Progressive Car Insurance Review : Is It Really Worth It?

Beyond the Commercials: The Real Truth About Progressive Car Insurance

Finding an insurance company that actually has your back after a wreck is incredibly stressful. Back in 1937, two lawyers named Jack Green and Joseph Lewis saw this struggle firsthand. They founded the company with a bold, compassionate mission: to protect the everyday, “high-risk” drivers that big, traditional corporations simply ignored. Today, that same innovative spirit is the very foundation of Progressive Car Insurance, making it a massive top-three US auto insurer that competes directly with giants like State Farm.

But is your family actually safe with them? When it comes to financial stability, their coverage acts as a rock-solid safety net for your hard-earned money.

- Elite Financial Strength: They hold the massive cash reserves needed to pay out your claims, even during severe economic downturns. Top-tier independent agencies verify this completely: A.M. Best awards them an ‘A+’, S&P gives them an ‘AA’, and Moody’s rates them at an impressive ‘Aa2’.

- Peace of Mind for Your Family: Imagine the relief of knowing that if a massive storm destroys your car, your family’s budget is completely protected. The agonizing fear of an insurer going bankrupt while you wait for a repair check simply does not exist here.

However, having deep pockets does not always equal a warm, comforting voice when you are standing freezing on the side of a highway. While their mobile app is incredibly reliable, the human element of their customer service sits right at the national average.

- The Reality of Claims: According to J.D. Power, they process payouts quickly, but you might miss out on deeply personalized care. You will be dealing with a highly efficient digital system rather than an empathetic, local agent holding your hand.

- Real Data on Complaints: The numbers actually work in their favor. Their National Association of Insurance Commissioners (NAIC) complaint index is just 0.89. This means they receive significantly fewer official consumer complaints than the national baseline average of 1.00 for a company of their massive size.

- Everyday Driver Trust: Real families appreciate this straightforward efficiency. They boast an ‘A+’ rating from the Better Business Bureau (BBB) and a solid score of 80/100 from Consumer Reports for their transparent pricing and flexible coverage options.

The Bottom Line

Ultimately, choosing Progressive Car Insurance means you are trading a close, personal relationship with a local agent for elite financial security and top-notch technology. They earn a solid ‘A’ for keeping your money safe and a ‘B’ for customer warmth. If you are a busy parent who just wants an easy app and guaranteed claim payouts, they are an incredible choice. But if you prefer handling your life’s emergencies face-to-face over a cup of coffee, you might want to keep shopping around.

Car Insurance Company Comparison with Progressive Car Insurance: All You Need to Know

America’s “Top 20 Giants” (The Big 20)

This group controls over 95% of the entire US auto insurance market.

Giving Your Family’s Budget a Break: 11 Ways to Lower Your Progressive Car Insurance Bill

Every parent knows the quiet anxiety of sitting at the kitchen table late at night after the kids have gone to bed. You watch those monthly bills creep upward, wondering where the extra money will come from this time. When you are working tirelessly just to keep food on the table and a roof over your family’s head, managing your auto coverage shouldn’t feel like another heavy weight on your shoulders.

Fortunately, finding the right Progressive Car Insurance policy opens the door to a massive array of stacking discounts. These simple savings can instantly breathe life back into your bank account. It gives you more room for the things that actually matter, like buying fresh groceries, saving for your child’s education, or finally being able to take a weekend trip without feeling financially guilty.

Here is the unvarnished breakdown of how you can protect your wallet right now:

- Combining the coverage on your family home with the policy for your daily commuter car or minivan unlocks an easy 5% to 12% off, standing as their single largest average discount for families.

- Your daily commitment to keeping your kids safe on the way to school pays off, as a completely clear driving record for three years automatically triggers a massive Safe Driver savings of up to 30%.

- Enrolling in the Snapshot telematics program tracks your habits to reward safe driving, saving the average careful driver about $231 a year, though risky habits can raise rates.

- Insuring both your commuter car and your spouse’s vehicle under a single household policy automatically triggers a 10% to 12% reduction, taking a huge financial weight off multi-car families.

- You earn a valuable loyalty rate break simply for maintaining uninterrupted Progressive Car Insurance coverage, even if you spent years previously insured by a direct competitor.

- Offset the terrifyingly high cost of handing your teenager the car keys; if your young student stays focused and maintains a solid “B” average or a 3.0 GPA, you can drop rates by up to 10%.

- The bittersweet tears of dropping your child off at a college over 100 miles away come with a silver lining, as leaving their car safe at home qualifies you for a neat 5% to 10% Distant Student rate cut.

- Simply owning the home where your family makes memories earns you a 5% discount based on your financial stability and hard work, even if your actual house is insured through an entirely different company.

- Completing your application online and signing your legal documents electronically saves the company operational costs, and they pass that quick 5% to 9% savings directly back to you.

- Ditching paper statements and setting up automatic monthly bank withdrawals cuts down administrative billing fees, keeping an extra $20 to $50 in your pocket for household essentials.

- If you happen to have the savings to pay your entire six-month premium upfront in a single transaction, you completely wipe out monthly installment fees and grab another 5% to 10% discount.

The “Name Your Price” Reality Check

The famous Name Your Price tool sounds incredibly empowering at first glance. You type in your exact target monthly budget, and the system builds custom coverage packages to hit that precise number. It allows you to safely tweak deductibles or add-ons, giving you a real-time look at how much you will pay out of pocket.

However, there is a very real, hidden danger for everyday families trying to save a few dollars. Setting your target budget too low automatically forces the system to strip away essential protections. It often removes comprehensive, collision, or gap coverage just to meet your price point.

Finding affordable Progressive Car Insurance shouldn’t mean leaving your loved ones completely vulnerable to financial ruin if someone runs a red light and totals your family vehicle. Never trade your family’s long-term safety net just to chase a cheaper monthly bill today.

The Truth About Snapshot: Is This Progressive Car Insurance Program Worth the Risk?

The promises made in those quirky television commercials often sound deeply comforting. They make it seem like simply being a good driver will instantly solve your monthly budget worries.

But the Snapshot telematics program is a slightly different story behind the scenes. While it claims to reward safe habits, the actual algorithm behind this Progressive Car Insurance feature introduces a high-stakes financial gamble. It can actually add intense, unexpected stress to your daily commute if you aren’t fully prepared for how it quietly watches your every move.

The Money Talk: Will This Actually Help Your Family’s Budget?

Enrolling gives you an immediate, temporary 10% sign-up discount. This offers a wonderful, brief sigh of relief for your wallet, maybe covering a week’s worth of gas. But that comfort only lasts for your first six months of monitoring. Once the tracking wraps up, the real numbers finally kick in.

Roughly 80% of drivers do successfully secure a permanent rate reduction, saving an average of $250 a year to put toward their household. However, the bottom 20% face a harsh financial sting that hurts hardworking families.

Unlike standard competitors who gently remove a discount for poor driving, this specific Progressive Car Insurance algorithm will actively penalize you. They will actually raise your premiums by 10% to 15% if the computer system decides it dislikes your daily habits.

The Cold Math: How the Algorithm Judges Your Daily Life

The tracking software sadly lacks basic human empathy. It doesn’t care if you had to slam your brakes to avoid a stray dog, a neighborhood child chasing a ball, or a texting driver swerving into your lane. It relies entirely on cold, rigid physics.

- Slamming your brakes and dropping your speed by more than 7 mph in a single second is the absolute number-one reason scores plummet, even if you were avoiding a terrible crash.

- Gaining over 7 mph in a single second easily traps owners of quick-accelerating electric vehicles, financially punishing them for the way their car was manufactured.

- Driving between midnight and 4:00 AM heavily tanks your score. This inherently punishes hardworking night-shift nurses, tired warehouse workers, or a panicked parent rushing to a 24-hour pharmacy for a toddler’s fever medicine.

- The system mathematically penalizes long stretches on the road, meaning it inherently punishes parents who must endure exhausting, long daily commutes just to provide for their kids.

- If you use the digital version, even just picking up your phone at a red light to check an urgent text from your spouse triggers an immediate distraction penalty.

Protecting Your Peace of Mind: Why How You Track Matters

If you join the program, you have to choose how they monitor your daily life. The smartphone app is notoriously prone to draining your battery and registering deeply frustrating false positives. It can easily mistake a bumpy ride on a public city bus, or a casual trip sitting in a friend’s passenger seat, for your own bad driving. This glitchy technology can unfairly hike your family’s rates without you doing anything wrong.

On the flip side, a physical plug-in device sits quietly under your steering wheel. It completely ignores your phone, tracks only the physical movements of your vehicle, and generates zero false alarms.

Choosing the physical plug-in ensures your Progressive Car Insurance premium is judged fairly on your actual driving. It keeps your hard-earned money safe from glitchy, overly sensitive mobile tracking software that lacks common sense.

Our Final Advice for Hardworking Families

If you decide to take the gamble to lower your bills, always protect yourself by choosing the physical hardware over the smartphone app. Telematics can absolutely work to your family’s financial advantage, but only if you understand how to play the game intelligently and cautiously.

By stacking those everyday standard discounts and navigating the tracking program carefully, you can successfully secure dependable Progressive Car Insurance at a price that honors your hard work. You deserve coverage that protects both your family on the road and your deep peace of mind when you finally pull into the driveway at home.

Progressive Car Insurance (50-State)

Progressive Auto Coverage (Quick Reference)

Choosing the Right Protections: Which Progressive Car Insurance Add-Ons Does Your Family Actually Need?

When you are trying to balance the mortgage, buy groceries, and set aside a little for your kids’ future, every single dollar counts.

Staring at a long list of optional insurance extras can feel incredibly overwhelming for any parent.

You desperately want to protect your family from disaster, but you don’t want to waste hard-earned money on things you will never use.

Let’s look at what is actually worth adding to your Progressive Car Insurance policy and what you can safely leave behind.

- Roadside Assistance costs just $4 to $6 a month.

- Picture your spouse stranded on a dark highway with a flat tire and the kids crying in the back seat.

- For the cost of a single cup of coffee, this covers 24/7 towing, battery jumps, and fuel delivery.

- It is absolutely worth it, saving you from a painful out-of-pocket tow bill that could easily ruin your weekly grocery budget.

- Rental Car Reimbursement runs about $5 to $8 a month.

- If someone runs a stop sign and totals your family vehicle, auto repairs can drag on for weeks.

- Trying to juggle school drop-offs, pediatric appointments, and commuting to work without a car is a complete nightmare.

- This pays for a daily rental, saving you from an unexpected bill of $900 or more, making it a highly recommended safety net.

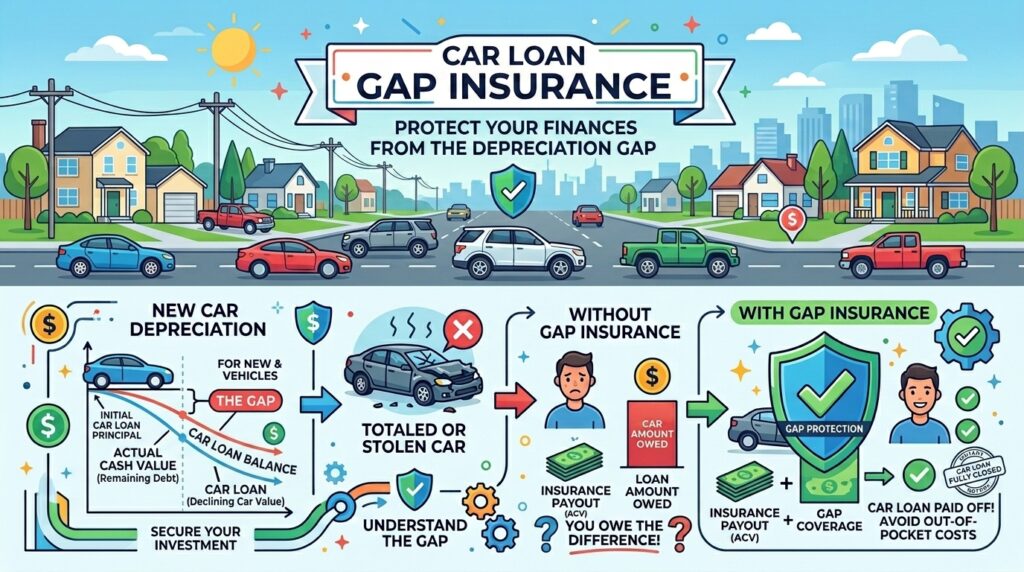

- Gap Insurance costs $5 to $10 a month and is vital for new car buyers.

- If you just bought a safe new minivan to fit the whole family, its value drops the moment you drive it off the lot.

- If it gets completely destroyed in a sudden crash, this pays the frightening difference between your high loan balance and the car’s actual value.

- It is a must-have for new loans so your family isn’t left paying for a car that no longer exists in your driveway.

- Custom Parts and Equipment costs $10 to $20 a month and protects up to $5,000 in aftermarket modifications.

- Honestly, when you are focusing on paying for your teenager’s braces or keeping up with winter heating bills, you should pass on this.

- Unless you have poured serious extra cash into upgrading your vehicle, it is highly conditional.

- Rideshare Coverage runs $15 to $30 a month.

- So many parents are driving for Uber or delivering meals late at night just to make ends meet and pay off credit cards.

- If you are doing gig work, this fills the dangerous liability gap when your app is on but you haven’t accepted a trip.

- It is completely mandatory for gig workers.

- If you skip this, they can deny your claim or cancel your Progressive Car Insurance entirely for fraud, leaving you legally and financially devastated.

- Deductible Savings Bank costs $3 to $5 a month.

- You pay extra every month just to potentially lower your deductible by $50 if you drive perfectly for six months.

- It is basically a bad math equation for a tight household budget, so you should skip it completely.

- You are far better off putting that extra cash into a glass jar on your kitchen counter for real family emergencies.

- Pet Injury Coverage is completely free.

- For many of us, our dogs and cats are truly beloved members of the family, riding along to the park or the vet.

- If your furry best friend gets hurt in a crash, you automatically get up to $1,000 in vet bills covered.

- It is a fantastic, deeply comforting bonus included for free if you carry standard collision coverage.

We highly suggest doing an annual audit of your Progressive Car Insurance policy sitting at the dining table with a cup of tea.

Drop Gap Insurance once your loan balance is finally lower than what your car is worth, usually after two or three years of hard-fought payments.

This puts about $120 a year right back into your pocket for school supplies.

You can also drop rental reimbursement once your trusty old car hits ten years old and is nearing the end of its reliable life.

Finding Your Fit: Is Progressive Car Insurance Truly the Best Choice for Your Household?

Every family is uniquely different. What works beautifully for your neighbor’s budget might be a terrible financial fit for your own home.

It helps to know exactly who benefits most from a Progressive Car Insurance plan, and who should kindly look elsewhere to protect their family’s savings.

- If you have had a rough patch in life, like an accident, a DUI, or a struggling credit score due to unexpected medical bills, the penalties here are much softer.

- They give high-risk drivers a fair, compassionate second chance to get back on their feet.

- For the hardworking parents hustling after hours on gig apps like Uber or DoorDash to pay for summer camp, they offer the most transparent and flexible protection available.

- Adding a teenager to your policy is famously terrifying for your wallet.

- But their strong discounts for good grades can significantly help offset the massive cost of handing your child the car keys for the first time.

- If you love technology and drive carefully with your kids in the back, using their telematics program allows you to actively lower your own rates, rewarding your cautious daily habits.

- If you inherited a beloved classic car from a grandparent, their partnership with Hagerty gives you top-tier agreed value coverage to protect that precious family heirloom.

- However, if you have a completely flawless driving record and perfect credit after years of hard work, you might find steeper discounts elsewhere to reward your perfection.

- If you want to bundle your home and auto seamlessly under one roof, be aware that their home coverage is handled by third parties.

- This can make claims deeply stressful when a severe storm damages the roof over your family’s heads.

- Military families who have sacrificed so much for our country should look to USAA instead, as this specific Progressive Car Insurance option sadly lacks specialized rates to honor veterans.

- If you stretched your family budget to buy an electric vehicle to save on gas, you might face surprisingly high rates here due to the terrifyingly high cost of repairing EV batteries.

- For our beloved seniors over 65, natural reflexes slow down.

- The tracking app might brutally penalize older drivers for hard braking, making other alternatives a much kinder choice to protect our aging parents.

The bottom line is simple. Lock in a Progressive Car Insurance policy if you do late-night gig work, have a few honest mistakes on your record, or need to cover a brand-new teenage driver.

Look to other major carriers if you want seamless home bundling, have a pristine driving record, or qualify for honorable military benefits.

Grace for the Road Ahead: How Progressive Car Insurance Handles Mistakes and Driving Violations

We are all human, and sometimes we make terrible mistakes behind the wheel.

A moment of pure distraction because a tired toddler is crying in the backseat can unfortunately lead to a fender bender.

Even with a violation on your record, securing Progressive Car Insurance often remains a much more affordable lifeline for stressed drivers than going to strict competitors.

Here is the honest truth about how mistakes impact your family’s monthly premium.

- Severe violations like a DUI or a hit-and-run are devastating, as your rates will jump by 70% to 90%.

- This is a massive financial blow that can force a family to skip vacations or delay needed home repairs.

- However, unlike others who will immediately abandon you, they rarely drop your coverage.

- They will quickly provide the SR-22 filings you need to keep legally driving to work and providing for your kids.

- If you accidentally cause a crash, expect your rates to increase by 40% to 65%.

- But there is real grace here with their small accident forgiveness program.

- It completely waives this painful price hike if the total property damage is under $500.

- They deeply understand that minor scrapes happen in crowded grocery store parking lots while rushing home.

- Getting caught speeding when you are late for your child’s school play, or checking a text message, will usually trigger a 10% to 25% increase.

- Fortunately, spending a Saturday taking a defensive driving course can often erase these minor penalties and restore your peace of mind.

- Minor tickets, like briefly forgetting to buckle a seatbelt during a quick trip to the neighborhood pharmacy, usually result in a tiny 3% to 5% hike.

- In some states, it is actually strictly illegal for them to raise your rates for this at all.

Most violations will thankfully clear from your record and stop hurting your budget after three long years, though severe ones take five.

If you have proven yourself over time and qualified for their elite Platinum tier, your very first major at-fault accident surcharge is completely forgiven.

It is a vital safety net that ensures one bad day on the road doesn’t permanently ruin your ability to afford Progressive Car Insurance to keep your loved ones safe.

Full Coverage Top 15 Auto Insurance Rate Comparisons

Below is a detailed breakdown of Top 15 Car Insurance average annual rates for full coverage auto insurance across various driver profiles, compared directly against the national average.

Top 15 Car Insurance Rates by Age & Experience

In the auto insurance industry, age and driving experience heavily dictate your premium. As you gain experience and your statistical risk of accidents decreases, Top 15 Car Insurance Rates by Age & Experience. Here is a quick breakdown of how age impacts your premium:

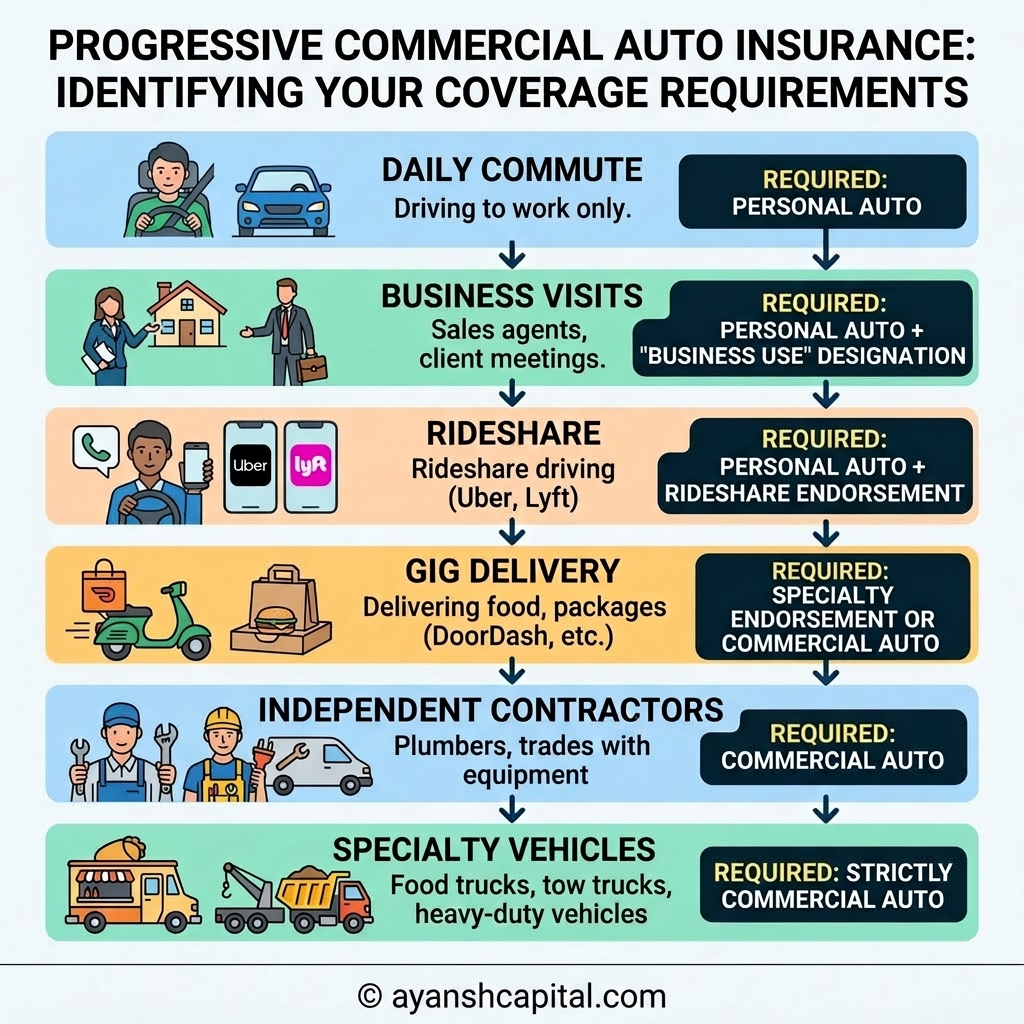

Progressive Commercial Auto Insurance: Identifying Your Coverage Requirements

If you use your vehicle for work—from gig delivery to heavy contracting—a standard personal policy will not protect you. Here are Progressive’s requirements to avoid a denied claim:

Vehicle Use & Policy Requirements

The Bottom Line: A commercial policy usually costs only 15% to 25% more than a personal policy, and the premiums are 100% tax-deductible as a business expense.

The Impact of Driving Violations on Premiums: A Comprehensive Breakdown

Even with a driving violation, Progressive often remains a more affordable option for high-risk drivers than competitors like GEICO or State Farm. Here is how different infractions impact your premium.

Severe Violations: The Dealbreakers

- Severe (DUIs, Hit & Runs): Rates jump 70% to 90%. However, Progressive rarely drops your coverage and provides quick SR-22 filings.

- At-Fault Accidents: Rates increase 40% to 65%. Progressive’s Small Accident Forgiveness waives this hike if total property damage is under $500.

- Speeding & Distracted Driving: Expect a 10% to 25% increase. Taking a defensive driving course can often erase minor speeding penalties.

- Minor Tickets (Seatbelts): Only a 3% to 5% hike, though some states make it illegal to raise rates for this at all.

The Bottom Line: Most violations clear from your record after three years (five for DUIs). If you qualify for Progressive’s Platinum tier, your first major at-fault accident surcharge is completely forgiven.

Progressive Claims: Quick Timeline

Progressive’s Home & Auto Bundle: The Hidden Catch

Bundling home and auto is standard advice, but Progressive handles it differently than traditional insurers. Because Progressive is primarily a car insurance company, their home insurance setup comes with a few hidden risks.

The Bottom Line

- Renters: Yes, bundle. It’s a quick, low-risk way to lower your auto insurance rate.

- Homeowners: Skip the bundle. Keep Progressive for your auto insurance if the rates are good, but buy your homeowners insurance from a dedicated property insurer to avoid a claims nightmare

How to Cancel Your Progressive Car Insurance Without Financial Stress

- Canceling an auto policy is usually a free process, but timing matters greatly when you are managing a tight household budget.

- If you wait until renewal, simply disable AutoPay 10 days early to avoid accidental charges that could unexpectedly drain your grocery fund.

- You can easily cancel your Progressive Car Insurance mid-term and receive a prorated refund within 14 days, though a few specific states charge a ~10% early penalty.

- If you sold your commuter car to pay college tuition, backdate the cancellation to the sale date using your Bill of Sale, and return Snapshot devices within 30 days to avoid a $50 fee.

- Never ghost the company by stopping payments, as this creates a lapse. If you need an SR-22 for your job, ensure your new policy is active before canceling.

- A single day uninsured causes new insurers to spike rates by 15% to 20%. Handle your Progressive Car Insurance transition properly by scheduling cancellation for the exact day new coverage starts.

Getting Your Progressive Car Insurance Quote: The Bottom Line

- When sitting down on a quiet Sunday morning to organize finances, getting a free quote takes exactly 10 minutes and won’t hurt your credit score.

- Use their mobile app, call their 1-800 number, or contact a local agent. Have your license, car VIN, and limits ready so your Progressive Car Insurance quote is perfectly accurate.

- Always be honest about past accidents. Hiding a past mistake will only spike your final Progressive Car Insurance price at checkout when they verify your record.

- Adjust your deductibles or use the Name Your Price® tool to input your strict monthly budget and let the system build a plan that fits real life.

- Once satisfied, this flexible plan lets you lock in extra savings by choosing AutoPay or paperless billing to print your ID cards instantly.

- It is the top choice for gig workers paying off student loans or folks with low credit. Progressive Car Insurance might be exactly what your household needs right now to stay secure without feeling judged.

Your Top 10 Progressive Car Insurance Questions Answered

- How long is the grace period before cancellation? If you miss a payment while juggling heavy household bills, the grace period is typically 10 to 20 days depending on your specific state.

- Are rental cars covered while on vacation? Yes, comprehensive and collision coverages easily extend to rental cars in the US and Canada, saving money on family summer road trips.

- Can using the Snapshot program raise your rates? Yes, roughly 20% of high-risk drivers receive a premium surcharge, which could accidentally hurt your family’s hard-earned savings.

- Is food delivery or rideshare driving covered by standard policies? No, standard Progressive Car Insurance policies don’t cover commercial driving; parents working side gigs must add a specialized endorsement.

- What exactly does Gap Insurance cover? It pays the scary difference between the actual cash value and your loan if totaled, protecting families from paying for a destroyed minivan.

- Can you cancel a policy mid-term? Yes, you get a prorated refund to help with family needs, though short-rate states do charge a 10% penalty on the remaining premium.

- Does your personal credit score affect your auto premium? Yes, lower scores significantly increase rates in most US states. Improving credit directly lowers monthly costs and brings financial stability.

- Will a minor speeding ticket permanently ruin my rates? A minor ticket while rushing to a school meeting won’t haunt you forever. A trusted Progressive Car Insurance policy often forgives these over time.

- Are there good student discounts for teenage drivers? Yes, submitting your teen’s report card with good grades offsets the notoriously expensive cost of insuring a newly licensed child.

- Can I bundle my home and auto coverage to save money? Bundling is the easiest way to secure a discount, simplifying bills and leaving more cash in your wallet for your family’s future.