: By successfully executing this masterplan, you effectively transition yourself out of the Subprime tier and into the Nonprime or Prime tier.

- The Savings: This maneuver can successfully slash a predatory 18% APR down to a much more manageable 8% or 9% APR.

- The Ultimate Benefit: Cutting your interest rate in half will significantly lower your monthly EMI (Equated Monthly Installment) and save you thousands of dollars in compound interest over the remaining life of the auto loan.

Credit Score for Car Loan: Avoiding the Negative Equity Trap

To truly navigate the subprime auto market for your Credit Score for Car Loan, it is crucial to understand exactly why lenders are willing to give you money when your credit is bad. The financial machinery operating behind the scenes relies on a complex system of risk and reward.

Here is a detailed, point-by-point breakdown of the financial mechanics driving subprime auto loans:

1. Loan Origination and Immediate Sale

When you sign a contract at a dealership for a high-interest loan (for example, at an 18% APR), the dealership does not keep that loan. They act merely as the originator. Almost immediately, the dealership sells your loan contract to a larger bank or a specialized financial institution to free up their own capital.

2. The Creation of Auto Asset-Backed Securities (ABS)

Once these large financial institutions purchase your loan, they do not hold it in isolation. They pool together thousands of similar subprime auto loans from across the country. This massive pool of debt is then packaged into a single, complex financial instrument known as an Auto Asset-Backed Security (ABS). These securities are then sold directly to investors on Wall Street.

3. The Investor’s Risk vs. Reward Calculus

Wall Street investors understand that the underlying loans in an Auto ABS belong to borrowers with bad credit and a low Credit Score for Car Loan. Consequently, they classify these securities as “High Risk.” In the financial world, taking on higher risk requires a higher guaranteed return. Because these investors demand high yields to purchase the ABS, that cost is passed all the way down to the consumer. This investor demand is the exact mathematical reason your individual APR is so high.

4. The Built-In Default Model

The entire subprime auto lending industry operates on a statistical business model based on your Credit Score for Car Loan that anticipates failure. Lenders and investors calculate in advance that a specific percentage of borrowers in the subprime pool will inevitably default (fail to repay) on their car loans and face repossession.

5. Cross-Subsidizing the Losses

To ensure the system remains profitable despite these inevitable defaults, lenders use the high-interest payments from successful borrowers to cover the losses of those who fail. When you pay an 18% or 20% APR, a large portion of your money is mathematically designed to subsidize the financial losses caused by other subprime borrowers who have defaulted.

6. The Ultimate Borrower Strategy: Breaking the Cycle

Understanding this Wall Street machinery fundamentally changes how you should view your loan.

- The Trap: The system is designed to extract maximum interest from you due to your Credit Score for Car Loan to balance its own risk sheets.

- The Goal: Your objective must not be merely acquiring a vehicle. Your goal is to aggressively break this statistical cycle. By making on-time payments, building your credit score and your Credit Score for Car Loan, and rapidly executing a refinance strategy, you successfully pull yourself out of the high-interest Auto ABS pool and escape the subprime trap.

The Trap of “Negative Equity” (Being “Underwater”)

In the US auto market, the absolute biggest enemy of a buyer with bad credit and a low Credit Score for Car Loan is Negative Equity, commonly referred to as being “underwater” on a loan. Dealerships often mask this dangerous financial situation under the seemingly helpful term “Rollover.”

Here is a detailed, point-by-point breakdown of how this financial trap works and how you can avoid it:

1. Understanding the Negative Equity Math

To understand how you become trapped, consider the following standard trade-in scenario:

- Your Current Loan Balance: You currently owe $10,000 to the bank for your existing vehicle.

- The Dealership’s Valuation: The dealer appraises your car and offers you a trade-in value of only $6,000.

- The Deficit (Negative Equity): The difference between what you owe ($10k) and what the car is actually worth ($6k) is $4,000. You are currently $4,000 “underwater.”

2. The Dealership’s “Rollover” Trap

If you attempt to buy a new car with a subprime credit profile and a low Credit Score for Car Loan, the dealer will use this negative equity against you.

- The Hidden Addition: The dealer will casually offer to take the old car off your hands and simply “roll over” that $4,000 of existing debt directly into your brand-new subprime auto loan.

- The Inflated Principal: If the sticker price of the new vehicle you want to buy is $20,000, your new auto loan does not start at $20,000. It instantly balloons to $24,000 (plus additional state taxes, documentation fees, and registration costs).

- The Compounding Interest Crisis: Because you have bad credit affecting your Credit Score for Car Loan, you are subject to subprime interest rates. You will now be forced to pay a massive 18% to 20% APR on that artificially inflated $24,000+ balance. Ultimately, you are paying high-interest rates on a $4,000 phantom debt for a car you no longer even own.

3. Strategic Solutions to Avoid the Trap

To protect yourself from these predatory practices regardless of your Credit Score for Car Loan, you must strictly adhere to the following avoidance strategies:

- Never Trade-In With Negative Equity: As a definitive rule, if your credit is bad based on your Credit Score for Car Loan, absolutely never trade in a vehicle if you owe more on it than its current market value. The math will always work against you.

- Pay Down the Existing Debt: Pause your plans to buy a new vehicle. Focus your financial resources on paying off the remaining deficit on your current car to bring your equity back to zero before applying for new financing.

- Execute a Private Party Sale: Dealerships deliberately underpay for trade-ins because they need to re-sell the car for a profit. Do not give them your vehicle. Instead, sell it directly to an individual buyer. A “Private Party Sale” generally yields 15% to 20% more value than a dealership trade-in offer. This extra cash can significantly reduce, or entirely eliminate, your $4,000 negative equity.

Auto Insurance Strategies That Help Protect Your Credit Score for Car Loan Approval

In the United States, a bad credit profile directly inflates your auto insurance premiums. However, by thoroughly understanding the insurance market and how major companies—such as State Farm, GEICO, Progressive, and USAA—assess risk, you can deploy advanced strategies to effectively manage and reduce these costs.

- Utilizing Bundling Mechanics (Multi-Line Discounts): Insurance providers heavily prioritize customer retention. If you are facing exorbitant auto premiums due to a subprime Credit Score for Car Loan, securing a “multi-line discount” is your strongest financial shield.

- The Strategy: Bundle your Auto Insurance with your Renter’s Insurance or Homeowner’s Insurance under the exact same provider.

- Comparative Cost Analysis: Always evaluate the total combined cost rather than looking at the auto premium in isolation. For instance, GEICO’s standalone auto policy might initially seem more expensive. However, if they offer a 15% discount for bundling renter’s insurance, your total out-of-pocket expense could be significantly lower than what you would pay for a standalone auto policy from a competitor like Progressive.

- Leveraging Telematics and Usage-Based Insurance (UBI): One of the most effective ways to completely bypass the negative impact of your Credit Score for Car Loan is to opt into a telematics program.

- How It Works: Programs like Progressive’s Snapshot or State Farm’s Drive Safe & Save calculate your premium based on your actual, real-time driving habits rather than your financial history. They use a mobile app or a plug-in device to track metrics such as how hard you brake, your acceleration patterns, and the time of day you usually drive.

- The Financial Benefit: If you are a demonstrably safe driver, these usage-based programs can result in massive premium reductions. They can slash your insurance bill by 20% to 30%, effectively overriding the penalty of a bad Credit Score for Car Loan.

- Navigating State-Specific Insurance Regulations: The US auto insurance industry is entirely regulated at the state level. This means the rules regarding how bad credit affects you change drastically depending on your zip code.

- Consumer Protection States: In states with robust consumer protection laws, such as California, or states that have recently undergone massive No-Fault law reforms, like Michigan, insurance providers are strictly prohibited by law from using your Credit Score for Car Loan to determine your insurance rates. In these states, your bad credit will not affect your premium at all.

- High-Penalty States: Conversely, if you reside in states like Texas or Florida, a bad credit profile tied to your Credit Score for Car Loan is heavily penalized and can literally double your insurance premium.

- Strategic Alternatives: If you live in a high-penalty state, your safest options are to proactively seek out localized, state-specific discounts from major carriers like State Farm. Alternatively, if you or an immediate family member are active-duty military or veterans, securing an auto policy through USAA is highly recommended, as their risk assessments are structurally different and often much more favorable to the consumer.

Co-Signer vs. Co-Borrower: Which Option Is Better for Improving Your Credit Score for Car Loan Approval?

When navigating the auto market with bad credit affecting your Credit Score for Car Loan, asking a friend or family member for help is a common and highly effective strategy. However, a single word on your financing paperwork can drastically alter the legal ownership of your vehicle.

It is vital to understand the nuanced, yet massive, differences between a Co-Signer and a Co-Borrower before you sign a contract. Here is a detailed breakdown of these two roles and the best strategy for your financial independence:

1. The Co-Signer (The Financial Guarantor)

A co-signer is essentially a financial safety net for the lender. This is usually someone with a high FICO score representing a strong Credit Score for Car Loan who agrees to attach their good credit profile to your loan application.

- Zero Ownership Rights: The most defining characteristic of a co-signer is that they have absolutely no ownership claim to the vehicle. Their name does not appear on the car’s Title.

- Total Financial Liability: Despite not owning the car, they are 100% legally responsible for the debt. If you miss a payment or default on the loan, the lender will aggressively pursue the co-signer for the money, and the co-signer’s credit score and their Credit Score for Car Loan will plummet alongside yours.

- Your Control: Because you are the sole name on the title, you have full legal authority to sell the car, trade it in, or modify it without needing the co-signer’s permission.

2. The Co-Borrower (The Joint Applicant)

A co-borrower, often referred to as a “Joint Applicant,” is taking on an entirely different legal role.

- Shared Ownership: A co-borrower is an equal partner in the transaction. Their name will be legally printed on the car’s Title right next to yours.

- Shared Liability: Just like a co-signer, they are equally responsible for ensuring the monthly payments are made on time.

- Loss of Sole Control: Because they are a legal co-owner, you cannot sell the vehicle, trade it in, or sometimes even alter the insurance policy without their explicit signature and legal consent.

3. The Winning Strategy: Why You Should Choose a Co-Signer

If your ultimate goal is to rebuild your bad credit for your Credit Score for Car Loan and maintain total control over your asset, you must always aim for a Co-Signer rather than a Co-Borrower.

- By utilizing a co-signer, you reap the benefits of their excellent credit score and high Credit Score for Car Loan (securing loan approval and a much lower APR) while maintaining absolute ownership of the vehicle. It prevents future legal complications if your relationship with that person sours or if you decide to sell the car unexpectedly.

4. The Exit Plan: Look for a “Co-Signer Release” Clause

When negotiating a loan with a co-signer, you should always ask the lender if their contract includes a “Co-Signer Release” option.

- How it Works: This specific clause is a built-in exit strategy. It stipulates that if the primary borrower (you) makes a specific number of consecutive, strictly on-time payments—usually spanning 12 to 24 months—you can legally apply to remove the co-signer from the loan entirely.

- The Benefit: Once executed, the loan is transferred solely into your name based on your newly improved, demonstrated payment history. Your co-signer is freed from the liability, and you successfully complete your transition to an independent borrower.

Credit Score for Car Loan: Choosing the Right Vehicle

When navigating the auto market with bad credit affecting your Credit Score for Car Loan, buyers often become overwhelmingly hyper-focused on securing an affordable monthly loan payment. In doing so, they completely overlook a crucial financial factor: the specific make and model of the vehicle directly dictates the strictness of the insurance underwriting process. Major US insurance carriers—particularly USAA, State Farm, GEICO, and Progressive—rely on massive, highly sophisticated data pools to calculate risk.

Here is a detailed, point-by-point breakdown of how your vehicle choice interacts with your Credit Score for Car Loan during the underwriting process:

- The Compound Penalty of “High-Risk” Vehicles

- The Problematic Models: If you have bad credit and attempt to finance vehicles like a Dodge Charger, Nissan Altima, or Hyundai Elantra, you are setting yourself up for a financial disaster.

- The Actuarial Data: According to comprehensive insurance industry data, these specific vehicle models carry statistically massive rates of theft and are frequently involved in high-speed collisions and accidents.

- The 200% Premium Spike: In the eyes of an insurance underwriter, a bad Credit Score for Car Loan already legally flags you as a high-risk driver. Combining a high-risk credit profile with a statistically high-risk vehicle creates a compounding algorithmic penalty. This toxic combination can cause your auto insurance premiums to violently skyrocket by up to 200%.

- The Smart Strategy: Opting for High-Safety, Low-Risk Profiles

- The Recommended Models: To actively combat your bad credit penalty tied to your Credit Score for Car Loan, you must intentionally select vehicles renowned for elite safety standards, crash survivability, and family-oriented utility. Prime examples of these preferred vehicles include the Subaru Outback, Honda CR-V, and Toyota RAV4.

- The Algorithmic Softening: Insurance companies categorize these specific vehicles as “low-risk.” This is due to both their advanced factory safety features and the historically safe, predictable driving habits of the demographic that typically purchases them.

- The Ultimate Financial Savings: When underwriters at major companies like State Farm and GEICO process an insurance policy for a subprime borrower who is purchasing a highly rated, safe vehicle, the algorithm actually softens the severe blow of the bad Credit Score for Car Loan. The low-risk nature of the car effectively offsets the high-risk nature of your financial history, allowing you to secure massive, long-term savings on your auto insurance bill.

The Mathematics of the “Sales Tax Shield” on Trade-Ins

When navigating the auto market with bad credit affecting your Credit Score for Car Loan, your absolute primary goal must be to reduce the total amount of money you are financing. By lowering your Loan-to-Value (LTV) ratio, you minimize the amount of principal subject to predatory interest rates. This is exactly where understanding and utilizing the “Sales Tax Shield” becomes a massive financial game-changer.

Here is a detailed, point-by-point breakdown of how this tax mechanism works and why it is uniquely beneficial for subprime borrowers working on their Credit Score for Car Loan:

- Understanding the Trade-In Tax Benefit In the majority of US states (such as Texas, Florida, and Illinois), purchasing a vehicle subjects you to a state sales tax that typically ranges from 6% to 10%. However, when you trade in your old vehicle at a dealership, most states offer a highly advantageous tax break. You are legally required to pay sales tax only on the difference between the price of the new vehicle and the value of your trade-in, rather than the full purchase price.

- The Exact Math: How the Shield Works To see the real-world impact, let’s look at a standard transaction in a state with an 8% sales tax:

- Scenario A (Without a Trade-in): You buy a vehicle for $25,000. You must pay the full 8% sales tax on the entire amount. This equals $2,000 in tax, bringing your total financed cost to $27,000.

- Scenario B (With a $5,000 Trade-in): You buy the same $25,000 vehicle, but you trade in your old car valued at $5,000. Thanks to the tax shield, you are only taxed on the remaining balance ($25,000 minus $5,000). You are now taxed 8% on $20,000, which equals only $1,600 in tax.

- The Compounding Value for Subprime Borrowers In the mathematical example above, the Sales Tax Shield immediately saved you $400 upfront. However, for a buyer with bad credit and a low Credit Score for Car Loan, the actual savings are much deeper.

- If you had rolled that extra $400 into a subprime loan with an 18% APR over a standard 5-year (60-month) term, you would be paying compound interest on that tax money.

- By shielding that $400 from being financed, you are actually saving yourself approximately $700 over the life of the loan. Every dollar you keep off the principal balance exponentially reduces your high-interest burden associated with your Credit Score for Car Loan.

- Crucial Warning: State-Specific Exceptions It is vital to know that auto insurance and vehicle taxation are regulated strictly at the state level.

- This tax shield does not apply universally. If you reside in states like California, Michigan, or Virginia, the law requires you to pay the sales tax on the full purchase price of the new car, completely regardless of how much your trade-in is worth.

- Action Step: Before setting foot in a dealership, you must always verify the specific tax codes in your jurisdiction by visiting your local Department of Motor Vehicles (DMV) website.

Conclusion: Credit Score for Car Loan – Get Approved with Bad Credit

Securing an auto loan with a poor Credit Score for Car Loan is challenging, but it is entirely possible with the right preparation and strategy. By understanding how lenders evaluate your FICO Auto Score, saving for a strong 20% down payment, and avoiding predatory “Buy Here, Pay Here” dealerships, you can protect yourself from massive financial losses. Always negotiate the Out-the-Door (OTD) price, utilize a reliable co-signer if necessary, and avoid trading in a vehicle with negative equity. Most importantly, accept a subprime loan only as a temporary stepping stone. By making consistent on-time payments for 6 to 12 months, you can rebuild your Credit Score for Car Loan and successfully execute a refinancing masterplan to secure a much lower interest rate and regain your financial freedom.

10 Frequently Asked Questions (FAQs)

Question 1: What is the FICO Auto Score, and how does it differ from a standard Credit Score for Car Loan?

Answer: It specifically predicts your likelihood of repaying a vehicle loan, rather than measuring general debt risk.

Question 2: How exactly does falling into the “Deep Subprime” credit tier affect the Annual Percentage Rate (APR) on a vehicle?

Answer: It triggers predatory interest rates (often 15% to 21%+), forcing you to pay thousands of dollars in extra compound interest.

Question 3: Why is providing a 20% down payment considered crucial when applying with a bad Credit Score for Car Loan?

Answer: It lowers the Loan-to-Value (LTV) ratio, reducing lender risk, increasing approval odds, and preventing negative equity.

Question 4: What specific proof of income and residence documents do subprime lenders require for auto loan approval?

Answer: They require your last 30 days of pay stubs, 2 years of W-2 forms, and a recent utility bill to prove a stable income.

Question 5: What is the fundamental legal and financial difference between a Co-Signer and a Co-Borrower?

Answer: A Co-Signer financially guarantees the loan but has no ownership rights. A Co-Borrower shares equal legal ownership of the vehicle.

Question 6: Why are “Buy Here, Pay Here” (BHPH) dealerships considered the absolute worst option for subprime borrowers?

Answer: They overprice vehicles, charge maximum APRs, use GPS kill switches, and often don’t report payments to help build your Credit Score for Car Loan.

Question 7: How does the dealership’s “Four Square” negotiation method trick buyers who focus only on their monthly payment?

Answer: It matches your desired monthly payment but secretly extends the loan term to 72-84 months, trapping you in hidden interest.

Question 8: What is the “Yo-Yo Financing” (Spot Delivery) scam, and how can a buyer protect themselves before driving off the lot?

Answer: Dealers let you drive home on a “pending” approval, then later claim it fell through to force a higher-rate contract. Only leave when the loan is 100% funded.

Question 9: How does rolling over “Negative Equity” into a new auto loan financially trap buyers with a low Credit Score for Car Loan?

Answer: It adds your old car’s remaining debt to your new loan, forcing you to pay an 18%+ subprime interest rate for a car you no longer own.

Question 10: What are the exact steps to successfully execute an auto loan refinancing masterplan after 6 to 12 months?

Answer: Make 100% on-time payments for 6-12 months, lower credit card debt, and refinance with a Credit Union once your Credit Score for Car Loan improves.