Full Coverage Car Insurance USA: Everything You Need to Know

The True Peace of Mind: Why Your Family Needs full coverage car insurance

Protecting your children’s joyful laughter in the backseat is a parent’s highest priority. In the United States (USA), many mistakenly believe there is a single magical document that shields them from every danger on the road. However, legally and technically, there is no single policy actually named full coverage car insurance.

1. Building a Loving Safety Net: The Reality of full coverage car insurance

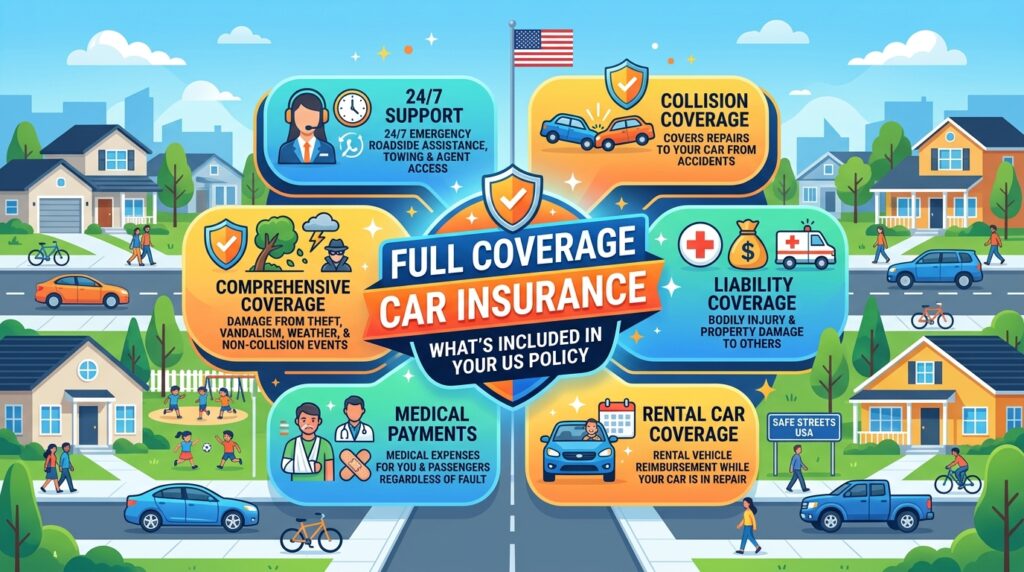

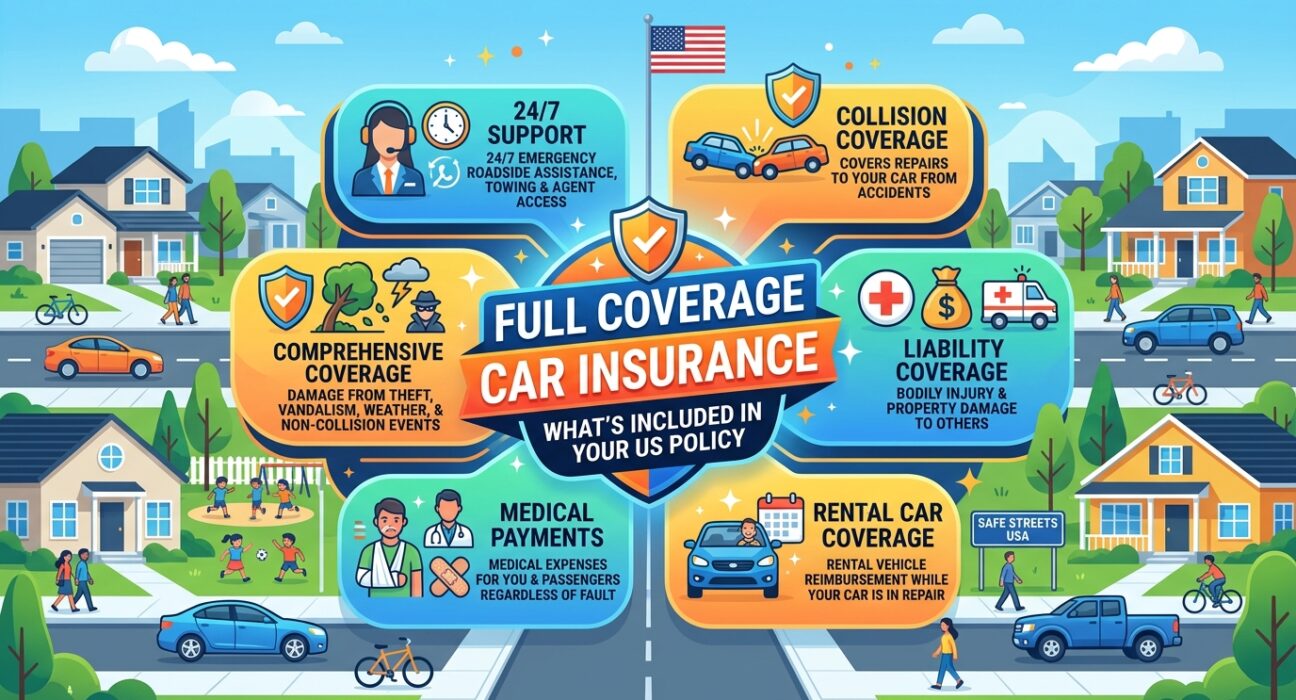

In reality, getting this protection means building a loving safety net made of a bundle of specific coverages. When you combine three main portions of care—Liability, Collision, and Comprehensive—it forms this protective shield to secure your family’s financial future. Let us deeply analyze these three portions, explicitly answering what they are and what they include, keeping all your vital data intact through the beautiful lens of family values.

2. Caring for Others (Liability): The Foundation of full coverage car insurance

In almost every state in America (with a few exceptions like New Hampshire and Virginia), having Liability coverage is legally mandatory before you drive.

What is it? The compassionate rule here is: “It is not for you, it is for others.” If you accidentally make an honest mistake on the road and cause an accident, this coverage pays for the damages caused to the other person, so you do not have to empty your children’s college savings to help them. It is divided into two parts of human care:

- Bodily Injury (BI): Respectfully pays for their medical bills, hospital expenses, ambulance fees, and even their ‘lost wages’ so their family does not suffer.

- Property Damage (PD): Pays to repair their car, or if you accidentally hit their wooden fence, mailbox, or the front of a local shop. (Note: The limits are usually written as 25/50/25, meaning $25,000 for one person’s injuries, $50,000 for total injuries, and $25,000 for property damage).

3. Shielding Your Own Vehicle (Collision): The Strong Defense of full coverage car insurance

If you took a bank loan to provide a safe vehicle for your family, the bank requires this coverage to secure their money.

What is it? While Liability helps strangers, Collision fixes your own precious car. It protects you from massive financial stress, regardless of who made the honest mistake. It applies when your car hits another object or vehicle.

What does collision coverage include?

- Your car accidentally hits another vehicle.

- Another vehicle hits your car (even in a cruel ‘hit and run’ case).

- Your car hits a tree, utility pole, street light, or building.

- Your car’s suspension or tire breaks from hitting a deep pothole while safely dropping the kids to school.

- The car loses control and rolls over. (Note: You share a small responsibility called a Deductible—usually $250, $500, or $1000—out of your pocket before the company pays the rest of the mechanic’s bill).

4. Safeguarding Against Nature’s Wrath (Comprehensive): The Silent Guardian of full coverage car insurance

Sometimes your car is safely parked at home, but nature strikes without warning.

What is it? Comprehensive protects your hard-earned money from terrifying physical damages that are not caused by a driving collision. It acts as a safety net against the environment and things completely out of your control, letting your family sleep peacefully at night.

What does comprehensive coverage include?

- Theft: If your car is stolen and never found, leaving you without a ride.

- Natural Disasters: Damage from a tornado, hurricane, car submerged in flood water, or a devastating earthquake.

- Weather Damage: A severe hailstorm causing dents on the car or breaking the glass.

- Fire: The engine catching fire or the car burning in a wildfire.

- Animal Collisions: This is very common in America. Hitting a deer, a bear, or a bird is considered a comprehensive incident, not a collision.

- Vandalism: Someone maliciously paints on your car, breaks the glass, or slashes the tires.

- Falling Objects: A heavy tree branch breaks and falls on your family car. (Note: Your family just chips in a tiny fraction—usually between $100 and $500—and as a beautiful gesture, certain caring states actually mandate replacing a shattered windshield at absolutely zero cost to you).

5. Teamwork for Your Family: How the Three Parts of full coverage car insurance Work Together

Let us look at one final real-life story to see this beautiful teamwork: The Scenario: You are driving safely in heavy snow. Your car slides, hits a parked car, crashes through a wooden fence, and finally stops against a tree.

- Liability: Pays to fix the stranger’s parked car and rebuild their broken fence, keeping your family out of stress.

- Collision: Pays to fix your own broken bumper and engine, so you can drive again safely.

- Comprehensive: Not used here. But if a sudden flood washed your safely parked car away at night, Comprehensive would respectfully pay you the full cash value of your car.

A Secure Future: Why Lenders Ask for full coverage car insurance

- When you finance a car to safely drive your loved ones around, the bank asks for a major promise.

- Many parents feel this requirement is just a trick to add extra expenses to their monthly household budget.

- But the reality is completely different; it is a vital step to protect your family’s future.

- Having full coverage car insurance is simply about making sure that if life throws a curveball, your family isn’t left in a terrible financial storm.

1. Understanding the true value of full coverage car insurance for your family’s safety

- The first step to understanding this promise is realizing that until the loan is paid off, the car is a shared responsibility.

- You get the keys to safely drop your kids at school, but the ownership paper (title) stays with the bank until you proudly pay the very last installment.

- Since the bank kindly invested $20,000 or $50,000 to help you get this family vehicle, they want their money secure.

- This isn’t about being strict; it’s about making sure their investment—and your family’s ride—stays safe in every situation.

2. Protecting our home from financial storms using full coverage car insurance

- Lenders mandate this because they genuinely understand that family budgets have limits.

- A Real-Life Story: Imagine you took a $30,000 car loan and only bought basic protection to save a few dollars for groceries. One day, you make an honest mistake, your car hits a tree, and it is completely crushed (Total Loss).

- The Heartbreak: You get zero dollars for your car, your family has no ride, and you still owe the old $30,000 to the bank.

- Financial records clearly show that in such painful situations, over 90% of people simply stop paying their loan installments because it feels impossible to pay for something that doesn’t exist anymore. This protection permanently eliminates that nightmare.

3. full coverage car insurance helps in keeping the car we love in top shape

- A car isn’t like a house; the moment you drive it off the lot to surprise your kids, its value drops by 10% to 20%.

- The bank’s biggest concern is keeping the car’s value high so it can stay reliable for you.

- An Everyday Example: Suppose a heavy hailstorm leaves 50 dents on the roof, or a stranger breaks your bumper in a dark parking lot. Without proper protection, you might not be able to afford the $3,000 repair bill from your monthly budget.

- You would be forced to drive a broken car, dropping its resale value to scrap rates. This promise ensures a certified mechanic fixes these damages, keeping the car—and your family’s safety—perfectly intact.

4. The caring promise of full coverage car insurance we share with the bank

When you protect a financed car, you must list your bank as the “Loss Payee.” This is just a caring legal promise with three simple rules:

- No Direct Cash: If a $5,000 claim is approved, the check isn’t written directly to you because the bank worries a struggling parent might use that money for rent instead of fixing the car. So, the money goes directly to the repair shop to ensure your car gets fixed.

- Total Loss Payments: If the car is stolen and never found, or burns entirely, the full $30,000 check goes directly to close your loan account so you aren’t burdened by heavy debt.

- Instant Alerts: If you quietly cancel the policy to save money, the insurance company sends an electronic alert to the bank, who then respectfully forces their own expensive protection onto your loan.

5. Securing your family’s daily rides with full coverage car insurance perfectly

- As long as the bank’s name is on the title, this requirement is a strict necessity to keep your family moving.

- Lenders trust you with thousands of dollars for a heavy machine that travels at 80 miles per hour on the highway.

- Therefore, this protection acts as an unbreakable framework that protects the car, eliminates the heavy risk of debt, and ensures the bank’s money is absolutely safe.

6. A final thought on absolute peace of mind with full coverage car insurance

- Ultimately, fulfilling the bank’s requirements simply means you can drive to work or take your kids on a weekend vacation without worrying about the “what ifs.”

- By combining these layers of care, we ensure that heavy financial burdens are lifted off our shoulders, letting us focus entirely on our children’s happiness and our secure future!

How Your Home Address Changes the Cost of full coverage car insurance

In our honest opinion, the exact place where your family sleeps every night has a massive impact on your monthly bills because living on busy streets with too many vehicles, facing scary storms, or living in towns where people argue a lot over tiny bumps makes protecting your family car much more expensive, which is why households across different places pay vastly different amounts as shown in the simple list below.

1. The big price difference for full coverage car insurance

- When looking at the numbers, it is our opinion that everyday families pay vastly different amounts to drive safely.

- We found a huge money difference between buying a car with your own savings versus asking helpers for a loan.

- If a father buys a car using pure cash from his piggy bank, the law only asks for a tiny safety promise.

- This basic promise is very cheap, costing a family only $61 to $68 every month.

- Over a whole year, this keeps the family’s cost very low, between $727 and $820.

2. How borrowing money makes full coverage car insurance so expensive

- But when kind helpers lend you money for a family car, they force you to buy a complete safety net.

- This strict rule makes your monthly bill jump super high, to about $216 to $244 a month.

- For the whole year, a family has to pay a massive $2,575 to $2,932 from their hard-earned savings!

- This means that asking for help to buy a car makes your safety bill jump up by a giant 250%.

3. Our honest opinion on full coverage car insurance

- In our honest opinion, you should always remember this giant extra cost before buying a shiny new car.

- Before you make a promise to the helpers, always count these extra monthly bills first.

- Doing this simple math makes absolutely sure that your children’s grocery money stays perfectly safe!

Family Safety and full coverage car insurance: Protecting Our Hard-Earned Peace

- Raising a family in the USA means counting every single dollar to ensure our children are safe and happy.

- An Everyday Example: Imagine a loving father, David. He buys a safe SUV for his kids and gets the mandatory policy just to leave the dealership.

- Next month, to afford his daughter’s school books, he quietly drops his full coverage car insurance to a cheaper ‘Minimum Liability’ plan.

- While David thinks this is a harmless shortcut, doing this with a financed car is a dangerous breach of trust.

- Let’s see how this single mistake turns everyday numbers into a real household nightmare.

1. full coverage car insurance alerts: Why the digital system reacts instantly

You might wonder, just like David did, “How will the bank ever find out?”

In today’s connected world, there is no hiding. The insurance companies are directly linked to the state’s DMV (Department of Motor Vehicles) and your lender (the Lienholder).

- The Automated Alarm: Because the bank kindly financed your family car, they are listed as the “Loss Payee” on your policy.

- The Trigger: The computer system instantly sends a red alert to your bank if you miss a payment.

- Strict Safety Net: It also alerts them if you increase your out-of-pocket deductible limit beyond their rules (for example, over $500).

The bank immediately knows the family is driving unprotected on busy highways.

2. The warning letter when full coverage car insurance is quietly removed

The bank doesn’t want to take your car away. They genuinely want your family to succeed.

By law, they respectfully give you a second chance to fix this honest mistake.

- A Caring Notice: The compliance department mails you a Warning Notice. They gently ask you to restore your full coverage car insurance to keep your family safe.

- A Real-Life Moment: Imagine a stressed mother reading this letter at the family dinner table. She is given a fair window of 15 to 30 days to correct the issue.

- The Simple Fix: You simply need to fax or email them your ‘Declaration Page’ as proof of safety.

Ignoring this warning is where a family’s financial heartbreak truly begins.

3. The massive bills replacing your safety shield today

If you can’t provide proof in time, the bank legally buys a policy for you.

This is called Force-Placed Insurance or CPI (Collateral Protection Insurance). Here is how these numbers quietly destroy a peaceful home’s budget:

- Exorbitant Bills: A family might normally pay $200 to $250 a month for proper full coverage car insurance.

- The Shocking EMI: CPI is incredibly expensive. It causes your regular loan installment (EMI) to jump by $50 to $150.

- A Painful Example: A manageable $400 EMI easily becomes a stressful $550 or $600. That extra money is stolen directly from the kids’ grocery or medical budget.

- Zero Protection: CPI only protects the bank’s car. It won’t pay a single dollar for a stranger’s medical bills if you hit them.

- Legal Danger: They can sue you personally, putting your hard-earned bank accounts and future paychecks (garnished wages) at massive risk.

- The Debt Trap: Imagine a hardworking parent trying to pay off their remaining $15,000 loan.

- Unfair Additions: When the bank forces a $2,500 annual CPI policy on them, their debt unfairly jumps to $17,500.

- Interest on Insurance: To make matters worse, the 7% or 10% interest rate (APR) applies to the insurance too, trapping the family in a vicious cycle.

4. Losing your family’s daily ride and credit score

The heavy weight of these new numbers eventually breaks the household budget completely.

- The Breaking Point: A parent who couldn’t afford their normal premium for full coverage car insurance suddenly finds it impossible to pay a new $600 CPI loan bill.

- The Repo Man: When payments stop, the loan defaults.

- A Heartbreaking Example: Imagine waking up at 7 AM for the school drop-off, only to find a ‘Repo Man’ has quietly towed the precious family car from your driveway.

- Extra Costs: The kids are left crying without a ride. The bank sells the car at an auction, adding the towing costs right back to your debt.

- The 7-Year Stain: This repossession is a devastating blow. It ruins your credit score for 7 full years.

- A Blocked Future: Because of this single mark, getting a future car or home loan is nearly impossible. Even kind landlords might refuse to rent your family a safe home.

5. Securing your family’s future with full coverage car insurance

- Dropping your full coverage car insurance to save a few dollars is a disastrous gamble.

- The painful CPI process raises your bills and leaves you legally naked on the road. It ultimately ends in a 7-year financial stain.

- If the premium ever feels too heavy, please consider a loving alternative.

- A Better Example to Follow: Instead of breaking the rules, a wise parent might trade their expensive SUV for a reliable, cheaper used car.

The most caring choice for your family’s future is to adjust your lifestyle safely. Never break this vital safety rule.

The Hidden Rule: Why Banks Limit Your Family’s Upfront Costs

- When a parent buys a safe vehicle in the USA, they usually think they can decide their own safety rules.

- This is completely true if you buy an older car with pure cash.

- But when a bank helps you pay for that precious family car, your rights quietly change.

- The biggest hidden rule is that lenders set a strict limit on your upfront personal share for full coverage car insurance.

- Let’s explore why banks step in and how it secretly affects a family’s grocery budget.

1. full coverage car insurance and how paying from your own savings works

In simple terms, a ‘deductible’ is the upfront money you must pay from your own savings before the company steps in to help.

It mostly applies when you accidentally hit something, or if severe weather damages your car. (Note: There is no personal cost when paying for a stranger’s medical bills).

- A Real-Life Example: Imagine a father accidentally bumps into a fence, and the repair shop prints a $3,000 bill.

- The Family Burden: If his upfront personal share is $500, he must pay that $500 from his children’s savings first.

- The Relief: Only then will his full coverage car insurance step in and pay the remaining $2,500.

2. Balancing family needs with full coverage car insurance to save grocery money

There is a simple truth to remember: taking a bigger money risk yourself makes your monthly bill cheaper.

In these expensive times, every hardworking American parent wants to reduce their monthly expenses.

- A Parent’s Mindset: Many safe drivers think, “I drive carefully with my kids, so I won’t ever crash.”

- The Saving Trick: To save money on their full coverage car insurance, they try to raise their upfront personal share to $2,000 or $2,500 online.

- The Hope: They hope this trick will cut their monthly bill in half, leaving more money for school supplies and food.

3. Why the bank stops you from taking bigger money worries

This is exactly where the bank steps in and stops your money-saving plan.

Because the bank’s name is on the ownership papers, you simply cannot choose this money limit freely.

- Big Bank Rules: Big names like Chase Auto, Bank of America, and Wells Fargo are very protective of the money they lent you.

- The Hard Limit: They demand that your personal upfront share must never exceed $500.

- Small Exceptions: Some special local credit unions might kindly allow a limit of up to $1,000, but not a single dollar more.

If you secretly pick a $2,000 limit, the bank treats it as broken trust. They will immediately punish your family by forcing their own incredibly expensive backup plan onto your car loan.

4. The heartbreaking truth behind the $500 or $1000 limit

Banks do not create these rules to hurt parents; they just look at harsh everyday realities.

- The Cash Problem: The bank knows the average family does not have thousands in emergency cash sitting around.

- A Painful Reality: Imagine a mother needing a sudden repair with a $2,000 upfront limit. She cannot easily pull $2,000 cash out of her purse without skipping rent.

- Driving Broken Cars: Without that cash, parents won’t ask for repair help. They will keep driving their kids in an unsafe car with a smashed door.

- Protecting the Money: A broken car’s selling value drops to half overnight. This scares the bank, as the car is the main security for their money.

If a struggling family stops paying their monthly car bill, the bank has to take the car away. Selling a broken car to strangers causes a massive money loss for the bank.

5. Managing your family budget alongside expensive full coverage car insurance

- This strict limit set by the bank is one of the heaviest hidden costs for a household.

- Because you are not allowed to choose a cheaper $2,000 limit, you are forced to stick with the $500 rule.

- This forces your monthly bill for full coverage car insurance to remain permanently high.

- Many parents carefully calculate their monthly car payment but completely forget this strict safety rule.

- When they realize their mandatory full coverage car insurance costs almost as much as the car itself, their monthly budget is completely ruined.

- This rule ensures a family can fix their car in an emergency, but it certainly makes daily life very expensive!

The Biggest Family Secret: Why Your Neighbor Pays Less for the Same Car

- Imagine finding out that your neighbor pays exactly half of what you pay every month for the exact same family car.

- How is that even possible?

- When a bank helps you buy a vehicle, they simply ask you to protect their money.

- But nobody tells you the secret rules that change the cost of your mandatory full coverage car insurance.

- Let us look at how your everyday life choices directly increase or decrease your monthly grocery budget.

1. full coverage car insurance: Why every family pays a different price

In our country, companies look at your past money habits to decide your monthly bills.

- A Great Reputation: If you always pay bills on time (a score over 750), your family might pay just $120 a month.

- Doing Okay: A good reputation (scores of 670-749) keeps things easily affordable at about $125 a month.

- The Heavy Burden: But if a father had tough times and a poor score (300-579), his bill unfairly jumps to $313 a month.

- A Painful Example: This is a massive 160% jump for the exact same protection!

A hardworking parent with past money struggles might lose $2,300 extra every single year.

That is money directly stolen from their children’s college savings, just to pay for their full coverage car insurance.

2. How your past choices change full coverage car insurance for your household

Companies also look deeply at how carefully you drove in the past.

- A Safe Drive: A clean history keeps your everyday family bill around $215 a month.

- An Honest Mistake: If a mother accidentally bumps another car, the bill jumps to $310 a month (a 44% increase).

- A Dangerous Choice: Driving after having drinks pushes the bill to a painful $377 a month (a heavy 75% penalty).

Even a tiny mistake can steal your extra grocery money for 3 to 5 long years.

A serious mistake will completely ruin a family’s budget for 10 full years!

3. The expensive reality of having young drivers at home

Letting your kids drive the family car is a proud moment, but it is incredibly expensive.

- Adult Bills: A safe adult parent (aged 25-54) usually pays around $215 a month.

- The Teenage Cost: Adding a young adult (aged 18-24) to your full coverage car insurance pushes the monthly cost to a shocking $497 to $537.

- A Real Example: An 18-year-old college student costs almost two and a half times (2.5x) more than their 40-year-old parents.

Companies know teenagers get easily distracted on the road.

Thankfully, these heavy bills finally start to drop once the child blows out 25 birthday candles.

4. Choosing the best safety partner for your peace of mind

This is the one choice where parents have complete control to save their hard-earned money.

Every local office uses a different secret rule to decide your price for full coverage car insurance.

- Travelers: Often very kind to wallets, asking for just $97 to $107 a month.

- State Farm: Very friendly for families, usually asking for $121 to $125 a month.

- Progressive: Another solid everyday choice, costing around $125 to $151 a month.

- Allstate: Slightly higher for households, falling between $161 and $196 a month.

- A Wise Trick: Never just say yes to the very first price at the car shop.

Asking around at different places can save a family hundreds of dollars every single year.

5. Protecting your hard-earned family money with full coverage car insurance

- While the everyday cost sits around $216 a month, your actual bill depends entirely on your daily choices.

- This safety net protects your car from unexpected crashes, sudden thefts, and bad storms.

- If a parent secretly drops this complete protection, the bank will force their own costly backup plan on the car.

- They will add this huge expense to your monthly car bill, pushing your peaceful home into heavy debt.

- To avoid a sudden financial crisis, always keep your family safe with full coverage car insurance.

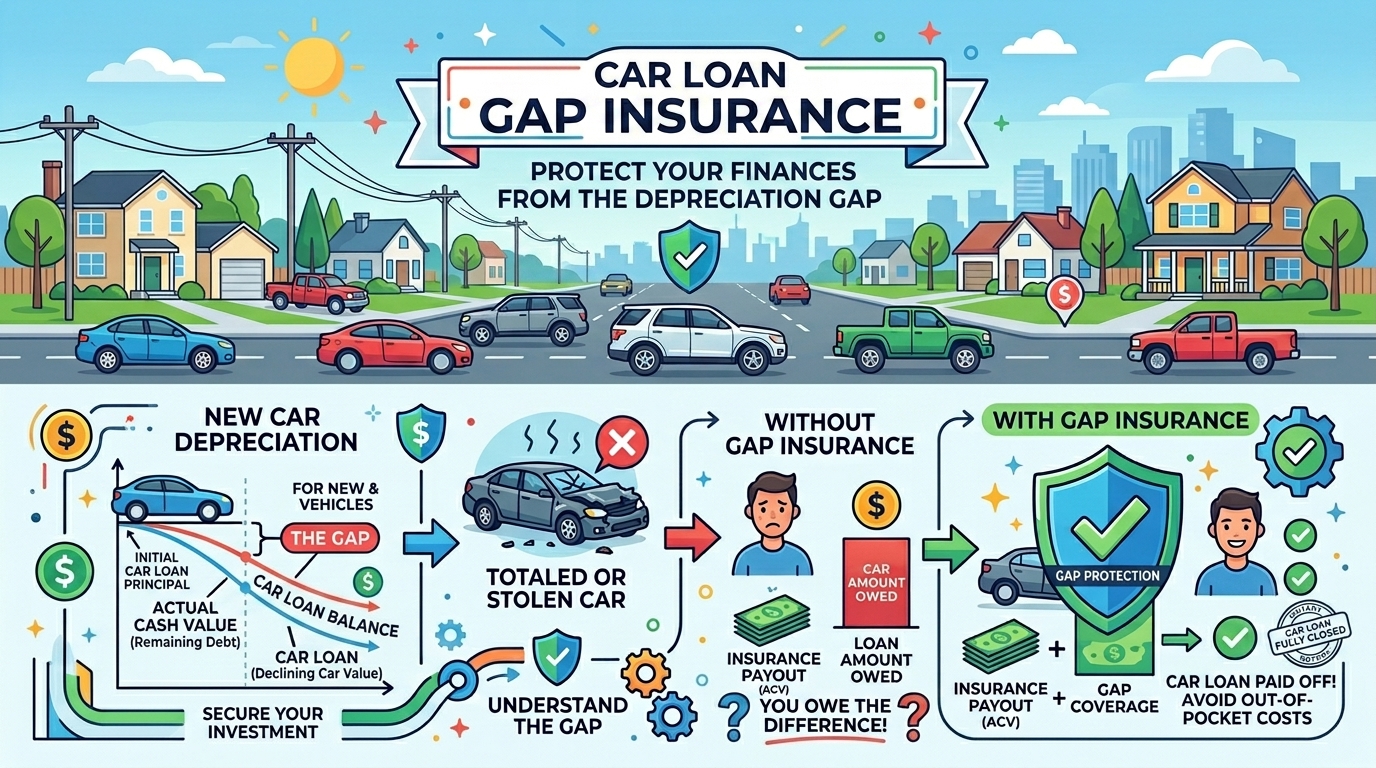

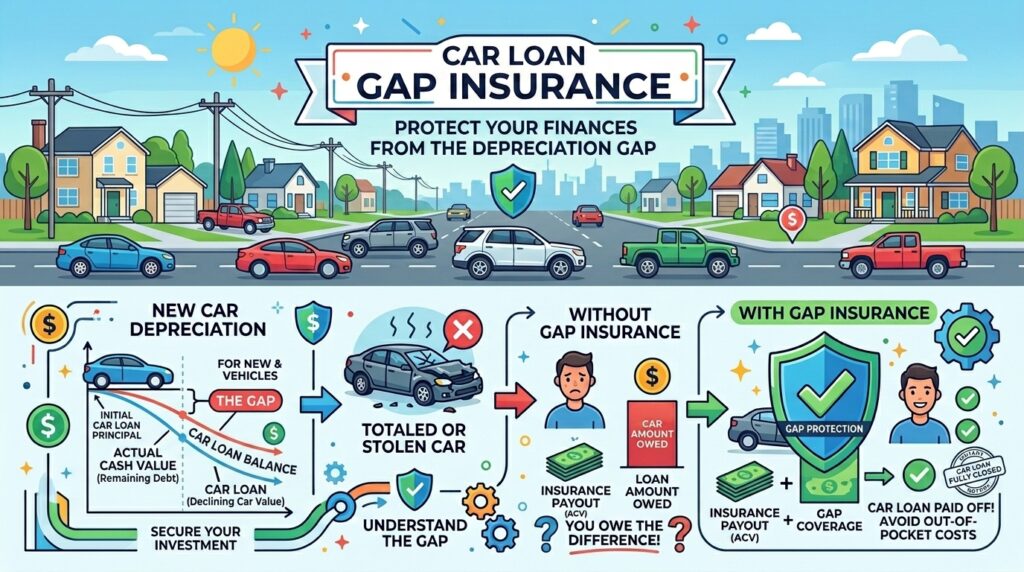

Gap Insurance: Why your everyday full coverage car insurance needs a friend

When you buy a brand-new car, its real-world price drops the very second you drive it home to your family.

Because of this fast drop, your standard policy only pays what the car is worth today, not the actual amount you borrowed from the helpers.

1. A real family story about a $35,000 money trap

- Imagine a loving father buys a safe new car for $35,000 and agrees to a 10% borrowing fee.

- Just one year later, the car’s real price sadly drops to just $25,000.

- But because he is paying slowly, he still owes a heavy $32,000 to the kind people who lent him the money.

2. The scary $7,000 gap despite having full coverage car insurance

If the car gets completely ruined in a bad storm, the company only gives the lenders $25,000.

The poor father is now forced to pay the missing $7,000 completely out of his own pocket.

He has to take this huge amount from his children’s savings, even though the family has no car left to drive!

3. Gap Insurance steps in like a true friend

- This is exactly where ‘Gap Insurance’ steps in to completely save the family’s peace of mind.

- Instead of the father emptying his pockets, Gap Insurance kindly pays that frightening $7,000 for him.

- It clears the heavy burden completely, keeping the family’s savings safe for groceries and school books.

4. When to add Gap Insurance to your full coverage car insurance

- Caring money teachers say you really need Gap Insurance if you couldn’t pay a big 20% chunk of cash on the very first day.

- You also absolutely need it if you promised to pay slowly for 60 to 84 months, or if you bought a really fancy ride.

- Ultimately, your main policy fixes the car, but Gap Insurance protects your family’s hard-earned money and future!

A Loving Parent’s Guide to full coverage car insurance

Question 1: Why do the people who lent us money make us have this rule?

Answer: They ask us to carry full coverage car insurance so they know their money is completely safe if our family car ever gets badly hurt or lost.

Question 2: How does this promise actually protect our family?

Answer: It pays the doctor if someone gets an ouch, fixes our car after a bump, and gets us a new ride if ours washes away in a bad storm.

Question 3: Can we break this rule to save our grocery money?

Answer: No, we gave our word to keep our full coverage car insurance every single day until we pay back every last penny we owe.

Question 4: Will the money helpers know if we secretly break our promise?

Answer: Yes, a tiny secret message flies to them the exact same second we try to break our word!

Question 5: What happens if we do break this big rule?

Answer: They will punish our family by forcing a giant, painful penalty onto our monthly expenses, taking away our hard-earned money.

Question 6: Does their giant penalty help us if we make a mistake on the road?

Answer: No, it leaves our family completely alone with zero help, only caring about the money we owe them.

Question 7: Can we promise to pay a big chunk of money ourselves so the monthly cost is tiny?

Answer: No, they know everyday families don’t have thousands hidden under the mattress, so they only let us promise a tiny bit.

Question 8: Why does the sweet family next door pay less than us?

Answer: Families who always keep their promises and pay on time are given much cheaper full coverage car insurance as a lovely reward!

Question 9: Why is the cost so big when an 18-year-old child drives?

Answer: Young kids are still learning how to steer, so they make more little bumps, which makes keeping them safe a lot costlier.

Question 10: How can we make this monthly cost as tiny as possible?

Answer: By driving super carefully, keeping our promises on time, and asking around town to find the sweetest deal on our full coverage car insurance.