Car Loan Gap Insurance: The Ultimate Guide Before You Buy

Will You Still Have to Pay Installments on a Junked Car After an Accident? Know the Family Truth of car loan gap insurance

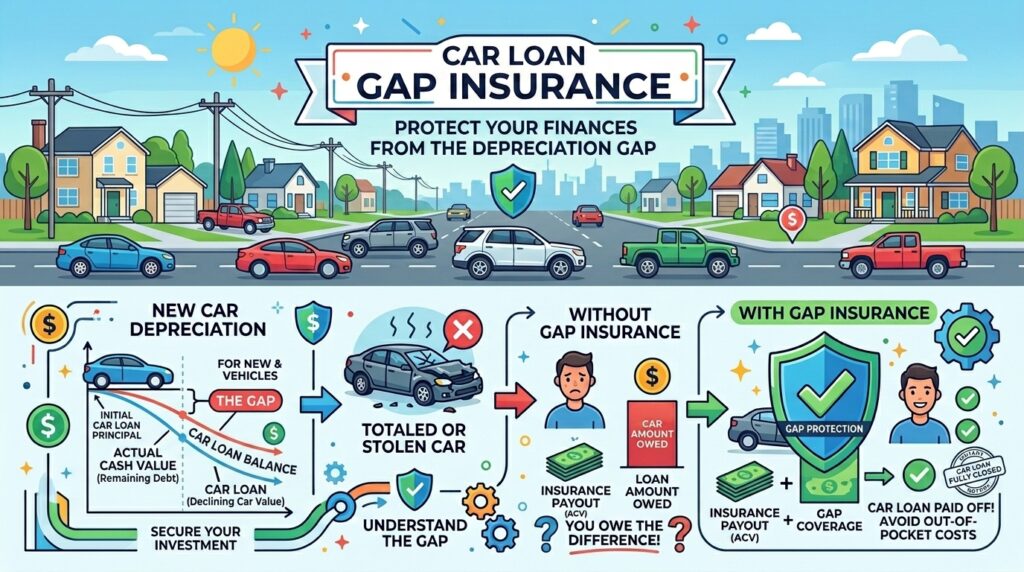

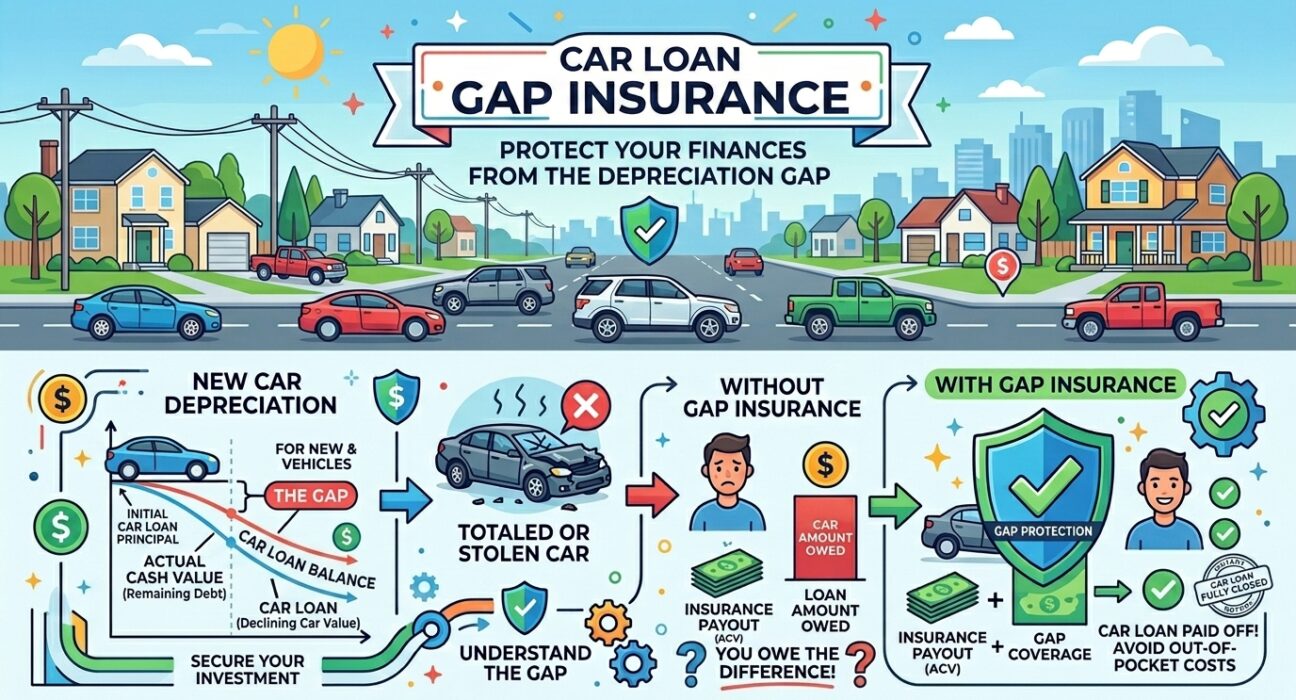

We all dream of a new car for our children’s safe travel and our family’s happiness. We invest our blood and sweat earnings for this. But have you ever thought about what would happen if tomorrow that car falls victim to an accident or gets stolen? The scariest truth is that despite having no car in your driveway, the bank will collect every single penny of the remaining loan from you! This is exactly where car loan gap insurance saves your family’s lifelong savings and peaceful sleep from being snatched away.

1. What is this safety shield and when do you need it?

Buying a car is a very big financial decision. When you bring a car by taking a loan from the bank, an unknown risk falls upon the family.

- The truth of incomplete safety: Your ordinary car insurance only pays the price (the amount it would sell for in the market) of the exact day the accident happened. It absolutely does not care how big of a loan you took from the bank for your children’s happiness.

- The crisis of difficult times: If after the accident the bank’s loan is more than the car’s remaining value, you will have to pay all that remaining money by cutting it from your home’s groceries or your children’s fees.

- True companion: A proper car loan gap insurance saves you from this terrible debt. It completely fills the ditch between the car’s price today and your remaining loan, so that no harm comes to your family.

2. How does the price of a car fall? (Simple household math)

Understand with a family example: when you bring a new toy for the children, it becomes old as soon as the packet opens and its price decreases. A car is also not land or gold whose price will increase, it starts becoming cheaper the moment it leaves the showroom:

- The first day: The moment you step out of the showroom with your family, the car’s price immediately drops by up to 10%.

- The first year: By your first long vacation with the children, the car loses 20% of its price.

- Future years: In three years it becomes 40% cheaper and in five years it becomes almost 60% cheaper.

- The bitter truth: When you initially bring a car by paying very little money from your pocket, the car’s price falls much faster than the speed of you paying off your loan.

3. A real-life example: How does this work?

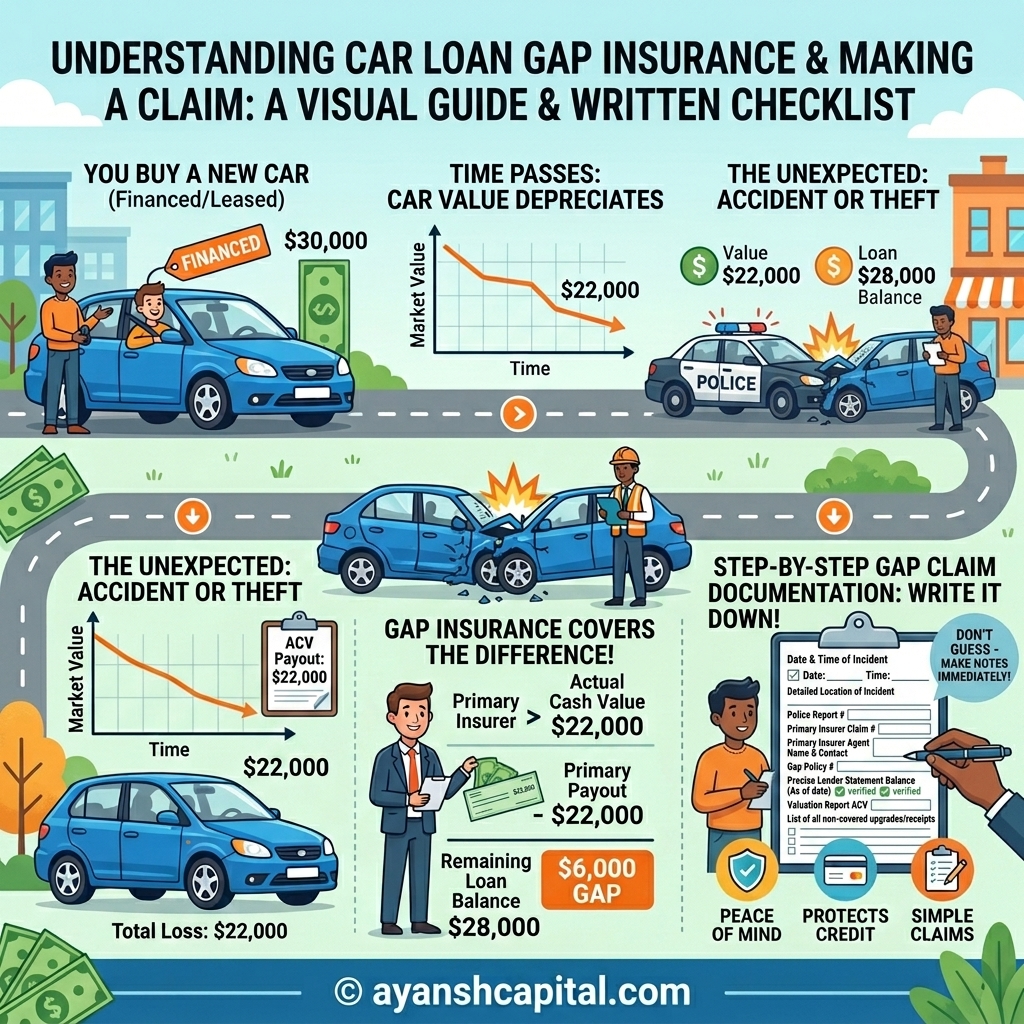

Suppose you bought a $35,000 car for the family, in which you paid only $1,000 from your pocket and took a $34,000 loan from the bank.

- The nightmare 6 months later: God forbid, 6 months later the car gets into a very bad accident and gets completely destroyed.

- The bank’s debt on you: In the initial months, your money only went into paying the bank’s interest. Therefore, you still have a bank debt of $32,500 remaining on you.

- The bitter truth of the insurance company: Because the car has become 6 months old, the insurance company will hand you a check of only $28,000.

- The heavy difference in debt: Now the bank’s $4,500 ($32,500 – $28,000) is left. The bank will send you a notice to pay this money from your pocket.

- A sigh of relief: Paying this $4,500 without a car can completely ruin your home’s budget. But if you had car loan gap insurance, this plan would have paid the full $4,500 and your family would have remained completely debt-free.

4. Does this also pay the initial expense that goes from your pocket at the time of the accident?

When an accident happens, often according to the rule, you have to pay an initial expense of $500 or $1000 from your pocket.

- The common rule: In most cases, this plan does not cover this initial expense given by you at the time of the accident. It only fills the difference between the bank’s loan and the car’s price.

- A smart step: Some specific companies include this in their responsibility too. Therefore, to save your family’s money, read the paperwork absolutely carefully before signing them.

An elder’s firm advice: For the golden future of your children and the peace of your home, whenever you buy a new car by paying less money initially, definitely consider car loan gap insurance as an essential protector for your family. This is not merely a piece of paper, but rather it stands like a shield like a true friend during your bad times.

Have You Ever Wondered How car loan gap insurance Saves Your Family’s Hard-Earned Savings?

If your brand-new car gets totaled on the very first day, your home could face a sudden financial nightmare. This safety net steps in so you never have to pay out of pocket for a car that no longer sits in your driveway.

5 Family Situations Where car loan gap insurance is 100% Essential

Not every family needs this. If you paid entirely in cash, skip it. But to protect your household from unexpected storms, these 5 situations absolutely require this safety net:

- 1. Paying Less Than 20% Upfront: The moment your kids hop into the new car, its price drops by 10%. If you paid 0% or 10% from your pocket, you instantly owe the bank more than the car is worth. A good car loan gap insurance protects your grocery money from this sudden risk.

- 2. A Loan of 60 Months or Longer: To keep bills low, parents often take 72-month or 84-month loans. Because early payments mostly go to bank interest, your debt shrinks slowly while the car ages fast—a dangerous trap for your hard-earned wealth.

- 3. Leasing the Family Car: You don’t own a leased car. If it gets stolen, the company still wants their full money. Almost all leases require this coverage to prevent a sudden tragedy from wiping out your savings.

- 4. Carrying Over Old Car Debt: Trading in an older car that still has a loan bigger than its trade-in value? Dealers add this old “ghost debt” to your new loan, creating a huge hole between what you owe and what the new car is worth.

- 5. The Car Loses Value Too Fast: Certain luxury or electric vehicles can lose over 30% of their value before your child finishes a school year. If the price drops this fast, this net ensures a total loss doesn’t destroy their college fund.

Where to Buy car loan gap insurance? (Dealerships vs. Your Insurance)

Here is a simple, honest breakdown to keep your family’s wealth safe.

Option A: Buying from the Dealership (The Costly Trap)

- The Heavy Cost: Dealerships charge a massive one-time fee of $500 to over $1,000. That money could pay for a beautiful family vacation!

- The Interest Trap: They add this $1,000 fee into your car loan. You pay 6% to 10% interest on it for the next 5 to 7 years.

- Hard to Cancel: Getting your refund back takes confusing paperwork and months of stressful waiting.

- Our Opinion: This drains your household wealth. Avoid it if possible.

Option B: Buying from Your Insurance (The Smart Family Choice)

Trusted companies let you add this directly to your policy.

- The Honest Cost: It costs just $20 to $60 per year (about $2 to $5 a month)—less than a kid’s fast-food meal!

- No Hidden Interest: You pay it with your normal bill, so you don’t pay a single cent of bank interest to greedy lenders.

- Easy to Cancel: Once you owe less than the car is worth, a quick five-minute phone call cancels it.

- Our Opinion: This is the safest, smartest choice for any household looking for car loan gap insurance.

Important Rules by Provider

When buying through standard providers, remember their specific rules so your family isn’t caught off guard:

- Progressive: Caps the payout at 25% of the car’s actual value. For example, if you owe the bank way more than that, you might still have to use the money saved for your family’s emergency medical fund or home repairs to cover the remaining debt.

- GEICO: Only for brand-new cars where you are the very first owner—perfect if you are celebrating a new baby with a fresh, safe family minivan!

- State Farm: Offers a feature that works just like standard car loan gap insurance, but is tied directly to their banking family to help you manage all your household bills easily in one place.

An Elder’s Honest Advice: If a dealer forces you to buy their expensive car loan gap insurance to approve your loan, accept it just so you can finally bring your kids home in a safe car without a stressful argument.

But a few days later, activate your own agent’s $5-a-month coverage. Cancel the dealer’s plan and send that massive refund straight to your loan balance. This smart move pays off your debt faster, freeing up money for your family’s daily needs!

The Loan Risk Factor: When Does Your Family Need car loan gap insurance?

In any household budget, there is a simple math rule that decides if your family is in a risky financial spot. It is the gap between what you owe the bank and what the car is actually worth today. Banks use this math to decide how much help they will give you if the worst happens.

- The Simple Household Math: Divide your total loan by the car’s current price, and multiply by 100.

- A Real Family Example: Imagine you finally bought that spacious, safe minivan for family road trips. It is worth $30,000 today. But after adding taxes and the leftover debt from your old car, your actual loan sits at $36,000. That means you owe 120% of the car’s worth.

- Why This Matters: That invisible 20% difference is a dangerous financial cloud hanging over your home. If an accident happens, a good car loan gap insurance acts as a hero, stepping in so you don’t have to empty your kids’ college savings to pay for a car you can no longer drive. Once your hard work pays down the loan enough, cancel the plan and spend that extra money on a nice family dinner!

Company Rules: Not All car loan gap insurance is the Same

Not every company offers unlimited help. If you carried old debt into your new family car, companies set strict boundaries. Anything beyond that boundary comes straight out of your pocket! Let’s look at how this impacts real families:

- Allstate: Often sold at the dealer, they cover up to 150%. Imagine you bought a reliable $20,000 car for your teenager’s first drives to school. They will protect your family’s savings even if your loan stretches up to $30,000.

- Farmers Insurance: They strictly cover a gap up to 25% of the car’s current value. If a bad storm totals that $20,000 car, they only help with $5,000. If your actual gap is $7,000, you must pay the remaining $2,000 yourself—money that could have paid for your family’s entire summer vacation!

- USAA (For Military Families): A beautiful benefit for our brave military households. Instead of just paying the exact debt, they actually give you 20% more! If the crashed car was worth $15,000, USAA sends an extra check for $3,000. You can use this blessing to buy a sturdy, safe replacement car to bring your newborn baby home in.

The Harsh Truth: What Your car loan gap insurance Will NEVER Cover

Many parents mistakenly believe this safety net wipes away all car debt no matter what. That is a dangerous myth. After an accident, the bank will strictly refuse to pay for these things:

- Your Initial Expense: If your main coverage requires a $500 out-of-pocket expense before they help, the bank simply takes this out of your final check. You might have to use the money saved for your daughter’s braces to cover it.

- Missed Payments: If times got tough and you skipped a car payment to buy winter coats for the kids, the bank won’t forgive that penalty. You must pay it from your own savings.

- Expensive Extras: If you added a $2,500 extended protection plan to keep the car running smoothly for family trips, car loan gap insurance will absolutely not pay for it. You must call that specific company for a refund.

- Everyday Breakdowns: This safety net only opens if the car is completely destroyed or stolen. If the engine suddenly blows while driving to grandma’s Thanksgiving dinner, it pays nothing.

Getting Money Back from Your car loan gap insurance to Help Your Budget

If you paid a massive $800 or $1,000 upfront at the dealership, you have a legal right to get your unused money back to help with household expenses.

- When Can You Claim It? You can get your money back if you work hard to pay off your loan early, sell the car, or move your loan to a new bank with better rates.

- Step 1: Get the Proof: When your loan hits zero, print a ‘Paid in Full’ letter online. Celebrate—your family is officially debt-free!

- Step 2: Make the Call: The dealer won’t do this automatically. Call their finance office to ask for your money back. (You will need to tell them the exact miles on the dashboard).

- The Joy of Simple Math: If you paid $1,000 for a 60-month plan but sold the car at 30 months, you get about $500 back in the mail. Imagine the relief of that surprise $500 check—it can fill your fridge with healthy groceries for weeks!

- The Monthly Plan Benefit: If you secure your car loan gap insurance through a monthly provider (like GEICO or State Farm), there is no stressful refund process. A quick five-minute phone call to your agent instantly lowers your family’s monthly bills, putting cash right back into your pocket!

The Sudden Nightmare: Could One Accident Wipe Out Your Family’s Savings?

Have you ever wondered if your savings would survive if your car was totaled tomorrow? Without the right protection, a single accident could turn your family’s financial dreams into a nightmare. Here is how to take control.

1. What to Do After a Crash Involving Your car loan gap insurance

If a terrible accident shatters your family car, hug your kids first and take a deep breath. To protect your home’s finances, follow this path:

- Make the Calls: Call the police, then your main insurance. If fixing your trusty $20,000 family SUV costs $16,000 (that’s 80%), they will declare it completely destroyed.

- Activate Your Shield: Call the bank immediately. Then, call your provider to activate your car loan gap insurance to save your hard-earned life savings from being wiped out.

- Where the Money Goes: The main check goes straight to the bank. If that check is too small, your extra safety net pays the rest. This frees your family from a massive burden, keeping your future secure.

2. The Low Price Trap: Why car loan gap insurance is Essential

When the company tells you the car is gone, they will send a price report. But beware—it is often thousands of dollars lower than what you’d need to replace your vehicle.

- The Sneaky Computer Math: They use cold programs that price your beautiful family car like a beaten-up vehicle on a dealer’s back lot.

- The Danger: A low price leaves you with a huge, unfair bank debt. This is exactly why having proper car loan gap insurance is a lifesaver; it catches your family when the main company tries to pay you only a fraction of what you actually need.

3. Fighting Back Before Relying on Your car loan gap insurance

Never accept their first low offer. Fight for your household’s money using these simple steps:

- Check Their Homework: Did they forget the $1,000 leather seats that easily wipe away spilled juice? Send them proof to instantly raise the money they owe you!

- Show Them Reality: Go online and find 3 to 5 identical cars for sale near your home. Email these to the company to prove it actually costs $20,000 to replace your family’s ride.

- The Result: Forcing them to be fair reduces the heavy lifting your car loan gap insurance has to do, ensuring it only covers what it truly should.

4. The Fairness Rule: A Secret Weapon Alongside car loan gap insurance

If the company remains stubborn, use a hidden right in your paperwork called the “Appraisal Clause.”

- Calling in an Honest Expert: You pay a fee (around $300 to $500) to hire an independent car expert. They write a true report of your car’s worth. The insurance company must then hire their own expert to compare notes.

- The Win for Your Family: In 95% of cases, the insurance company finally gives up and offers a much higher, fair price.

- A Parent’s Caution: Only use this secret weapon if the company is cheating you out of $1,500 or more. If the difference is just $500, paying the expert will eat up money meant for your children’s winter clothes! A fair fight ensures the main company pays their share, letting your car loan gap insurance finish the job of keeping your home debt-free and stress-free.

Unlocking Extra Family Cash: How to Easily Afford Your car loan gap insurance

Imagine finding an extra $500 in your bank account to spend on your family’s summer vacation just by making a quick phone call. Your legally required “full coverage” auto policy might be quietly draining your monthly budget, taking away money meant for your loved ones.

But you don’t have to overpay just to keep your family safe on the road. Here are five simple, everyday ways to lower your bill by 20% to 30%. This extra cash makes it much easier to pay for your car loan gap insurance without ever feeling financially stressed.

1. Keep a Little Emergency Cash on Hand

When you agree to pay a slightly higher out-of-pocket amount (your deductible) if you get into a fender bender, insurance companies lower your monthly bill.

- For example, moving your deductible from a pricey $250 or $500 up to $1,000 can drop your premium by 15% to 20%. Just keep that $1,000 safely tucked away in a savings account for emergencies!

- Please check your auto loan paperwork first, as some banks only allow a maximum $1,000 deductible. Also, remember that a standard car loan gap insurance policy will not cover this $1,000 for you if your car is completely totaled.

2. Let Your Safe Driving Pay You Back

If you are a careful parent who stops gently at red lights and ignores your phone while driving, let your insurance app prove it. The savings are so big that adding car loan gap insurance to your life feels practically free.

- Programs like State Farm’s Drive Safe & Save or GEICO’s DriveEasy can lower your bill by 25% to 30% just for smooth, safe driving.

- Progressive’s Snapshot saves safe drivers an average of $231 a year.

- USAA’s SafePilot gives our military families up to 30% off just for driving carefully on their daily commutes.

3. The Simple Renters Policy Trick

Did you know that signing up for a basic $10 to $15-a-month renters policy can shrink your car insurance bill, even if you don’t own a home?

- Insurance companies love when you bundle your policies together. Grouping a cheap renters plan with your auto plan usually gives you a solid 10% to 15% discount on your car.

- Often, the money you save on your car is much bigger than the $10 cost of the renters policy itself! It literally puts free grocery money back into your pocket. Plus, some companies let you bundle your car loan gap insurance right into this package for even easier savings.

4. Pay Your Bills on Time to Lower Your Rate

In almost every state (except CA, HI, MA, and MI), insurance companies look at your credit history to decide your price.

- Families with poor credit are often charged a massive 115% more. Unfortunately, having bad credit is also exactly how pushy dealers trap parents into buying overly expensive car loan gap insurance at the dealership.

- The Simple Fix: Keep your credit card balances low and pay your bills on time. As soon as your credit score improves from ‘Fair’ to ‘Good’, call your agent to ask for a lower price. This frees up your cash so you can easily buy a smart, low-cost car loan gap insurance policy directly from them.

5. Ask for Everyday Discounts You Might Be Missing

Don’t leave free money sitting on the table. Ask your agent about these simple, everyday discounts:

- Pay All at Once: If you pay for your 6-month policy all at once instead of monthly, companies usually drop their sneaky fees and give you a 5% to 10% discount.

- Your Job Matters: Are you a hardworking teacher, engineer, or registered nurse? Major companies offer up to 8% off just to say thank you for the work you do.

- Take a Quick Class: Spending an hour on a $20 to $30 online defensive driving class on a Sunday afternoon can lock in another 5% to 10% discount for the next three years.

Lowering your main bill makes protecting your family’s vehicle with car loan gap insurance completely manageable. It ensures you never have to face a massive car debt alone, letting your coverage do its job of keeping your home secure and stress-free!

A Parent’s Peace of Mind: Your True Financial Shield

Buying a new car for your family should be a joyful moment, not a financial trap. The truth is, cars lose their value quickly, often leaving families owing the bank much more than the car is actually worth. Having car loan gap insurance is a wonderful safety net to protect your home’s savings. The real danger isn’t the coverage itself, but the overpriced fees pushy dealers try to charge stressed parents.

By knowing exactly what you owe, understanding what your plan covers, and learning how to fight for a fair price, you take the power away from the big banks and put it right back into your family’s hands.

Three Simple Steps to Protect Your Family’s Wallet

Before signing any heavy paperwork, take these three simple steps to protect your hard-earned money:

- Do the Kitchen Table Math: Before buying, sit down and compare the car’s price to your total loan. If you owe more than the car is worth, securing car loan gap insurance is an absolute must to keep your savings intact for things like your kids’ education.

- Call Your Agent First: Call your current home or auto insurance agent before you ever step foot on the car lot. Adding affordable car loan gap insurance directly through them is the smartest way to skip the dealer’s heavy, hidden fees.

- Get Your Money Back: If you work hard to pay off your loan early, or if you sell the car, do not leave your money behind! Call the dealer to claim a refund for any upfront car loan gap insurance you purchased. That is your family’s money, and it belongs in your pocket!

We Want to Hear Your Story! Have you ever successfully fought a low insurance offer, or walked away from a pushy dealership trying to overcharge your family? Share your victories and experiences in the comments below!

Share the Knowledge: Save this guide for your next family car purchase, and share it with friends or loved ones who are buying a car soon. This simple knowledge could save them thousands of dollars, keeping their household budget safe and sound!

Simple Answers to Keep Your Family Safe With car loan gap insurance

Families always have questions when buying a car. Here are 10 quick, easy answers (with no confusing bank words!) to help you protect your household.

1. What exactly does this do for my family?

If your car is ruined in a crash, it pays off the leftover bank debt that your regular insurance won’t cover, completely saving your kids’ savings account.

2. Is it a strict rule from the government?

No, it’s not a law. But if you are renting (leasing) a car, the dealer will usually ask you to get it to protect the vehicle before your family drives away.

3. How much does this safety net actually cost?

A pushy car dealer might charge you a huge $500 to $1,000 upfront. But if you call your own friendly insurance agent, they often just add $20 to $60 a year, saving you money for family pizza nights!

4. Will it pay my emergency cash fee during a crash?

No. If your regular insurance asks you to pay the first $500 from your own pocket, the bank simply takes that out of your final check. Always keep a little rainy-day cash saved up in a jar!

5. When is the best time to add this to my car?

Add your car loan gap insurance the exact same day you bring your new family car home, especially if your car payments stretch out for 5 long years (60 months).

6. Will it help if I miss a monthly car payment?

Sadly, no. If you skip a car payment to buy winter coats for the kids, this plan won’t forgive that missed payment, and it won’t pay for any late fees either.

7. Can I cancel it later and get my money back?

Absolutely! If you paid a big $1,000 charge at the dealer but worked hard to pay off your car early, call them for a refund for the unused time. It’s your family’s hard-earned money!

8. When exactly should I cancel it?

The exact month your hard work pays the loan down so much that you owe less than what your car is actually worth. Then, cancel your car loan gap insurance and put those extra dollars toward a family vacation!

9. Do I really need this if I buy a used car?

Yes! It is a great idea for a used family car too, especially if you bought it with very little cash down and a long, 5-year payment plan.

10. Where is the easiest place to buy it?

Skip the stressful dealer desk! The cheapest and safest way to get car loan gap insurance is to call your personal auto insurance agent, keeping your monthly bills low and your family stress-free.